Edition #197

Labor Market Resilience Pushes Risk Assets Higher

Investors,

This week was packed with important labor market data, helping to give key insights into how the economy has been responding to consistent & aggressive Federal Reserve policy. The rate hikes might seem mild, but it’s important to note that this is arguably the strongest magnitude of a tightening cycle that the U.S. economy has experienced.

Below is the YoY percent change in the effective federal funds rate:

While this is largely a function of the Fed dramatically raising rates from a target range of 0.00%-0.25%, the velocity & magnitude of this hiking cycle is unprecedented. As we embark through these uncharted waters of monetary policy, I’ll continue to provide actionable & objective insights on the economy, the stock market, and Bitcoin using a data-driven approach.

If you’re new to Cubic Analytics, please subscribe below! If you’ve been subscribed, please share this with any colleagues who might benefit from my research:

Macro & Monetary Policy:

Labor market data was the key focus for the week, helping to illustrate the impacts (or lack thereof) from the Federal Reserve’s ongoing rate hikes. We’ve seen headline after headline about layoffs and hiring freezes, but I continued to stress the importance of looking at both sides of the coin. We cannot analyze layoffs/hiring freezes in a vacuum and must contextualize them against hiring activity in order to monitor net employment activity.

Unfortunately for the Fed, the data we saw this week showed massive resilience & dynamic strength in the labor market. The Job Openings & Labor Turnover Survey (JOLTS) for June 2022 had some weakness, with job openings declining from 11.3M in the prior month to 10.7M. This decline is reflecting some potential weakness, but it’s difficult to contextualize why the decline is happening…

Are job openings declining because the positions are getting filled or because employers are simply delisting them? Considering that the former is a positive development and the latter is a negative development, this missing context makes it unclear whether or not this is a positive or negative sign. This is why it’s so vital to take a wholistic look at the labor market to get a firm grasp on the data.

As it pertains to the remainder of the JOLTS data, I was keen to monitor ongoing wage-price spiral dynamics, specifically:

The quits rate remained at/near record highs, measured at 2.8% in July.

The layoffs rate remained at/near record lows, measured at 0.9% in July.

Both of these figures were equivalent with the prior month, so the data continues to stabilize at these extreme levels.

What are the implications of this? First and foremost, it means that employees are able to enter a dynamic labor market with abundant options to find better opportunities, while employers remain extremely unwilling to depart from their skilled labor force. Employees, faced with ample opportunities to earn higher wages in a job more aligned with their skills, interests, and career goals, are maximizing their potential in the market.

Rightfully so! That’s a great environment to be in if you’re in the labor force.

Since May, I’ve been sharing my perspective that a high quits rate is fueling a wage-price spiral. Considering that job switchers generate a larger increase in their salaries than individuals who move up within a company, more quits equals more salary. Recent data from Axios helps to reaffirm this dynamic:

On an inflation-adjusted basis, a job switchers’ real earnings have grown by +9.7% vs. -1.7% for individuals who stay at the same company. This means that the 12-month moving average of nominal earnings growth for job switchers is likely above +16% as of March 2022.

As the quits rate remains at historically elevated levels, it will continue to create an environment where employees are growing their income at historically elevated levels. With rapidly increasing personal disposable income, the labor force has a greater propensity to absorb higher consumer prices. Employees who stay at their same company, with negative real earnings growth, are then incentivized to leave the company in order to capitalize on greater earnings potential and keep up with inflation pressures. This recursive cycle is what helps to fuel inflation, which fuels higher wages, which fuels more inflation, and so on.

The Federal Reserve Bank of Chicago acknowledged this dynamic in a 2015 paper, titled “Job Switching and Wage Growth”, concluding that:

“Job switchers drive up wages as they move up the job ladder.”

“The pace of job switching is a useful indicator for forecasting the behavior of wages & inflation.”

Based on the dynamic between a high quits rate and low layoffs rate, the labor market is telling us to expect more elevated inflation.

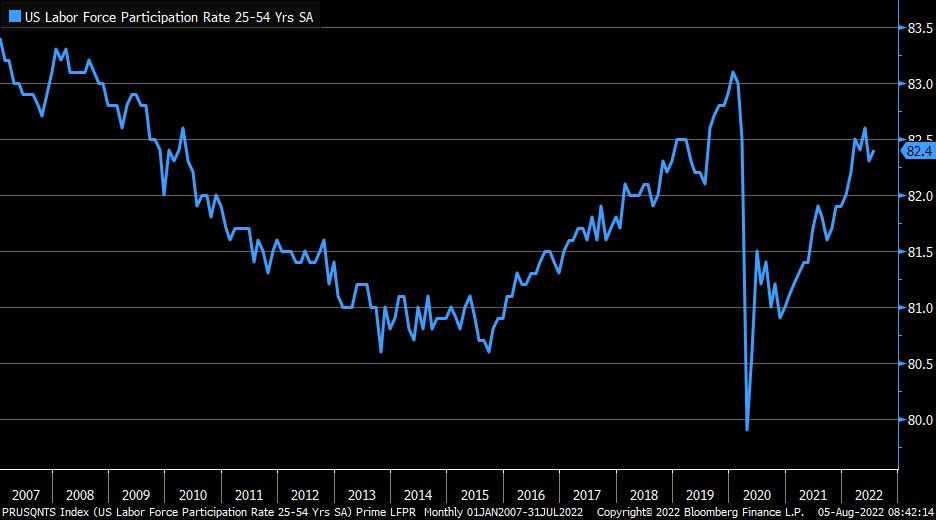

On Friday morning, the nonfarm payroll data was released for July 2022 in which median estimates were expecting to see 250k. Shockingly, the figure came in more than double at an extremely strong level of 528k jobs! Additionally, the unemployment rate decreased from 3.6% (where it was for four consecutive months) to 3.5%. The only weakness in this report was the decline in labor force participation rate (LFPR), which fell from 62.2% to 62.1%; however, the prime-age LFPR increased to 82.4%:

On net, I think the decrease in the total LFPR is outweighed by the increase in the prime-age LFPR.

As a final thought, I want to tie this into the Federal Reserve & the trajectory of monetary policy. Quite simply, the Fed cannot be enthused by this data considering that they are attempting to reduce demand in order to re-equilibrate the market at lower prices. Resilience in the labor market reflects a dynamic ability for earnings potential and therefore spending potential — the exact opposite of what the Fed is trying to accomplish. Since the Fed is unable to increase supply, they are forced to constrain demand to combat inflation. The rate of inflation for June 2022 was +9.1%, an absolutely unacceptable level for the Fed’s mandate of price stability.

The recent data suggests that a hot labor market will continue to keep inflationary pressures elevated, thus making the Fed’s job more difficult. In response, the Fed is likely to increase their pace of rate hikes with a stagnating economy (the U.S. has officially reached two consecutive quarters of negative real GDP growth) and runaway inflation.

While the market consensus has been that the Fed will likely raise rates by +0.5% in September, odds are increasingly favoring that the Fed will raise by +0.75%. Currently, the futures market is pricing in a 65% likelihood for 75bps:

One month ago, the market was anticipating a 3.4% chance of a 75bps rate hike in September. Despite this rapid re-pricing of a third consecutive +0.75% rate hike, financial markets & risk assets have been shrugging off this hawkish development…

Stock Market:

Despite the more aggressive developments happening in the monetary policy environment, based on resilient labor market data, asset markets continue to grind higher. Each of the major U.S. indexes had respectable weekly returns of:

Dow Jones Industrial Average $DJX: -0.12%

S&P 500 $SPX: +0.36%

Nasdaq-100 $NDX: +2.0%

Russell 2000 $RUT: +1.95%

Investors clearly have an appetite for technology & growth related stocks, as well as small-caps. If we move further out onto the risk curve, the iShares Expanded Tech ETF, IGV 0.00%↑, had a weekly return of +3.7%. IGV has experienced eight consecutive trading sessions where the daily close was higher than the daily open. This has been the longest such streak since March 2021, when the market gained +14.5% over a 3-week span. IGV has gained +19.8% since the YTD lows in June 2022, indicating that investors have a strong demand for risk assets.

As it pertains to the broader market, IGV is trading at a pivotal support & resistance range, indicating that price may be at an important inflection point. If price can break above this range, it has the potential to extend higher & flip this level into support. If price gets rejected on this range, as it has in the past, it could be indicative of fading market momentum. In my opinion, this sensitive pocket of the market will likely foreshadow more significant moves for the broader stock market & even for Bitcoin.

The market is experiencing a positive momentum thrust, which investors continue to be suspicious of. The S&P 500 is currently generating the strongest rally of 2022, up +13.8% from the YTD lows just seven weeks ago. Without question, the market will experience a cooldown period and exhale. When it does, investors will need to swiftly defend against the drawdown and be able to increase their demand for risk assets. Specifically, the market will need to produce a higher low in order to increase the probability that we are in a sustainable bull market trend reversal, the same way that the market produced a lower high at the start of the bear market trend reversal in Q1 2022.

I feel quite confident that the S&P 500 will trade below Friday’s closing price of $4,145 within the next 6 weeks, giving investors a sufficient chance to buy the market at a lower price in the near future. If it doesn’t, I continue to dollar-cost average at a steady pace and won’t be upset if the market accelerates higher from here. My general market thesis for the year has been a two-pronged approach of:

Reducing short-term risk during market rallies by increasing cash position.

Increasing long-term risk by patiently allocating newly raised cash into core portfolio positions.

While I’m certainly enthusiastic about recent market trends, I’m generally viewing the strategy above as the most attractive option available to investors.

Bitcoin:

While stocks have been celebrating higher, Bitcoin and crypto have generally remained stable over recent weeks. For Bitcoin specifically, price has settled around the $23k level for the past 2-3 weeks. The ETH/BTC ratio, a critical measure of risk appetite in the crypto market, has been trending higher during this 2-3 week window. With $ETH generally outperforming $BTC, this reaffirms the dynamics in the stock market where tech & high growth sectors are leading the broader market.

From my perspective, crypto & Bitcoin bulls should generally be thankful when ETH/BTC is rising because it generally indicates that risk appetite is rising and momentum is growing to the upside. Consider this: ETH/BTC bottomed in mid-June, exactly when the crypto market bottomed & the entire industry has been rising higher. In fact, the ETH/BTC ratio is extremely correlated to the entire market capitalization of the total crypto market, such that:

ETH/BTC ↑ = Crypto Market Cap ↑

ETH/BTC ↓ = Crypto Market Cap ↓

The chart below shows ETH/BTC in green/red candles and the total crypto market cap in teal. They typically generate local tops & bottoms in tandem, or with a minor lag.

I don’t think this is a coincidence. Therefore, in order for the broader crypto market to keep rising in the short-run, I think we’ll need to see ETH/BTC rising as a core confirmation of a bullish trend.

As ETH/BTC continues to ramp higher, I’m seeing continued signs of increased risk appetite & a momentum thrust. These are positive developments, though I expect to see them cooldown in the near future, similar to my prediction for a minor consolidation of the S&P 500. On a multi-year basis, ETH/BTC is now trading back within an important channel range:

This channel acted as the line in the sand for a bear market breakdown, which is exactly what took place. As soon as price broke below the channel, it experienced a massive cascade lower. Now that we’re back within this range, we have the opportunity to manage risk around the same levels.

Best,

Caleb Franzen

DISCLAIMER:

My investment thesis, risk appetite, and time frames are strictly my own and are significantly different than that of my readership. As such, the investments & stocks covered in this publication are not to be considered investment advice and should be regarded as information only. I encourage everyone to conduct their own due diligence, understand the risks associated with any information that is reviewed, and to recognize that my investment approach is not necessarily suitable for your specific portfolio & investing needs. Please consult a registered & licensed financial advisor for any topics related to your portfolio, exercise strong risk controls, and understand that I have no responsibility for any gains or losses incurred in your portfolio.