Investors,

This was a shaky week in terms of economic data and movements in the financial markets. We’ve unquestionably been in a euphoric environment for the past few weeks, fueled by a somewhat speculative mania and a massive divergence between optimists & pessimists. It seems as though both sides have ammunition to defend their perspectives, but I’ve generally avoided taking a stance on short-term market dynamics. All I do know is that short-term fear creates long-term opportunities.

Selfishly, I’ve been hoping for another consolidation so that I can buy high-conviction & core portfolio positions at even more attractive prices; however, I’ve been patiently adding exposure for the past few months. Regardless of the short-term environment, I’ll continue to be a net buyer of assets. The only variation is the pace at which I’ll be buying:

In a rising market, I’ll reduce the pace/magnitude of my purchases.

In a falling market, I’ll increase the pace/magnitude (though generally staying in a defensive mindset).

Reducing short-term risk while patiently increasing long-term risk has been the name of the game in 2022, allowing investors to take chips off the table during market rallies and then steadily increase exposure thereafter. The macro environment & financial conditions continue to remain highly uncertain from my perspective, so I believe that this patient approach is a win-win scenario.

Is it optimal? No, but it’s good enough and has allowed me to feel comfortable regardless of how the market performs in the short-run.

Here are the most important charts & developments that I want you to know:

Macroeconomics:

Economic data didn’t dominate the headlines this week, but I still think there were important developments that should be highlighted. Here were the three main components that I focused on:

July 2022 retail sales

Housing market data

Leading economic indicators by The Conference Board

Retail sales has been fairly stagnant, if not negative, in recent reports, particularly when adjusted for inflation data. As the economy continues to trend closer to a recession, this is a key data point to track. For the month of July, retail sales was unchanged on a month-over-month basis at ±0%, but increased by +10.3% on a YoY basis. The YoY increase was an improvement relative to June’s +8.5% YoY increase, so I think we can say that retail sales accelerated vs. June. However, if we adjust this nominal data for inflation, therefore measuring real retail sales, the actual YoY data declines to +1.7% vs. July 2021:

This is relatively anemic growth in retail sales, but not out of the ordinary vs. the historic trend. Note that the 2010-2019 data primarily fluctuated between a YoY % change of +1% to +5%.

Generally speaking, the retail sales report wasn’t great but it wasn’t terrible either. On net, I think it’s a positive development that we aren’t seeing worse data and that the U.S. consumer is remaining resilient, even if they’re relying more heavily on credit-based consumption.

Unfortunately, housing market data painted a significantly worse picture, reaffirming a continued downtrend in the real estate market. As a result of higher mortgage rates, housing market activity is slowing down dramatically and prices are certainly reflecting this decline. Quite simply, we haven’t seen mortgage rates accelerate at such a rapid pace, increasing by +89% relative to July 2021.

As a result of rapidly declining affordability, the recent data is deteriorating:

Existing home sales fell by -5.9% MoM and -20.2% YoY

Housing starts declined by -9.6% MoM and -8.1% YoY

Mortgage applications declined by -18.4% YoY

Amazingly, the national median home price increased by +10.8% on a YoY basis, but fell by -2.64% vs. June 2022. Unequivocally, the housing market is deteriorating. Unfortunately, with rates remaining at such a high level, the monthly decline in prices isn’t necessarily affordable due to higher debt-servicing costs.

Finally, The Conference Board updated their leading economic indicators (LEI) on August 18th, showing another decrease for the month of July 2022. This marks the fifth consecutive month of a decline, and a total decline of -1.6% since January 2022 which erases all gains made in the prior six months. The report specifically cited:

Consumer pessimism

Equity market volatility

Slowing labor markets

Housing construction

Manufacturing new orders

All of these factors “suggest that economic weakness will intensify and spread more broadly throughout the U.S. economy.” The last time The Conference Board’s LEI declined for five consecutive months was just prior to the Great Recession.

Amidst a wide array of weakening data, this essentially confirms that economic fundamentals are deteriorating while inflation remains historically elevated.

Stock Market:

Investors continue to ride the emotional rollercoaster of the market. As I explained at the beginning of this letter, markets were euphoric last week and even at the beginning of this week. I saw bulls dancing on the graves of bears across Twitter, essentially shaming people for being skeptical about the market rally.

After rising in a straight line for the past four weeks, I warned that an eventual cooldown was inevitable:

The market peaked during Tuesday’s session and rolled over considerably in the second half of the week, with most of the damage coming on Friday. On net, each of the indexes had a negative weekly return relative to last Friday’s close:

Dow Jones $DJX -0.17%

S&P 500 $SPX -1.2%

Nasdaq-100 $NDX -2.38%

Russell 2000 $RUT -2.94%

Meanwhile, the riskiest stocks (measured by ARKK 0.00%↑) had the weakest performance, falling by -14.1% week-over-week.

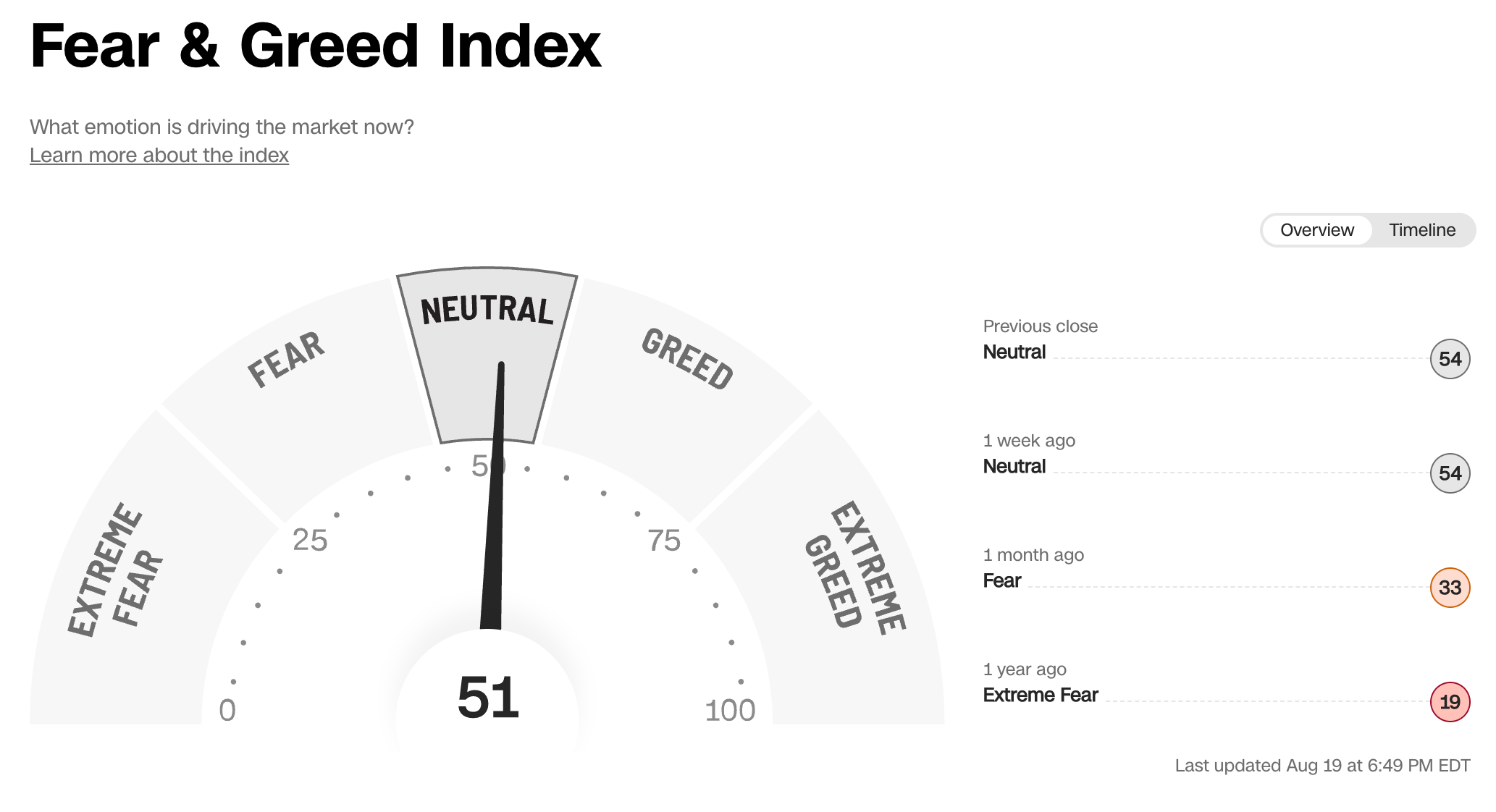

The Fear & Greed Index is currently reflecting “neutral” market sentiment, but I’d argue that sentiment is currently a tug-of-war between the optimists and the skeptics, rather than a battle between optimists and pessimists.

While pessimists certainly exist, it feels like the market consensus is that the YTD lows are in. Therefore, I think it’s a reasonable expectation that the market could continue to consolidate but essentially produce a higher low. In order to gain higher conviction that we’re in a new bull market, buyers will need to defend an eventual pullback (whether or not this is “the” pullback):

I posted this Tweet more than two weeks ago and it’s very possible that we’re about to witness the extent of the market’s conviction. As always, time will tell…

Bitcoin:

With pressure spreading across the equity market, crypto is facing the brunt of the pressure. Since the August highs, Bitcoin & Ethereum have both fallen by a significant amount:

BTC -16.6%

ETH -20%

(as of August 19th at 7pm ET)

Earlier this week, I posted in-depth analysis on YouTube to highlight the concerning dynamics that I was seeing for Bitcoin. Notably, the significant underperformance vs. other risk assets made me cautious that BTC was about to get even weaker. Since posting that analysis, that’s exactly what we’ve seen. Rather than re-hashing the same data, I’d refer you to watch the video below:

Best,

Caleb Franzen

DISCLAIMER:

My investment thesis, risk appetite, and time frames are strictly my own and are significantly different than that of my readership. As such, the investments & stocks covered in this publication are not to be considered investment advice and should be regarded as information only. I encourage everyone to conduct their own due diligence, understand the risks associated with any information that is reviewed, and to recognize that my investment approach is not necessarily suitable for your specific portfolio & investing needs. Please consult a registered & licensed financial advisor for any topics related to your portfolio, exercise strong risk controls, and understand that I have no responsibility for any gains or losses incurred in your portfolio.

Great writing Caleb. Your common sense approach, to see whole market based on data, couldn't be any more accurate.

But will argue regarding real estate guesstimate, typical well do buyers are not concerned with rates much , they know market and value ,they are looking for a better quality money can buy in location they need .Builders are not starving , they continue control price on what they produce "less is more ..expensive " approach, control cost by buying premium market at reduced rate.

Being reasonable in my books on achievement of 70 % + return from June in $NAIL telling all .

Seems like most retail investors are anticipating another big drawdown, which could certainly mean the opposite will actually happen.