The Stock Market Is Not The Economy

Investors,

It’s perfectly fine to accept that good things are happening in the economy while recognizing that great things are not. However, we must also be willing to accept that “great” things are not an exclusive requirement for asset prices to rise. In July 2022, I mentioned how the stock market doesn’t bottom on good news, but rather on “less worse” news.

Since then, the S&P 500 has gained +10.1% and the Nasdaq-100 has gained +21.1%, despite both indexes making new lows in September & October 2022.

It’s also important to recognize that, while stocks and the economy can be correlated, the stock market is not the economy (and vice versa). For example, I was recently scrolling through photos on my phone & saw this screenshot from August 2020:

Stocks were at all-time highs after gaining +55% amidst 1/7 Americans filing for unemployment benefits. Clearly, stocks can perform very well in an environment where macroeconomic fundamentals are poor.

Given my strong emphasis on the economy, I want to reiterate that I’m not dismissing the impact of macroeconomic fundamentals on the stock market; however, I fully concede that there are an array of factors that influence asset prices at any given moment. The point is, determining asset prices requires a multivariate analysis, of which the fundamental economy at any given point in time is merely one factor.

If anything, the rate of change of economic circumstances, notably those that impact monetary policy, the labor market, inflation, and liquidity dynamics.

So how are these components changing right now?

Monetary policy is becoming less aggressive, given the Fed’s step-down in rate hikes from +0.75% to +0.5% to three +0.25% to a pause in June 2023. The pace of rate hikes, even if the Fed restarts rate hikes in July, is considerably slower than it was in 2022. Monetary policy is restrictive, but it’s becoming less aggressive. While this may seem like an insignificant nuance, it’s not. Less aggressive monetary policy is better for asset prices.

The labor market, which has been historically resilient, has shown more pronounced cracks and signs of potential weakness. The unemployment rate of 3.7% is higher than it was one year ago at 3.6%, the first positive YoY percent change in a post-COVID era. Initial unemployment claims are accelerating higher, even if they remain at historically low levels. Wage growth is still high, but decelerating. The amount of job openings have been resilient lately, but are trending lower over the past 12 months. Still, labor market participation is rising. It’s too early to aggressively ring alarm bells, though investors should be on alert for more decisive deterioration in the labor market going forward, which would not be good for asset prices.

Inflation is dead. More specifically, the pace of price increases from 2021 and 2022 is far behind us. We are firmly in disinflation, which is characterized by a deceleration of price increases. Whether we’re talking about consumer prices or producer prices, and the various measures of these baskets (core, median, trimmed-mean), inflation has been trending lower for the past 11 months. My December 2022 prediction for clear disinflation going forward has been validated and I suspect that disinflationary trends will continue for the remainder of the year at a strong pace. In fact, I think that deflation is becoming more probable than a re-acceleration of inflation. Disinflation has been and will continue to be good for asset prices.

Liquidity conditions are a mixed bag depending on the nature of which measures are being focused on. Are we talking about global liquidity or domestic liquidity? Are we talking about financial conditions in the commercial banking system, or Federal Reserve induced liquidity? My general views on liquidity can be explained by the following: liquidity is not good on an absolute basis, but it’s less worse than it was last year on a rate of change basis. On net, this has been good for asset prices.

Given that the top two stories of 2022 were inflation & the Fed’s monetary tightening, the “less worse” nature of these two components is creating tailwinds for asset prices.

Could these four components above significantly worsen going forward? Yes.

However, we don’t have evidence of that right now.

Stocks are in an uptrend. Bitcoin is in an uptrend. Inflation is in a downtrend.

These are unequivocal facts, which then force us to debate what these trends look like on a go-forward basis. As the saying goes, the trend is your friend. Therefore, I believe that normal circumstances will prevail, where inflation resumes its march towards the Fed’s 2% target and asset prices continue to climb a wall of worry.

This report will succinctly highlight one critical chart in each of the following areas:

Macro

Stock market

Bitcoin

These are the top charts & datapoints currently on my radar:

Macroeconomics:

The S&P Global Flash U.S. Composite Index was published on Friday, June 23rd, which includes the service and manufacturing sectors. In this particular data, a result above 50 indicates an expansion, while a reading below 50 indicates a contraction.

The latest data showed the following:

S&P Global Flash US Services PMI = 54.1 vs. prior 54.9

S&P Global Flash US Manufacturing PMI = 46.3 vs. prior 48.5

Flash US Manufacturing Output Index = 46.9 vs. prior 51.0

S&P Global Flash US PMI Composite Output Index = 53.0 vs. prior 54.3

In plain english:

Services are expanding at a slower rate than in May.

Manufacturing is contracting at a faster pace than in May.

On the aggregate, these components are expanding at a slower rate.

From this data, we can extrapolate two key takeaways using a Keynesian approach to economics:

The economy is slowing down, but still growing.

Given the correlation between growth and spending, it’s likely that we will see slower spending trends going forward, which therefore means that there will be less inflationary pressures. Translation: expect to see more disinflation.

Given the recent expansionary reading for the Composite PMI data, it’s safe to say that the economy has been more resilient than expected; however, I want to be clear that my baseline assumption is for steady & moderate deterioration going forward. Given this “moderate” deterioration, we should expect to see some upside surprises & resilience within a broader downtrend of slower economic growth & the potential for outright contraction over the next 12 months.

This has a direct impact on inflationary pressures and the ongoing trend of disinflation. In fact, the PMI report even shared the following perspective about inflation:

“Despite a sharper rise in cost burdens, U.S. firms raised their selling prices at the slowest pace since October 2020.”

This bodes well for further disinflation in the months ahead and continues to reaffirm my belief that YoY inflation readings will decelerate substantially through the end of 2023.

Stock Market:

Small caps, on the aggregate, are the worst possible investment in the stock market right now. Particularly given the Russell 2000’s significant exposure to the financial sector and banking stocks, we continue to see that the S&P 500 is outperforming the Russell 2000 (SPX/RUT):

This relationship is pushing up against YTD highs, just below the all-time highs from March 2020.

Bears continue to beat the drum that this is a negative development, representative of unhealthy market behavior. That’s just simply not true.

In fact, it’s extremely common for technology to outperform small-caps during a broad-market uptrend! Take for example the Nasdaq-100 relative to the Russell 2000:

You’ll notice that this relationship was falling steadily in the years leading into the Great Recession… was that healthy? History tells us no.

What about after the Great Recession? We can see a steady & consistent uptrend, with technology stocks making higher highs and higher lows relative to small caps. Has the market been unhealthy for the past 15 years? I’d suggest that we’ve been experiencing one of the strongest & longest bull market uptrends in U.S. history.

The point is, we should be celebrating the fact that the largest & most promising companies in the United States are doing so well, given the evidence that this is common during a broad-market uptrend.

Bitcoin:

Bitcoin hit new YTD highs on Friday, piercing above $31,000 and climbed as high as $31,400. The bullish structure in the $25k to $27k range was crystal clear, which I reiterated in real-time in these reports, on Twitter, and on group calls with premium members. As we stand here this morning around $30.7k, on-chain fundamentals & technical analysis remains bullish on a multi-month basis.

While I wouldn’t be surprised to see another consolidation to the $27k level, I lean towards bullish scenarios over the coming weeks, potentially getting as high as $34.4k.

Given the pace of the rise from $25k to $31k, this price target feels quite conservative.

Here are the facts about Bitcoin right now:

12-month Williams%R ≠ “oversold”

18-month Williams%R ≠ “oversold”

24-month Williams%R ≠ “oversold”

Bitcoin trading above the 200-day moving average

Bitcoin trading above the 200-week moving average

Bitcoin trading above the AVWAP from the 2021 cycle highs

Bitcoin trading above the short-term holder realized price

Bitcoin trading above the long-term holder realized price

Short-term holder realized price > long-term holder realized price

All of these statistical indicators reflect bullish behavior.

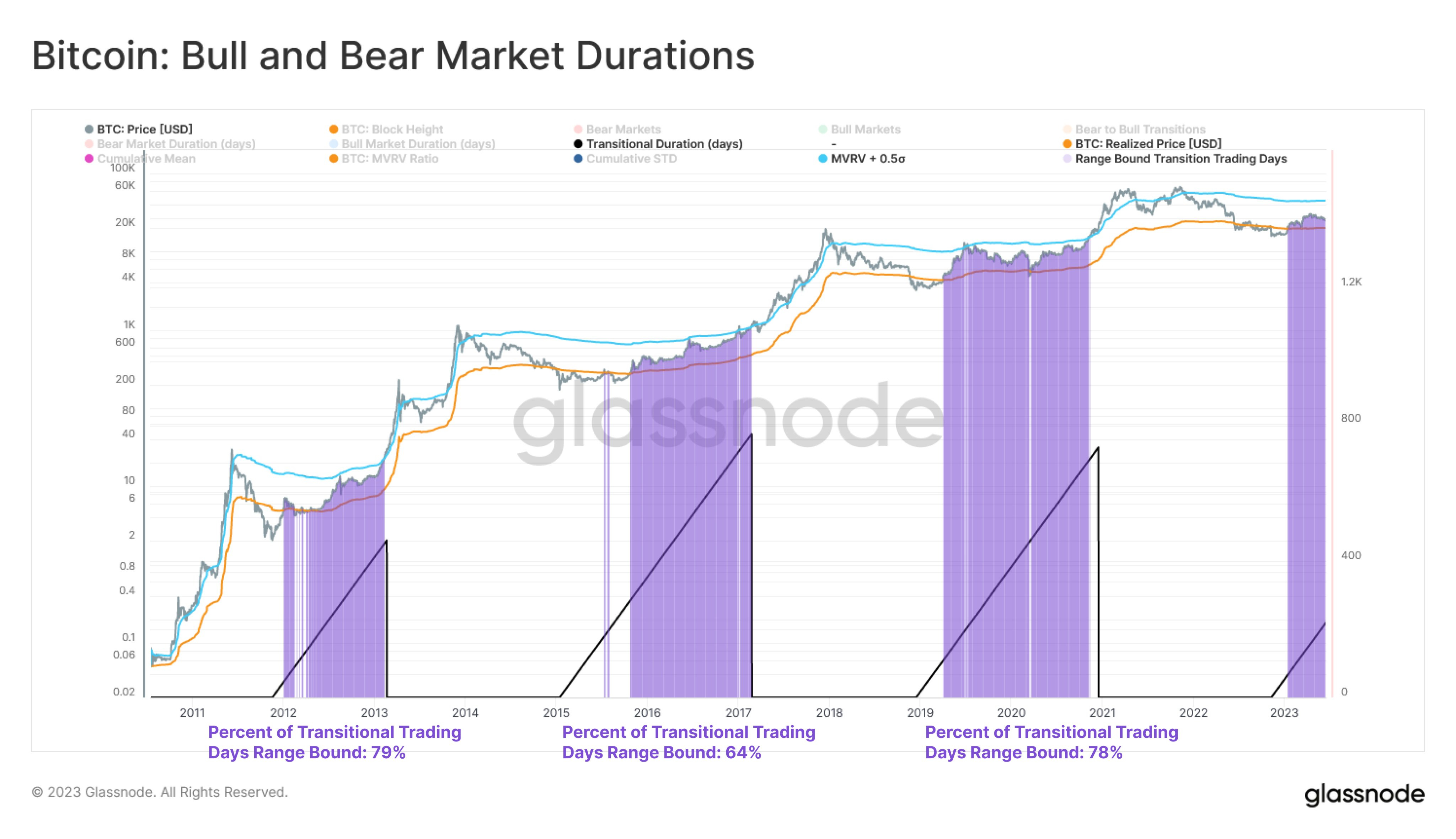

Regarding on-chain data,

This chart shows, quite simply, the bullish tailwinds that have followed once Bitcoin is able to break above the long-term holder realized price after a bear market. After each of these reclaims, price has rapidly approached the MVRV plus half a standard deviation. Bull market trends typically ride the upper-bound higher, but I still think it’s premature to suggest that this is the most likely case over the medium-term.

Either way, I think it’s totally permissible for investors to feel bullish.

I’ll do my best to remain cautiously optimistic, as usual.

Best,

Caleb Franzen

Caleb Franzen

SPONSOR:

This edition was made possible by the support of MicroSectors, a financial services and investment company that creates an array of unique investment products and ETN’s. Their NYSE FANG+ products are the only one of their kind, allowing investors to gain exposure, leveraged/un-leveraged and direct/inverse, to the NYSE FANG+ Index. They have a suite of products ranging from big banks, to oil and gas, and even gold/gold miners. I’m currently using two of their products, GDXD -0.81%↓ and OILD 0.80%↑ as short-term trades to bet against gold miners and energy stocks!

I started a partnership with MicroSectors because I’ve been using their products for over a year and this was an organic and seamless fit with my views.

Please follow their Twitter and check out their website to learn more about their services and the different products that they offer.

DISCLAIMER:

This report expresses the views of the author as of the date it was published, and are subject to change without notice. The author believes that the information, data, and charts contained within this report are accurate, but cannot guarantee the accuracy of such information.

The investment thesis, security analysis, risk appetite, and time frames expressed above are strictly those of the author and are not intended to be interpreted as financial advice. As such, market views covered in this publication are not to be considered investment advice and should be regarded as information only. The mention, discussion, and/or analysis of individual securities is not a solicitation or recommendation to buy, sell, or hold said security.

Each investor is responsible to conduct their own due diligence and to understand the risks associated with any information that is reviewed. The information contained herein does not constitute and shouldn’t be construed as a solicitation of advisory services. Consult a registered financial advisor and/or certified financial planner before making any investment decisions.

This report may not be copied, reproduced, republished or posted without the consent of Cubic Analytics and/or Caleb Franzen, without proper citation.

Please be advised that this report contains a third party paid advertisement and links to third party websites. These advertisements do not constitute endorsements and are not necessarily representative of the views or opinions of the newsletter author. The advertisement contained herein did not influence the market views, analysis, or commentary expressed above and Cubic Analytics maintains its independence and full control over all ideas, thoughts, and expressions above. The mention, discussion, and/or analysis of individual securities is not a solicitation or recommendation to buy, sell, or hold said security. All investments carry risks and past performance is not necessarily indicative of future results/returns.

Another outstanding newsletter! You positively nailed Bitcoin's price action. I must admit, I was rooting for you to be wrong regarding support around $25,000 (I certainly didn't try to hide my hopes for an epic selloff below $20K to offer better buying opportunities, but so be it).

I've found I'm actually more comfortable investing in bear markets than bull markets, so I've come to rely on your analysis to help me navigate uptrends. I know. It sounds counter-intuitive for a long-term investor who doesn't short (much) to actually PREFER the selloffs, but I guess it's a result of PTSD from me starting in the markets in 1998 and then getting my butt handed to me in 2001 and 2008 (not to mention a few less-severe smackdowns aside from those).

Anyway, thank you for all of your amazing work and analysis, Caleb. Your comprehensive work helps guide my investing journey, and I am truly grateful.