Investors,

The stock market loves soft data, particularly at this stage of the monetary policy cycle where investors & financial markets are looking for additional signs that the Fed is done with raising interest rates. With disinflation firmly in place, but more progress required to defeat high inflation, the stock market ripped this week in light of 2 things:

Softer economic data, particularly for the labor market

Another Fed pause, the third non-hike meeting of 2023

In response, the S&P 500 gained a whopping +5.9% this week while other areas of the market enjoyed even larger gains. To be clear, I didn’t see this rebound coming. I’m totally fine with that, because I haven’t sold any material equity exposure this year and I’ve massively been a net-buyer of assets. It’s the old adage of “time in the market beats timing the market”. Weeks like this prove why this phrase is so important.

The Nasdaq-100 $NDX gained +6.5%.

The Russell 2000 $RUT gained +7.5%.

The NYSE FANG+ ETF $NYFANG gained +8.4%.

The Ark Innovation ETF $ARKK gained +18.6%.

These weekly gains roughly equate to the average calendar year return of the S&P 500!

Before diving into this edition of Cubic Analytics, where I’ll be analyzing the top trends within the economy, the stock market, and Bitcoin, I wanted to congratulate the team at MicroSectors for having 3 funds in the list of the top 6 YTD performers:

I’m proud to have MicroSectors as the sponsor for this edition of Cubic Analytics and encourage you to visit their website to learn more about their investment products and the various strategies that they’re using in the market.

I’ll be sharing more in the Sponsor section of the newsletter.

Macroeconomics:

The Federal Reserve left interest rates unchanged in their policy decision meeting on November 1st, leaving the effective federal funds rate at 5.33% for the second consecutive meeting. In their last five meetings, the FOMC has:

May 2023: Hiked +0.25%

June 2023: Paused

July 2023: Hiked +0.25%

September 2023: Paused

November 2023: Paused

For those of you who have followed my research closely, you’ll know that I was vehemently predicting another pause for this meeting even before the pause from the September meeting. Even in my 2023 outlook, I predicted the following:

“My baseline assumption is that the Fed will likely conduct 2-3 more rate hikes, for an aggregate amount of +0.5% to +1.25%, and that their balance sheet will decline in 2023.”

So far, the Fed has hiked a total of +1.0%. While most investors (and the market) was pricing in rate cuts during 2023, I told you that the Fed was going to stay the course and maintain their fight against inflation. They have.

It’s now clear that they’ve taken their foot off the gas pedal (or is it “off the brakes”?) and that they’re going to keep interest rates at this level for the coming months & quarters. As I’ve been sharing on Twitter & within these editions of Cubic Analytics, my base-case is that their first rate cut will happen no sooner than Q3 2024, barring a major recession or widespread financial crisis event.

As we look forward to the next meeting in December 2023, the final one of the year, the market is currently assigning a 95.2% probability that the Fed will pause again.

Specifically, I want you to focus on the trajectory of this probability by referencing the table at the bottom of the screenshot above…

One month ago, the probability of a pause was 64.5%

One week ago, the probability of a pause was 79.1%.

Today, the probability of a pause is 95.2%.

I fully expect to see this figure trend closer and closer to 100% in the coming weeks.

Why?

Because disinflation is firmly intact, as I’ve been saying all year, and because we’re seeing softer economic data and labor market dynamics. I’ve covered the latest round of inflation data (CPI & PCE) ad nauseam in prior reports, so I wanted to combine the latest round of labor market data to show forward-looking implications for inflation:

1. The quits rate continues to stabilize with a downward trajectory: I’ve highlighted this relationship in the past, but there’s a strong correlation between the quits rate and the YoY inflation rate. The chart below shows the quits rate vs. headline CPI (YoY) and core PCE (YoY):

With quits stabilizing for the 2nd consecutive month at 2.3% (down considerably from the peak of 3.0% in April 2022), the implication is that YoY inflation readings will continue on their path of deceleration and trend lower in the months ahead.

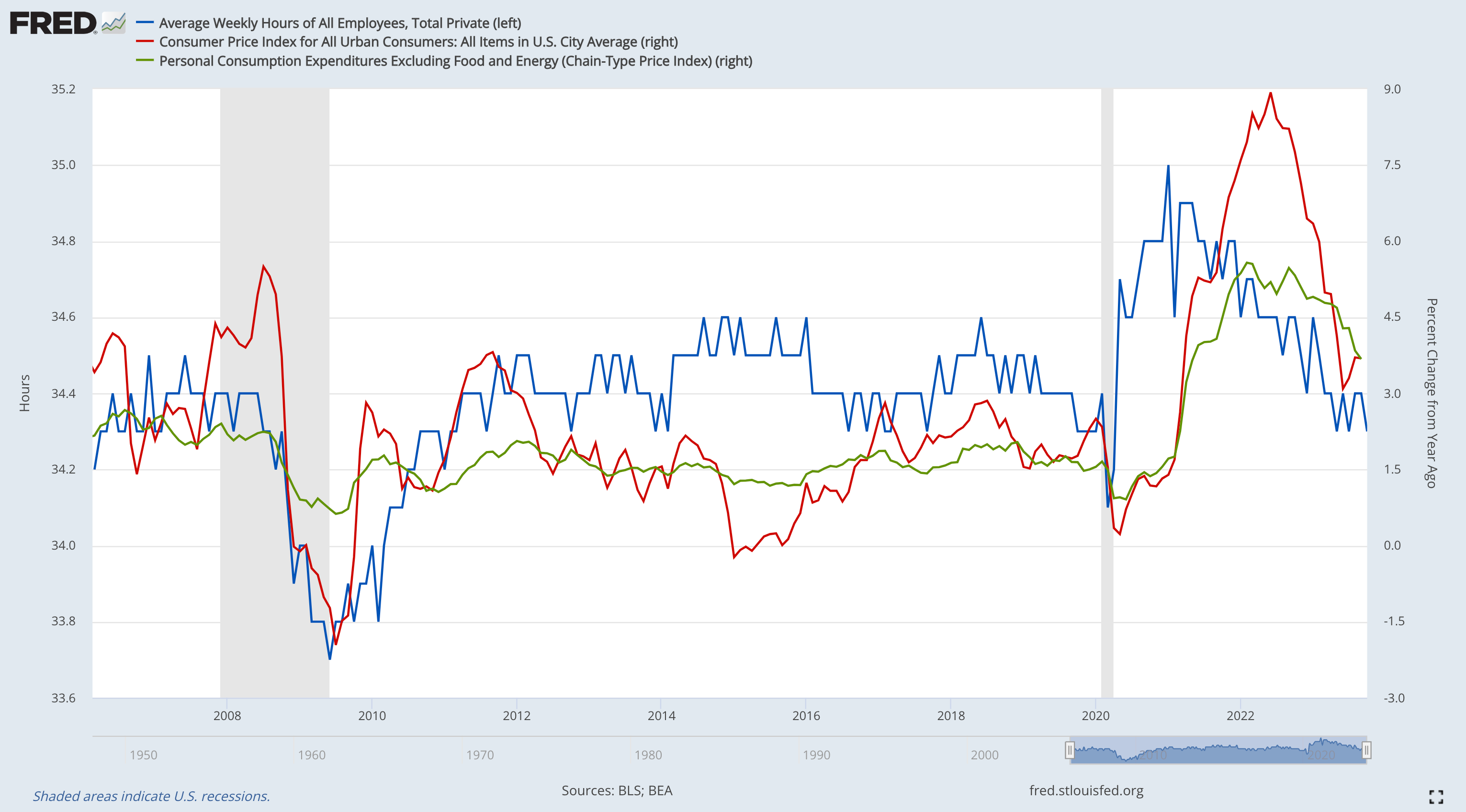

2. Average weekly hours worked continues to trend lower: I’ve also showcased this correlation, highlighting the total average number of hours worked and inflation, which is a particularly useful indicator as wage growth continues to decelerate.

Why?

Because if hourly wages are slowing and less hours are being worked, then personal disposable income should decelerate on both fronts (PDI = Wages * Hours Worked).

Thankfully, you don’t need to take my word for it, as the data quantifiably proves this:

As average hours worked increases, inflation tends to accelerate.

As average hours worked declines, inflation tends to decelerate.

It’s a very simple but logical correlation.

With average weekly hours worked declining in the latest monthly report, my assessment is that inflation will continue to decelerate (aka disinflation).

Therefore, based on this new labor market data, the implication is that disinflation will continue towards the Fed’s stated goal of a 2% inflation rate and the Fed just needs to let previous rate hikes ripple through the system & continue to have their intended effect.

As we look at the rest of the labor market data, it’s clear that conditions are softening.

However, I don’t want this softness to detract from the fact that the labor market, as a whole, is still dynamic & resilient. These are the two adjectives I’ve been using to describe the labor market for the past 18 months, and they are still valid today.

My key takeaways from JOLTS & Nonfarm payrolls are:

JOLTS: The stabilization of job openings in September are a sign that employers are still looking to hire and that there is an abundance of opportunity for those seeking employment. Additionally, the layoffs rate remains historically low at 1.0%, highlighting how labor turnover is very minimal and can be absorbed by the large amount of opportunities in the labor market. When the quits rate (2.3%) is larger than the layoffs rate (1.0%), it’s a sign that individuals have strong conviction in their ability to gain new employment opportunities or have already accepted new a new opportunity, which generally doesn’t happen in a recession.

NFP: The number of jobs created in the month of October missed estimates and came in below prior month results; however, it’s important to understand that the economy still added 150,000 new jobs during the month. This highlights softness, not weakness. The unemployment rate ticked higher from 3.8% to 3.9%, but this figure is also historically low. It’s rising from historically low levels, which is exactly what the Fed would like to see in order to accomplish their dual-mandate. While it’s appropriate to have concerns about the rising trend in the unemployment rate, I think it’s far too soon to panic. As a final note, nominal wage growth also decelerated on a YoY basis, reaffirming the disinflationary dynamics that we addressed above.

All in all, the labor market continues to be dynamic & resilient, but we are unequivocally seeing signs of softness.

No, that doesn’t mean deterioration.

No that doesn’t mean weakness.

It means softness.

Within a macroeconomic context, there’s a massive difference between deterioration (bad) and softening (not necessarily bad):

The macro doomers have endlessly shouted that the end is nigh, highlighting a myriad of catalysts and warning signs. None of them have materialized into a sustained contraction or downturn in economic activity, the labor market, or the consumer.

Housing unaffordability

Pending CRE collapse

Rising initial unemployment claims

Rate hikes

Sticky inflation

Multiple jobholders

Consumer credit

Rising defaults & delinquencies

Global conflicts

Unions & labor strikes

While I’m not dismissing the validity of these concerns, as I’ve referenced many of them myself, it’s vital to understand that these trends could reverse and that they can take a long time to impact the broader economy. My base-case scenario has been a steady & slow softening of labor market conditions, as I mentioned in my 2023 outlook:

“With a baseline expectation that the unemployment rate is likely to climb higher, I’m cautious of the economic implications… My base-case outlook is that the unemployment rate will at least reach 4.3% at some point in 2023.”

Notice the language that I used…

I didn’t say that a rising unemployment rate will lead to economic catastrophe. I said that I’m cautious of the economic implications. If anything, my expectation of a 4.3% unemployment rate was too gloomy! So far, the recent softness in the labor market is too early and too little to raise any significant red flags, which may change in the months ahead. Given the persistence of the resilient & dynamic nature of the labor market (and the broader economy for that matter), I think it’s more appropriate to think that this persistence will sustain itself for a bit longer.

Stock Market:

Tying together the economic dynamics above and how it relates to the stock market, I shared my immediate thoughts on Twitter/X to explain my views:

Considering that the Federal Reserve has already been pausing their rate hikes, the addition of softer economic data reaffirms the trend of disinflation and therefore reduces the likelihood of more rate hikes in the future. The stock market is therefore interpreting this soft data as being bullish, based on the sharp decline that we’re seeing in Treasury yields in response to this macro data.

For the market, which is a forward-looking pricing mechanism, that’s all that matters.

So long as data gets softer, but avoids entering worrisome territory, equity markets have the ability to grind higher. This week was proof-positive that this is true.

A key sign that I’ve wanted to see is for the S&P 500 to get back above the 200-day moving average cloud after recently breaking down two weeks ago. After this week’s strong move, we’ve checked that box off of my list.

While it’s not guaranteed that the index will stay above the 200-day MA cloud, this development is much more welcome than staying below the cloud. In other words, “not bearish” is good enough to be bullish (for now).

In fact, the Nasdaq-100 rebounded perfectly on its 200-day moving average cloud!

This is eerily similar to the rebound that occurred in March 2023 before the tech index experienced a massive rally going into the July YTD highs. This rebound, in and of itself, is bullish for technology stocks and mega-cap tech in particular. When we also recognize the bull flag, a potential breakout would add to the bull case.

I’d encourage all investors to closely monitor the Nasdaq-100 here. To be clear, I have zero interest in trading/investing in small caps stocks or the Russell 2000.

Bitcoin:

I remain very bullish on Bitcoin here at $34.7k, particularly as the market digests the significant gains from the past month. All of the market dynamics that I’m seeing look healthy & constructive within a 12-month uptrend.

Bitcoin dominance (Bitcoin’s market cap as a percentage of total crypto market cap) remain near YTD highs but has cooled off over the past few weeks. This has given many altcoins the ability to breath and experience strong gains. With equity market participation this past week, many altcoins showed a lot of strength.

Notably: $INJ, $SOL, $LDO, $LINK, $RNDR, $MKR, $SUSHI and $RUNE.

Here’s how I think Bitcoin dominance is likely to move in the weeks/months ahead:

It’s likely that we see some rotation here, but I think short-term traders should be enthusiastic about the conviction that we’re starting to see in the altcoin market.

I specifically want to highlight two of my recent posts on Twitter/X to ensure that everyone is aware of how I see the crypto market right now:

Best,

Caleb Franzen

SPONSOR:

This edition was made possible by the support of MicroSectors, a financial services and investment company that creates an array of unique investment products and ETN’s. Their NYSE FANG+ products are the only one of their kind, allowing investors to gain exposure, leveraged/un-leveraged & direct/inverse, to the NYSE FANG+ Index.

For investors who are looking to generate income on their assets while also having simultaneous exposure to FANG+ stocks, their new $FEPI product is extremely interesting and worth researching on your own.

I started a partnership with MicroSectors in 2023 because I’ve been using their products for over a year and it was an organic and seamless fit.

Please follow their Twitter and check out their website to learn more about their services and the different products that they offer.

DISCLAIMER:

This report expresses the views of the author as of the date it was published, and are subject to change without notice. The author believes that the information, data, and charts contained within this report are accurate, but cannot guarantee the accuracy of such information.

The investment thesis, security analysis, risk appetite, & timeframes expressed above are strictly those of the author and are not intended to be interpreted as financial advice. As such, market views covered in this publication are not to be considered investment advice and should be regarded as information only. The mention, discussion, and/or analysis of individual securities is not a solicitation or recommendation to buy, sell, or hold said security.

Each investor is responsible to conduct their own due diligence and to understand the risks associated with any information that is reviewed. The information contained herein does not constitute and shouldn’t be construed as a solicitation of advisory services. Consult a registered financial advisor and/or certified financial planner before making any investment decisions.

Please be advised that this report contains a third party paid advertisement and links to third party websites. These advertisements do not constitute endorsements. The advertisement contained herein did not influence the market views, analysis, or commentary expressed above and Cubic Analytics maintains its independence and full control over all ideas, thoughts, and expressions above. The mention, discussion, and/or analysis of individual securities is not a solicitation or recommendation to buy, sell, or hold said security. All investments carry risks and past performance is not necessarily indicative of future results/returns.

Will be interesting to see $BTC consolidate while allowing $ETH to play catch up.. great analysis my brother-🤝👽