Investors,

If you managed to maintain your composure this week, congratulations. I’m serious. Even as someone who’s primarily in cash right now (and has been since May 2022), this was a tough environment to stomach.

I have more in-depth thoughts & reflections on the recent market dynamics that I’ll cover later in this report, but I wanted to remind everyone about the core message that I’ve continued to share throughout the year. In fact, I reiterated this core concept in Edition #197 at the beginning of August:

“I feel quite confident that the S&P 500 will trade below Friday’s closing price of $4,145 within the next 6 weeks, giving investors a sufficient chance to buy the market at a lower price in the near future. If it doesn’t, I continue to dollar-cost average at a steady pace and won’t be upset if the market accelerates higher from here. My general market thesis for the year has been a two-pronged approach of:

Reducing short-term risk during market rallies by increasing cash position.

Increasing long-term risk by patiently allocating newly raised cash into core portfolio positions.

While I’m certainly enthusiastic about recent market trends, I’m generally viewing the strategy above as the most attractive option available to investors.”

I executed this strategy once again, reducing exposure to individual positions that I no longer wanted to hold for the long-term while simultaneously using cash to increase exposure to core positions that I intend to continue buying in this bear market.

The selloff event that we’re currently witnessing could be over very quickly, or it could continue to persist for weeks/months. We simply don’t know. Either way, I’ll continue to increase my long-term exposure to risk assets.

Macroeconomics:

There were three key aspects that I was focused on this week. Chronologically, they were:

Gross domestic income (GDI) data for Q2 2022 and the revised Q2 GDP.

Personal income and outlays for July 2022.

Jerome Powell’s press conference at the annual Jackson Hole symposium.

With these data points/events now at our disposal, here are the key takeaways & insights that I gained from each…

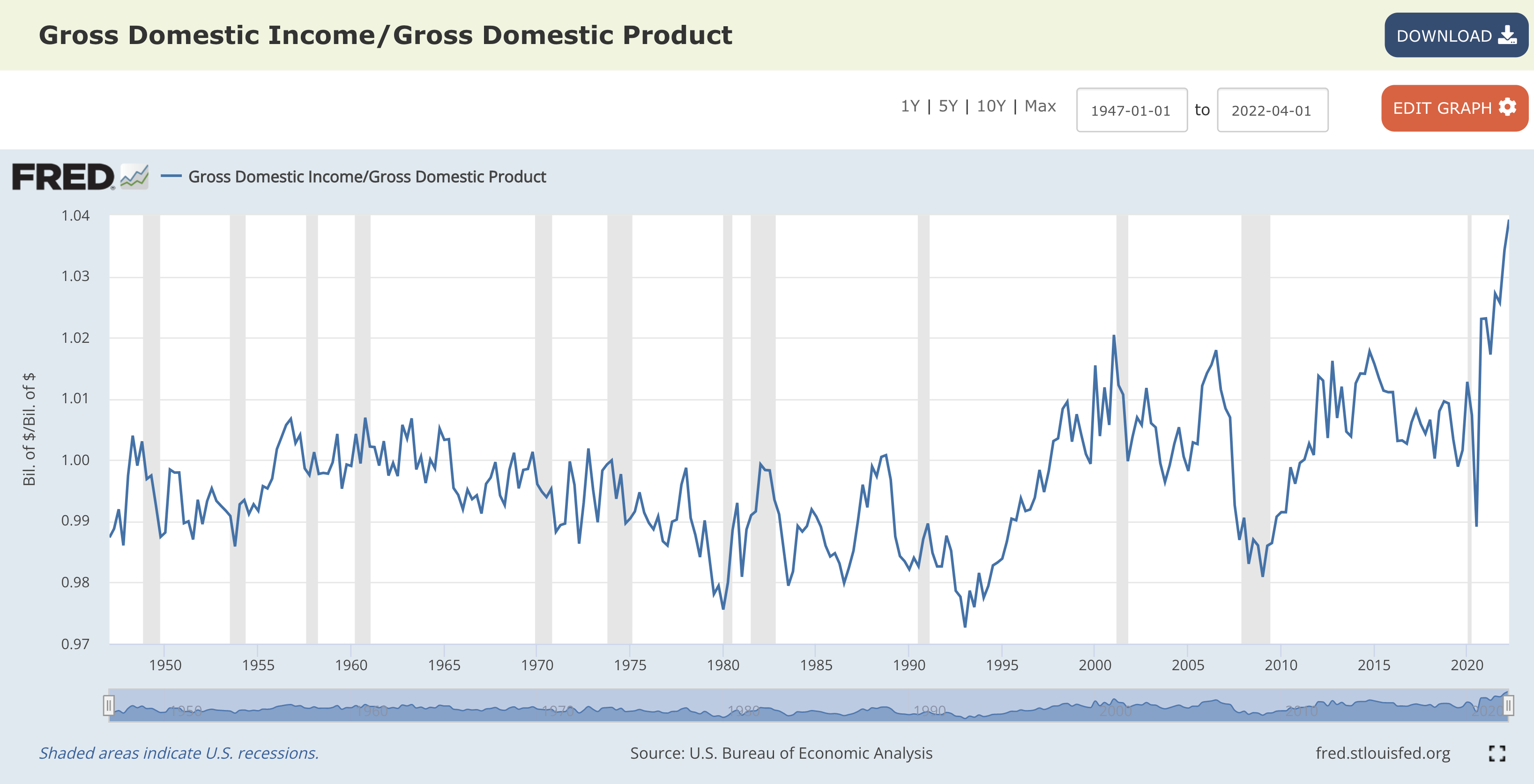

Regarding GDI, I was keen to review the Q2 data because of the interesting dynamics that we witnessed in Q1. Specifically, we saw a massive divergence between GDP and GDI, which are expected to move in-line with one another. In fact, entry level economics classes teach that there are multiple ways to calculate GDP, with one solution being to calculate the total income earned by all economic participants. As such, we’d expect to see these key measures of income & production grow and contract in tandem.

However, that is not what we saw in Q1, wherein real GDP contracted by -1.6% while real GDI grew by +1.8%. These contradictory data points suggest two different versions of the economy, one where incomes for corporations & individuals are expanding while production & economic activity are declining. Interestingly, the Q2 2022 data confirmed that this head-scratching dynamic continues to persist. As we know, Q2 GDP was negative; however, this latest report contained a revised figure of -0.6% growth vs. the original -0.9%. Meanwhile, Q2 2022 real GDI increased at a pace of +1.4%.

This prompted me to ask, what is the historic relationship between GDI & GDP. I referred to the Federal Reserve Economic Database (FRED) to calculate GDI/GDP and was astonished by the results:

Quite simply, gross domestic income has never been larger relative to gross domestic product and it’s growing at an unprecedented pace. This divergence highlights the unique economic environment that we’re in. From my perspective, this indicates that the U.S. economy has continued to trend towards stagflation, with consumers able to absorb higher prices while output remains anemic. By very definition, this means that more money is chasing fewer (or the same amount) of goods & services within the economy. In turn, inflationary pressures should persist.

This sentiment was confirmed by the personal income data for July 2022, which indicated that personal income grew by +0.2% relative to June 2022. This figure came in lower than estimates of +0.6% and prior month gains of +0.7%, but still indicates that incomes are rising. This reflects a strong ability for consumers to absorb higher prices for goods and services within the economy.

Another key datapoint from this report is Personal Consumption Expenditures (PCE), which is the Federal Reserve’s preferred method of measuring inflation. PCE inflation was +6.3% YoY for July 2022, down slightly from June 2022’s pace of +6.8%. However, it’s important to note that the month-over-month rate of change was -0.1% in July, indicating that the PCE fell MoM. On net, this means that the YoY dynamics are disinflationary and the MoM dynamics are deflationary. This was an important win for the Federal Reserve, who continues to remain steadfast in their fight against historic inflationary pressures.

Speaking of which, Jerome Powell’s speech at the Jackson Hole symposium was considerably underwhelming in terms of the content but produced an outsized impact on financial markets. Powell’s speech lasted a grand total of nine minutes vs. his scheduled time of thirty minutes, proving that he didn’t need long to put the market in its place.

His message was simple: the Federal Reserve will act with resolve in their fight against inflation and will continue to prioritize inflation.

This all but confirms the sentiment that I shared in March of this year, when I suggested that the current inflation dilemma is Powell’s “Volcker moment”:

There were two primary quotes that stood out to me during Powell’s remarks:

“High inflation has continued to spread through the economy. While the lower inflation readings for July are certainly welcome, a single months improvement falls far short of what the Committee will need to see before we are confident that inflation is moving down. We are moving our policy stance purposefully to a level that will be sufficiently restrictive to return inflation to 2%.”

“We must keep at it until the job is done. History shows that the employment cost of bringing down inflation are likely to increase with delay as high inflation becomes more entrenched in wage and price-setting. The successful Volcker disinflation of the early 1980’s followed multiple failed attempts to lower inflation over the previous 15 years. A lengthy period of very restrictive monetary policy was ultimately needed to stem high inflation, and to start the process of getting inflation to the low & stable levels that were the norm until the spring of last year. Our aim is to avoid that outcome by acting with resolve now.”

Powell repeatedly referred to Paul Volcker and invoked Volcker’s resolve throughout his speech, recalling the lessons learned from the inflationary 1970’s. Regardless of whether or not the market recognizes that this is Powell’s Volcker moment, the Federal Reserve believes that it is.

At the end of the day, that’s likely all that matters.

Stock Market:

It seems that we’re finally get the pullback that I’ve been waiting for. Admittedly, I didn’t think the market would be able to sustain as much of a rally as it did, but I continued to keep an open mind about market momentum. Since the beginning of August, I shared my perspective that an eventual pullback will need to be defended by investors:

What do I mean by “defend”? Quite simply, that the stock market indexes will need to produce a higher low relative to the June 2022 lows. I don’t care how deep the total drawdown is, all that matters is whether or not we can produce a higher low.

Market momentum since the June lows has primarily been fueled by two dynamics:

Market Positioning: Investors were extremely bearish in June, anticipating more inflation and an aggressive Federal Reserve. As upside momentum started to build, starting as a speculative rally, sidelined money started to flood back into the market & produce a self-fulfilling rally.

Peak Inflation Narrative: Since receiving the June 2022 CPI data (+9.1% YoY) in mid-July, the market narrative became: “it can’t get much worse than this.” Sure enough, the July CPI data seemed to reaffirm the disinflationary expectations that the market had, indicating that the Fed might be closer to the end of the tightening cycle. The sooner that inflation peaks, the sooner it declines, and the sooner the Fed can take their foot off the gas pedal. The “peak inflation” narrative soon became a “peak hawkishness” narrative, suggesting that the Fed might pivot/pause sooner than originally anticipated.

In my opinion, the market positioning aspect of this rally has now played out. In fact, one could argue that market positioning is now in an inverse position, indicating that too many people have FOMO’d into the market and are about to get caught offsides. Afraid to miss the beginning of a new potential bull market, investors rushed back into the market. This likely won’t lead to optimal outcomes, as I implied in this post:

As it pertains to the peak inflation narrative, Powell’s succinct speech on Friday morning quelled the idea of a pivot. The entire pivot narrative was extremely premature from my perspective, which I outlined in early August:

The stock market has seemingly lost both factors driving the market higher, so I’ll continue to be on the lookout for the next catalyst that could push asset prices in one direction or another. My best guess is that the S&P 500 falls below 3,900 (indicating potential downside of at least -3.9%), which would achieve a drawdown in excess of -9.9% from the August 16th peak.

Bitcoin:

With cracks appearing across the stock market, I’m surprised to see the crypto market hold up as well as it did this past week. Relative to prior Friday close, the S&P 500 had a weekly return of -4.04% while total crypto market cap fell by -3.9%. In a market environment where stocks & risk assets are selling off, I’d expect to see weaker returns from crypto.

With that said, crypto has fallen substantially more than the S&P 500 since the mid-August peak. Over this time period, we’ve seen the S&P 500 fall by -6.2% while Bitcoin and Ethereum have fallen by -19.8% and -26.1%, respectively. With Bitcoin hovering above $20,000, I think that the market is providing a clear accumulation signal based on the statistical long-term analysis that I’ve conducted. Though, to be clear, I certainly expect more downside.

I saw interesting analysis from Glassnode on Twitter, highlighting the potential support band & significant price levels:

With Bitcoin’s price falling below the realized price (the price of Bitcoin at last transaction value), the likelihood that we fall closer to the balanced price & delta price is growing. The $13.7k level of the delta price aligns with multiple other levels that I’ve outlined in various scenario analyses. In fact, I’ve continued to reiterate that the $13,000 range is my base case scenario.

Could we fail to fall that low? Absolutely. Am I mentally prepared for price to fall that low? Absolutely. Will I be buying Bitcoin as it falls towards that level? Absolutely.

Take care out there,

Caleb Franzen

DISCLAIMER:

My investment thesis, risk appetite, and time frames are strictly my own and are significantly different than that of my readership. As such, the investments & stocks covered in this publication are not to be considered investment advice and should be regarded as information only. I encourage everyone to conduct their own due diligence, understand the risks associated with any information that is reviewed, and to recognize that my investment approach is not necessarily suitable for your specific portfolio & investing needs. Please consult a registered & licensed financial advisor for any topics related to your portfolio, exercise strong risk controls, and understand that I have no responsibility for any gains or losses incurred in your portfolio.