The Earthquake Effect

Investors,

This report is an exclusive deep-dive and analysis of overall market conditions. There was absolute chaos in the market this week, for better and for worse, and I’ll be addressing the fundamental reason(s) why this is happening. If you enjoy this analysis, please like the post and share with any colleagues that might be interested.

I am also available for 1-on-1 meetings, which can be scheduled at the link below:

Book a meeting with Caleb Franzen

We can address any questions that you might have about this report, or broader market dynamics that are at the top of your mind. Either way, I’d love to chat!

A Receding Tide of Liquidity

In coastal geographies, earthquakes can pose a unique risk to the local population and ecosystem. During a high-magnitude earthquake, a dramatic shift in the underlying seafloor can displace the ocean water. In response, the ocean water begins to recede away from the coastline, setting up the next chaotic phase of a natural disaster. The ocean water eventually comes back with a vengeance, in the form of a tsunami or massive tidal wave. This is exactly what happened in 2004, when a 9.1 magnitude earthquake near Indonesia produced a tsunami that killed an estimated 230,000 people.

This CGI video helps to illustrate this dynamic perfectly:

As an economist & financial market analyst, why am I attempting to explain geological science? Because this is essentially what’s happening in the financial markets right now, and recent events (particularly in crypto) are proof-positive that the tide is going out.

There’s a classic saying in finance that goes along the lines of:

“You don’t know who’s swimming naked until the tide goes out.”

We’re going to explore exactly what this means and why it’s relevant in the current market conditions & broader monetary policy environment. Bear with me as I bridge the analogy of the earthquake/tsunami into the current financial market environment.

From a high-level perspective, here’s what we need to know:

Earthquake = inflation

Tectonic plate displacement = Federal Reserve rate hikes & balance sheet reduction

Receding water = declining market liquidity

Tsunami = financial market failures, deleveraging, bankruptcies

The financial market earthquake (aka inflation) happened in mid-2021, which prompted historically aggressive monetary tightening starting in March 2022. In response to rapid interest rate hikes by the Federal Reserve, we’ve seen liquidity disappear and expose a variety of bad actors, over-leveraged investors (both retail & institutional), and even outright scams/Ponzi schemes. The latest collapse of FTX is the latest example of someone swimming naked; however, it’s far too soon to tell if it’s the result of negligence, malice, or a combination of both.

The tide has rapidly receded, exposing a variety of naked swimmers that no one had suspected of swimming naked. Remember, 99% of concerns about Terra Luna were dismissed when the UST stablecoin started to de-peg from $1.00. The founder & CEO, Do Kwon, famously took to Twitter and reassured investors that everything was fine. Suddenly the value of their token & the entire $40Bn project ecosystem imploded in a matter of days.

Shortly thereafter, fringe concerns were being voiced about another crypto company, Celsius, and their corresponding token. Most of these concerns were dismissed, labeled as FUD (fear, uncertainty, and doubt), but reality quickly set in. Depositors were unable to access & withdrawal their funds, the company filed bankruptcy & the CEO resigned. No one was concerned about Voyager Digital until, all of a sudden, everyone was concerned. They were caught swimming naked and everyone realized at the same time. Leading up to the exposé of Three Arrows Capital, a $10Bn crypto hedge fund now alleged to be a Ponzi scheme, everyone thought that the firm employed the smartest traders in the industry. Eventually, the tide went out and investors realized that the 3AC was swimming naked. The founders have essentially disappeared and there are ongoing investigations by the SEC and CFTC.

Snap, poof, gone. Depositors, investors, and creditors were rugged.

The latest domino to fall is FTX, the world’s second largest crypto exchange platform, which filed Chapter 11 bankruptcy on Friday morning, along with its 130+ different subsidiaries. Hailed as the next Warren Buffet, founder & CEO Sam Bankman-Fried has resigned & seen his billionaire status evaporate in less than a week. As I write & edit this report, FTX’s wallets are currently being hacked, rumored to be an inside job, for an amount greater than $600M. Clearly, the story is still developing…

Amazingly, each of these implosions are intertwined and connected through a variety of different avenues. Regardless of how they are intertwined, the magnitude of each implosion continues to grow and the contagion events are becoming more widespread. The purpose of this report is to focus on the causal factor that started the domino effect: Federal Reserve rate hikes & monetary tightening.

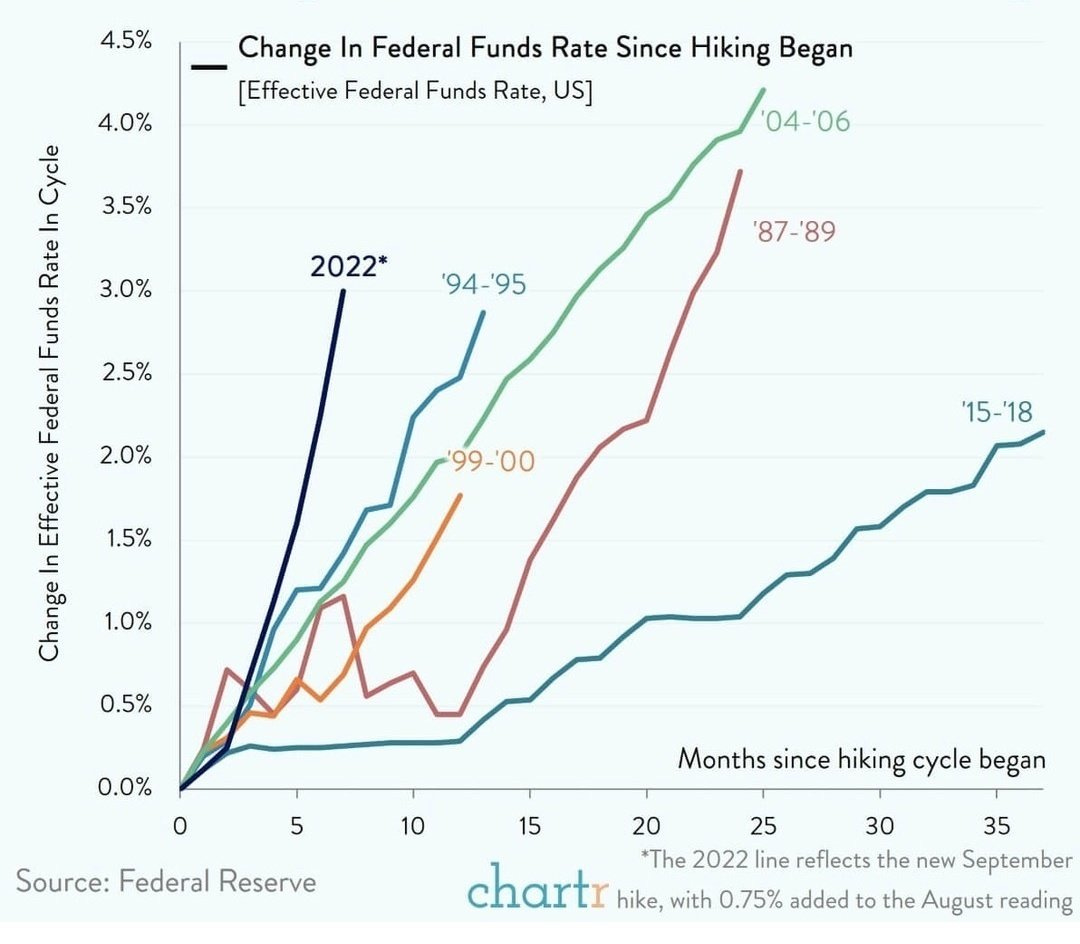

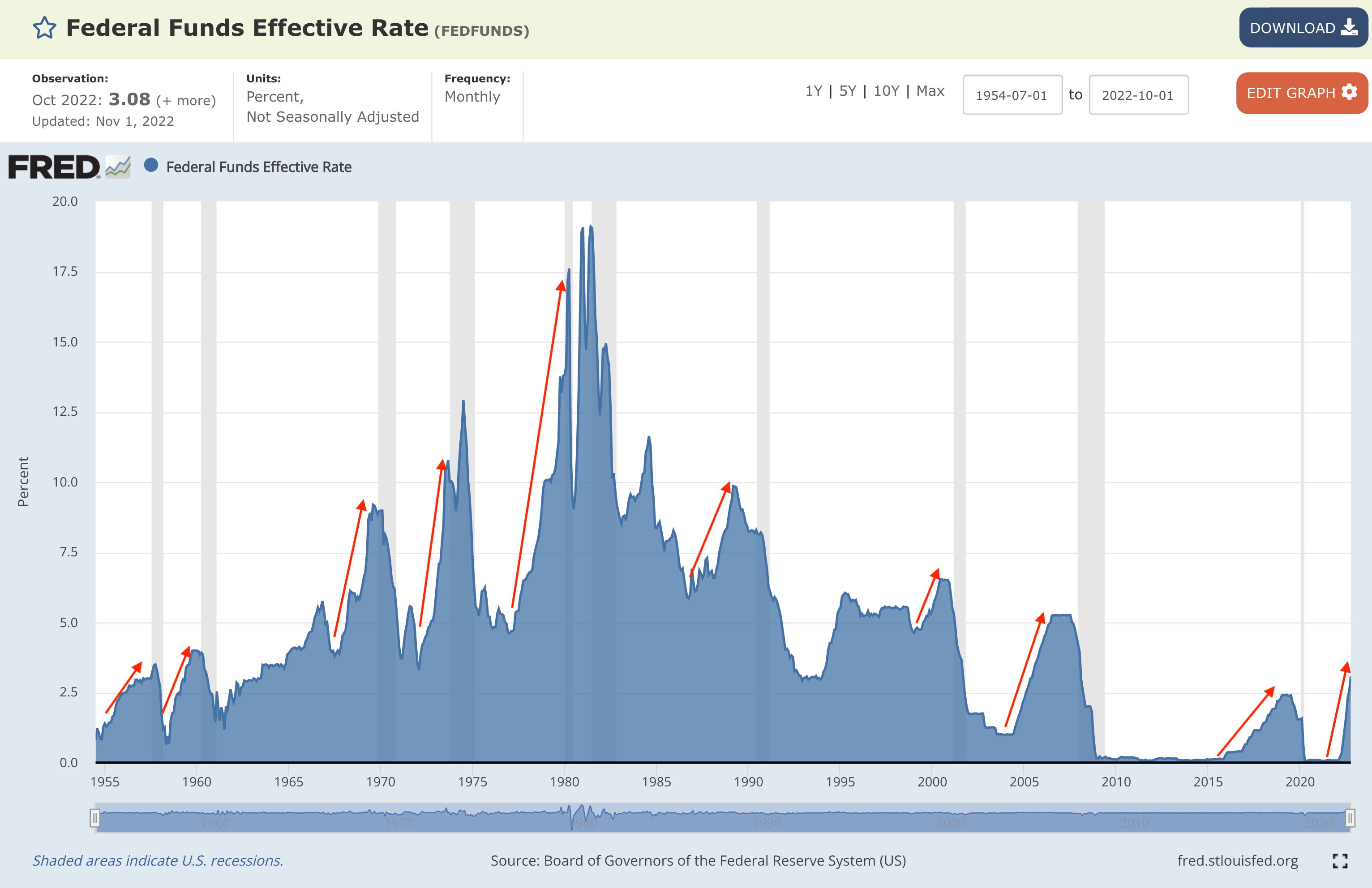

We are realistically seven months into the ongoing monetary tightening cycle, when the Federal Reserve first increased the federal funds rate by +0.25% in March 2022. Since then, we’ve undergone the most rapid tightening cycle in U.S. monetary history. We can prove this with three charts, which amazingly don’t include the Fed’s recent +0.75% rate hike on November 2, 2022:

1. The YoY Percent Change (rate of change) in the Federal Funds Rate: The FFR has increased by +3,750% YoY, as of October 2022, driven by a combination of historically low interest rates in 2021 (base effects) and historic tightening in 2022. We’ve never seen the federal funds rate accelerate by this degree.

2. The YoY Percent (nominal increase) in the Federal Funds Rate: To combat the base effects mentioned in the chart above, the chart below tracks the rolling YoY nominal increase rather than the percent change. This is unequivocally the fastest YoY monetary tightening since the early-1980’s.

3. The speed & magnitude of the current tightening cycle vs. prior cycles: Instead of measuring the YoY rate of change or nominal increase, this chart measures the magnitude of each rate hike cycle starting from the first rate hike of that cycle. Prior cycles don’t compare to the pace/magnitude of the current tightening cycle. As mentioned, this doesn’t include the Fed’s latest +0.75% rate hike, which put the effective federal funds rate at roughly 3.8%.

In each of their unique ways, these three charts provide quantifiable evidence that we’re experiencing one of the fastest rate hike regimes in U.S. history. After years, if not a decade, of historically low interest rates & monetary stimulus, we’re undergoing a rapid unwind of financial risk caused by a rapid increase in interest rates.

Why is this significant? For three primary reasons:

Interest rates & asset prices have an inverse correlation, all else being equal. As rates rise, the discount rate also rises, pushing the present value of future cash flows (aka asset prices) down.

Interest rates ↑ = Asset prices ↓ (all else being equal)

Interest rates ↓ = Asset prices ↑ (all else being equal)

Less monetary stimulus from the Federal Reserve, and outright monetary tightening, drains liquidity out of the financial system. All else being equal, liquidity and asset prices have a positive correlation, all else being equal.

Liquidity ↑ = Asset prices ↑ (all else being equal)

Liquidity ↓ = Asset prices ↓ (all else being equal)

In an artificially suppressed interest rate environment, investors are forced to hunt for yield. When the Fed buys $120Bn worth of Treasuries & mortgage backed securities for 18+ months, yields on these securities plummet. In response, pension funds & institutions who need to generate a yield are forced to generate a return somewhere else. This causes investors to move further out onto the risk curve, investing in higher yielding assets or using leverage on low risk assets. Remember, return is always congruent with risk. Therefore, stripped of their ability to rely on lower risk assets to generate a return, institutions have become conditioned to hunt for yield in riskier assets.

I’d like to focus on this third point for just a moment, because I recently finished a phenomenal book that explores this topic. “The Lords of Easy Money”, by Christopher Leonard, highlights the inner-workings of the Federal Reserve’s management through financial crises & recessions in modern history. The book was published in January 2022, so it includes an analysis & discussion of the monetary policy response to the COVID pandemic as well. Either way, Leonard’s discussion revolves around the former President of the Kansas City Federal Reserve, Tom Hoenig, who is generally viewed as being cautious of quantitative easing & excessive monetary stimulus.

While reading the book, the following quote from Hoenig stood out to me because it appropriately translates to the current macro environment that we’re in today:

“You had seven years of basically zero-interest rates. Now, what happens in an economic system over seven years? The entire market system develops a new equilibrium — around a zero rate. An entire economic system. Around a zero rate. Not only in the U.S. but globally. Now think of the adjustment process to a new equilibrium at a higher rate. Do you think it’s costless? Do you think that no one will suffer? Do you think there won’t be winners and losers? No way.

You have taken your economy and your economic system and you’ve moved it to an artificially low zero rate. You’ve had people making investments on that basis, people not making investments on that basis, people speculating in new activities, people speculating on derivatives around that, and now you’re going to adjust it back?

Good luck, it isn’t going to be costless.”

Amazingly, Hoenig said this in August 2016! Long before the historic monetary stimulus and asset purchases from 2020-2022, Hoenig, then retired from the Federal Reserve, was cognizant of how rate hikes in a post-ZIRP world would create a ripple effect throughout the financial system and the economy.

This brings us full circle to the earthquake & tsunami analogy: the financial system, conditioned by low interest rates, is struggling to cope with a historic acceleration of interest rates. As rates rise and liquidity gets pulled out of the system, the tide is receding and exposing a variety of previously unsuspecting naked swimmers.

Practically no one could’ve foreseen that these individual companies would be exposed at the start of the year, yet here we are. Contagion events in the U.S. have, thus far, been contained within the cryptocurrency industry and have yet to ripple into the traditional financial system. This should be making investors wonder whether or not dominos start to fall outside of crypto. One could argue that the failures in the U.K. bond market was a contagion event stemming from rapid monetary tightening.

To no surprise, the entire crypto market is facing immense pressure upon further FTX revelations & announcements. FTX is likely in the early innings of the implosion, so investors across the industry are scrambling to find answers, reduce risk, and try to avoid whichever domino could fall next. Crypto investors are on alert, and crypto prices are reflecting that. Total crypto market cap declined by more than $240Bn at one point this week, wiping out an immense amount of value. Bitcoin reached new YTD lows and traded below $16,000 for the first time since early November 2020. Crypto projects closely aligned with FTX, like Solana $SOL, fell nearly -50% during Wednesday’s session. The native token of the FTX exchange, $FTT, has fallen more than -91% since last Sunday evening.

The crypto industry is an embodiment of mayhem right now.

With that said, stocks managed to shrug off this entire debacle after Thursday’s impressive CPI report for October 2022. Considering that the FTX situation is solely impacting the cryptocurrency market, I’m not surprised to see stocks & crypto diverge; however, I’m certainly surprised by the magnitude with which stocks are accelerating.

Traditional markets are celebrating after a decisive deceleration in the rate of inflation for the month of October, reporting a headline inflation rate of +7.7%. Median estimates were calling for +7.9% YoY, so the result was warmly received by the market. On a month-over-month basis, consumer prices increased by +0.4% for the second consecutive month, but we saw outright MoM deflation in several categories, including: energy services, utility gas, used cars, apparel, medical care, and commodities less food & energy commodities. Core CPI and trimmed-mean CPI also decelerated, further confirming the idea that inflation is cooling down. With that said, there’s still plenty to go, but it appears that the base effects from last year’s high inflation prints are going to make YoY inflation rates stabilize.

Investors immediately recognized this result as confirmation that the Fed would begin to reduce the pace of their future rate hikes, and potentially pause sooner than expected. Odds of a +0.5% rate hike increased from 50% earlier in the week to 80% today. In turn, stocks ripped higher on Thursday morning & continued to gain momentum on Friday. The Nasdaq Composite experienced its largest 2-day gain since December 2008, largely driven by Thursday’s +7.4% gain. On Friday, it gained another +1.9%, generating a 2-day return of +9.4%.

It feels great to celebrate this win and the subsequent market rally, but I dug further in order to learn more about the implications of such substantial market rallies. I looked at the 20 largest daily gains for the Nasdaq since 1971, which includes Thursday’s gains, then analyzed when/where they happened relative to the bear market lows:

Here are my takeaways from this data:

These powerful days of performance occur in clusters during a bear market, often before the market lows have been reached.

In 15 prior occasions, the market continued to decline substantially.

Only 4 occurred after the lows, in the depths of the Great Recession and the COVID pandemic.

Considering that these momentum thrusts typically occur in cluster, I expect to see more massive up-days in the near future (1 week to 6 months).

Whether or not the market climbs higher or falls lower from here is up for debate, but I think this data tells us that we must expect higher volatility.

The 15 prior occasions where the market continued to decline show that plenty of pain could still be in store. Investors must weigh the risk vs. the reward based on these figures. Ask yourself, am I prepared to experience another -30% drawdown in my equity portfolio? What about -60%? Do the potential upside rewards compensate for these risks?

From my perspective, I remain cautious about this rally, though I expect that it could have momentum to keep rising in the coming days/week ahead. Unfortunately, I feel that this rally will suffer the same fate of all other market rallies in 2022. In 2022 alone, the Nasdaq Composite has now experienced 6 double-digit percentage rallies. It would be 7 if you count the +9.9% gain in mid-February. Each of them failed to produce a sustainable bottom and the market rolled over to create new YTD lows.

What makes this one any different? Once again, the market is speculating that we’ve reached peak hawkishness from the Federal Reserve and that a pivot is around the corner. We’ve heard this story before. The only difference this time around is that we truly have less worse economic news! Specifically, here’s what I’m focused on:

After two consecutive quarters of negative real GDP growth, Q3 2022 real GDP growth was stronger than expected at +2.6%.

We continue to see a strong & dynamic jobs market, with ample demand for labor.

Headline inflation continues to show signs of improvement, but the October data adds more confirmation that the underlying drivers of inflation are moderating & beginning to cool.

Call me crazy, but is the Federal Reserve actually pulling off a soft-landing? The market seems to believe so, emboldened by the appearance of decelerating inflation. From the market’s perspective, the October inflation data gives the Fed permission to “only” raise rates by +0.5% in December. Prior to the data, the market was still debating whether or not the Fed would raise rates by +0.5% or +0.75%. Considering that there’s a higher likelihood of a less substantial rate hike, markets are happy.

My issue is this: even if the Federal Reserve reduces the pace of their rate hikes, they are still raising rates. In turn, this will reduce liquidity, force the “ocean water” to recede further, and potentially expose more naked swimmers. As the tide goes out, we don’t know who will be exposed or how severe of an impact it will have on the broader market.

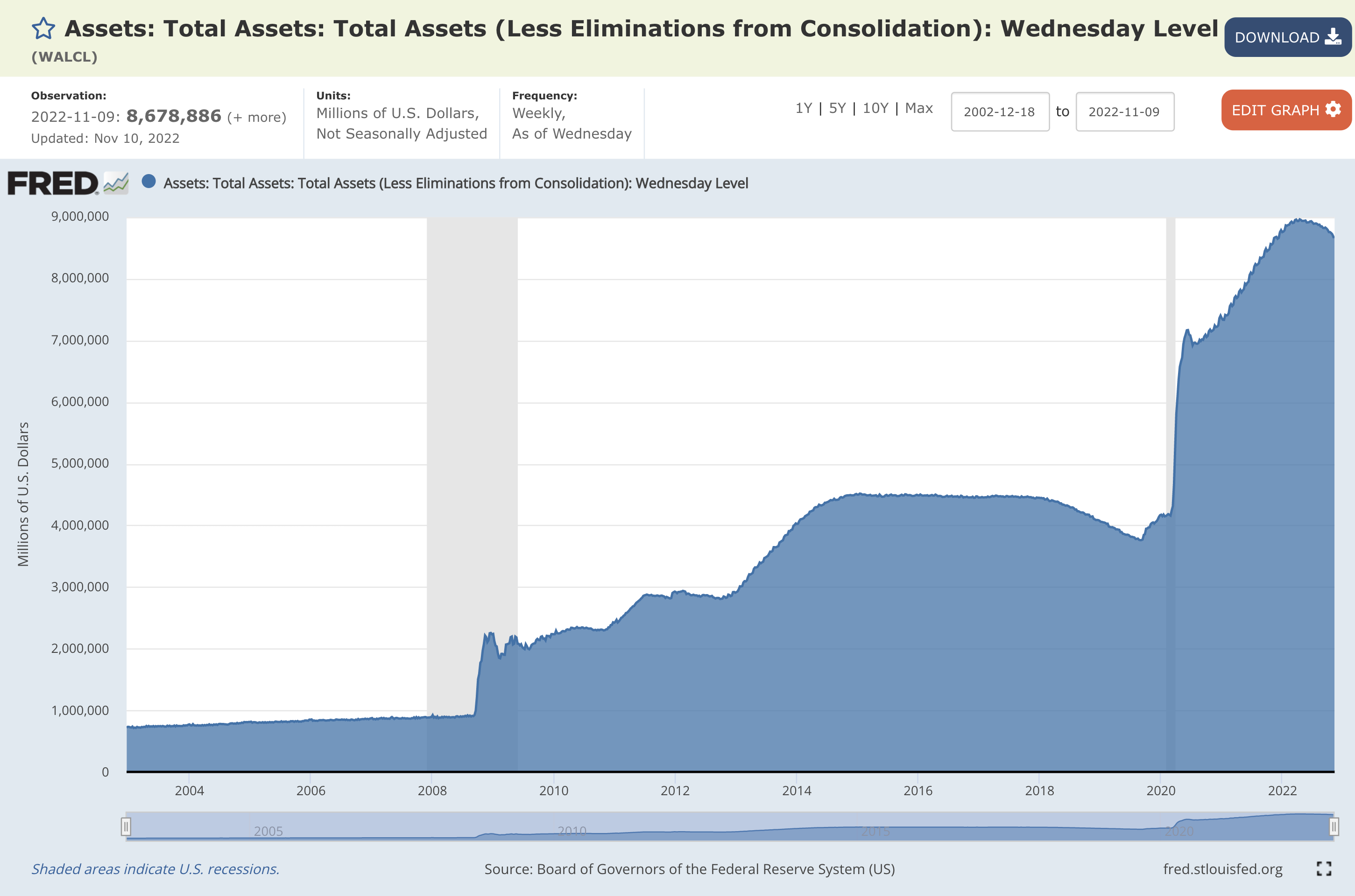

We must also confront the second aspect of monetary tightening aside from raising rates: balance sheet reduction.

Up until now, the Federal Reserve has only moderately reduced the size of their balance sheet. As they accelerate the amount of balance sheet runoff and potentially transition to the outright selling of Treasuries & mortgage-backed securities, liquidity will get drained even further. After peaking at $8.965Tn in April 2022, the Fed currently holds $8.678Tn in assets on their balance sheet. In other words, they’ve only reduced the size of their balance sheet by -3.2%. Relative to the pre-Pandemic level in January 2020, the balance sheet has grown by +109%.

Can they even unwind this? How far can they get? What happens if they try to?

The market will discover these answers over the coming months, and potentially over the next year. Even if inflation continues to moderate, the Fed appears committed to reducing the size of their balance sheet. After a consistent series of rate hikes, the Fed is likely to prioritize balance sheet reduction in the near future, mirroring their strategy in the 2015-2019 tightening cycle. During that time, the Fed steadily raised rates between December 2015 and December 2018, paused for several months, then started to cut interest rates in the latter-half of 2019. In early 2018, the Federal Reserve attempted to reduce the size of their balance sheet. As they embarked on this path, cracks within the traditional financial system began to form in the overnight repo market. The stock market had terrible performance in 2018, with tantrums in Q1 & Q4 that resulted in a -20% drawdown for the S&P 500 in a matter of months.

The point is, we know the Fed’s playbook going forward if inflation normalizes: reduce the pace of rate hikes, pause, accelerate balance sheet reduction, then potentially cut rates. Using 2018 as the experiment, we can see that markets didn’t respond positively to this playbook.

Extrapolating on this, there’s a clear pattern to the Fed’s monetary policy whereby the provide excessive monetary stimulus for too long, then proceeds to tighten monetary conditions too late. Because they start to raise interest rates too late, they are essentially forced to overtighten & course-correct. This overtightening dynamic is subsequently followed by a recession whereby the Federal Reserve proceeds to cut rates, provide monetary stimulus, and repeat the process over again.

Hike into a recession, then stimulate to get out of it.

From my perspective, we are unequivocally in the phase where the Fed overtightens until we experience a major break down in the structural economy/financial system. While it’s possible that the Fed is able to successfully engineer a soft-landing, we’re seeing cracks across the crypto ecosystem, which could be foreshadowing further cracks in the traditional financial system. Even if these contagion events stay contained within crypto, it’s very possible that more dominoes are due to fall.

All I do know is that the tide is going out, we’re seeing who’s swimming naked, and perhaps the biggest waves of the tsunami have yet to arrive on the shore.

Best,

Caleb Franzen

Massive shoutout to several other analysts & writers on Substack! I truly appreciate your support:

who writes

who writes

who writes

who writes

I’d highly recommend that you check out each of their newsletters, as they produce top-notch analysis & market commentary in their respective & unique ways.

DISCLAIMER:

My investment thesis, risk appetite, and time frames are strictly my own and are significantly different than that of my readership. As such, the investments & stocks covered in this publication are not to be considered investment advice and should be regarded as information only. I encourage everyone to conduct their own due diligence, understand the risks associated with any information that is reviewed, and to recognize that my investment approach is not necessarily suitable for your specific portfolio & investing needs. Please consult a registered & licensed financial advisor for any topics related to your portfolio, exercise strong risk controls, and understand that I have no responsibility for any gains or losses incurred in your portfolio.

Great article, I like the 2018 throwback to the Fed's playbook in 2018: It just doesn't make sense to me that the market thinks it's a pivot when we think about the balance sheet and the work the Fed still has to do on that.

Also thank you for the shout-out!

Very good. Thanks! I longed on Thursday, but I stay cautious. (Btw, I have worked several years on the question of how metaphors can be models or function as models. That would have been a very good example!)