Stocks Don't Do This In Bear Markets

Investors,

Q2 2023 has concluded, giving us an opportunity to reflect on the path we’ve walked.

Over the past three quarters, the S&P 500 has produced the following returns:

Q4 2022: +7.08%

Q1 2023: +7.0%

Q2 2023: +8.3%

Call me crazy, but stocks don’t consistently trend higher during bear markets. The bear market in 2022 evolved into a bear market rally in Q1 2023, which evolved into a new bull market in Q2 2023. That’s how it works folks.

Looking at the S&P 500 with quarterly candles, we see the following historical trend:

The three quarterly candles we’ve just witnessed are not (I repeat, ARE NOT) characteristic of a bear market. This behavior didn’t exist in 2000-2003 or 2007-2008. Not even during 2020’s COVID collapse, given the rapid nature of the decline/recovery.

In fact, looking at the end of the recessionary bear markets and the dawn of the new bull market, each of those periods had at least three consecutive quarters of positive returns! Their 3-quarter returns were quite strong, representing strong investor conviction and increasing momentum. I’ve highlighted each of these periods in teal, which correspond with the following dates & returns:

April 2003 - December 2003: +31%

April 2009 - December 2009: +40%

April 2020 - December 2020: +50%

In the current streak of positive 3-quarter returns, the S&P 500 has netted +23%.

Therefore, we can actually say that the current market environment is much more contained/reasonable/justifiable than prior births of a new bull market. I fear that bears will look at this data and interpret it differently, arguing that “lower returns in this regime reflect a weak new bull market, which likely means that this isn’t a new bull market”.

To each their own.

All I know is that over the course of the past 8 weeks, we’ve seen a wide range of stock market participants trending to new 20-day, 50-day, and 52-week highs. Even the industrials sector hit new 52-week highs (again) on Friday, up +9.3% YTD. The Dow Jones had the highest daily close of 2023 on Friday. The S&P 500 reached & closed at new YTD highs on Friday. Same with consumer discretionary stocks.

Oh, the Nasdaq-100 is also up +39% YTD & McDonalds MCD 0.00%↑ hit new ATH’s.

Stocks, across a wide range of sectors and market caps, continue to produce higher highs and higher lows for the past 8 months, while producing more new highs than new lows on short, medium, and long-term timeframes.

That is not indicative of a bear market. It simply isn’t.

In the remainder of this report, I’ll cover:

Macro: More disinflation in new PCE data & housing market declines.

Stock Market: Long-term visualization of stock market returns.

Bitcoin: BTC shrugs off SEC’s request for spot ETF re-applications.

First, I want to thank MicroSectors for their continued support of Cubic Analytics and encourage everyone to follow the great data that they’re posting on Twitter!

Macroeconomics:

I’ve been of the opinion that inflation will continue to decelerate since December 2022, upon release of the November 2022 CPI data. In other words, disinflation was the trend and the likely trend going forward. To expand on this point, I made it clear that inflation (a rate of change of prices) had peaked, but prices themselves (a nominal value) had not peaked.

Month after month, this thesis has been proven correct.

While Team “Sticky Inflation” has fear-mongered about Core CPI Services, energy & agricultural commodities, and even car insurance prices (yes, really), the broad baskets of consumer and producer goods/services have been reflecting disinflation.

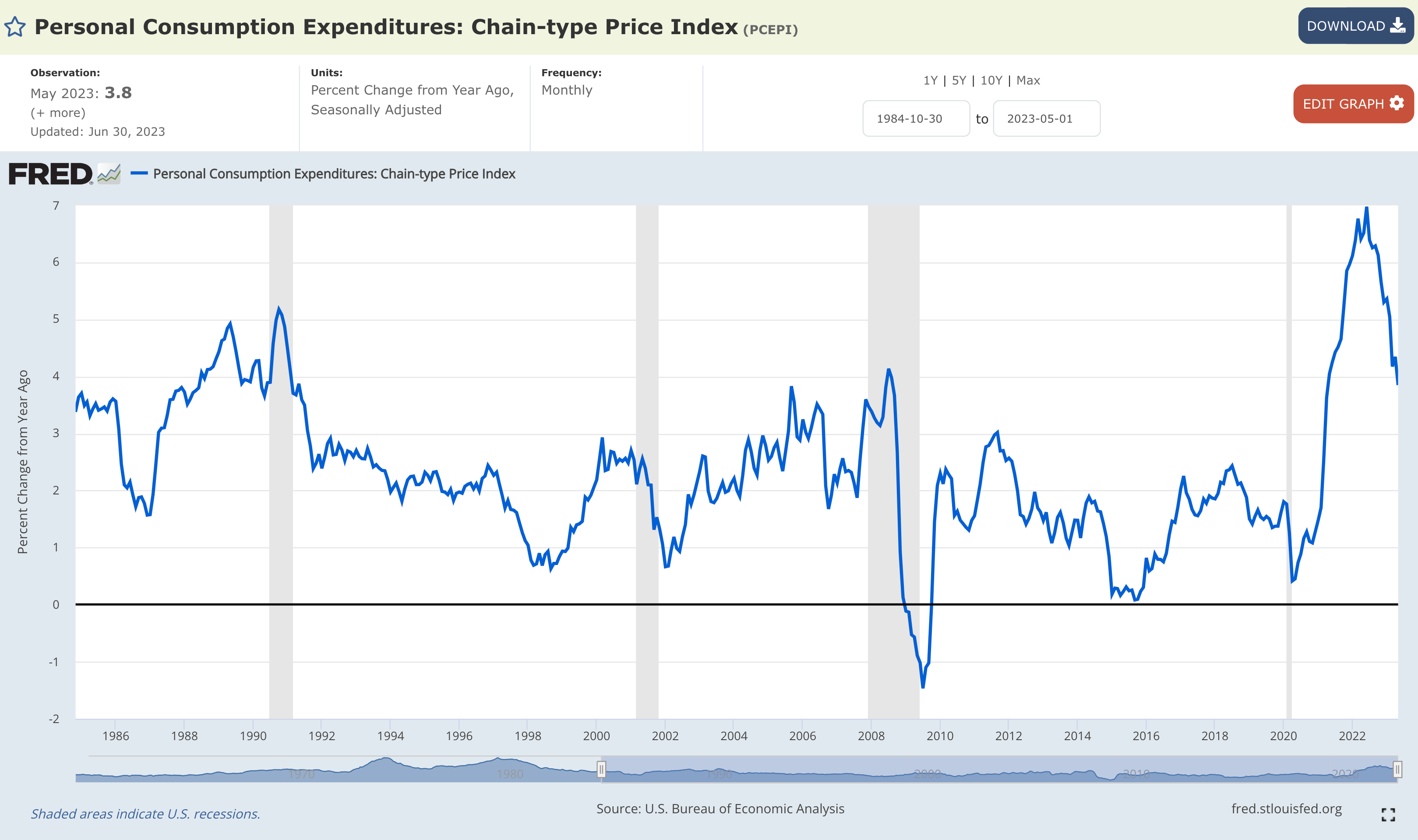

Even the Federal Reserve’s preferred methodology for measuring inflation, the Personal Consumption Expenditures: Chain-Type Price Index, continues to reflect disinflation (prices rising at a slower pace) back towards the historic trend. More specifically, the May 2023 data showed a year-over-year increase of +3.8% vs. the April result of +4.34%.

This measurement is now at its lowest point since April 2021, with one key difference:

In April 2021, the YoY PCE measurement was accelerating higher. Today, it’s clearly decelerating. Still, Team “Sticky Inflation” is not pleased and saying the following:

“But Core PCE YoY is still +4.6%”

Yes, it’s at +4.6%. That’s marginally lower than the prior month result of +4.7% and unequivocally lower than the peak in February 2022 of +5.4%. Regarding this argument, my pushback is that we shouldn’t let “perfect” be the enemy of “good” and therefore recognize that progress is being made. That’s sentiment I’ve been sharing quite often this year, which has turned out to be a great perspective.

My view is that inflation will continue to decelerate and that disinflation will continue to become increasingly apparent for the remainder of 2023. If you want to know more about why I believe this, I suggest you read my Twitter post where I highlighted the key components of this outlook.

One of those key components is that real-time measurements of Shelter (housing prices and rents) continue to decelerate on a YoY basis. In fact, the latest data for the S&P Case-Shiller National Home Price Index was published this past week, showing a YoY decline of -0.24% in April. While this is a modest contraction, it’s a stark difference vs. the result of +20.8% in both March and April 2022.

Said differently, it took one year for the rate of change to decline from +21% to ±0%.

Imagine how significantly this will impact disinflation within the overall CPI, of which Shelter accounts for 35% of the CPI weighting, over the next 6-12 months! Given that Shelter lags real-time housing/rental market data by 8-12 months, this creates significant momentum for disinflation going forward. Are housing/rental prices still high today? Absolutely. However, with respect to inflation, they are rising at a slower pace (or even contracting). That’s all that matters with respect to calculating YoY inflation readings, which is what the Fed targets with their 2% goal.

Stock Market:

If you made it this far, I truly appreciate your continued support. As a way to celebrate the fact that the S&P 500 is up roughly +15% YTD, I’m currently offering a 15% discount for premium memberships to Cubic Analytics.

You can sign up using the link above to apply the discount!

Stocks had an excellent bounce-back week after the prior week’s losses. In total, the S&P 500 gained +2.33% vs. the prior week’s loss of -1.4%. As a result, the index had the highest daily, weekly, and monthly close since March/April 2022.

Not too shabby.

I saw a great post from

on Twitter showcasing the cluster of positive vs. negative calendar year returns for the S&P 500 going back to 1928:

This data has a few key takeaways, but one stands out to me in particular: It’s quite rare for the U.S. stock market to experience consecutive down years.

Using this data, I count 31 years where the U.S. stock market had a negative return. Only 7 of these instances were followed by another loss in the next calendar year. Statistically, this means that 22.5% of negative years were followed by a subsequent loss in the next calendar year. We can rephrase this in a more bullish conclusion that 77.5% of negative calendar year returns were followed by a year of positive returns.

Wow.

This reminds me of the data that I shared in my 2023 outlook, highlighting the distribution of calendar year returns (including dividends) for the S&P 500:

I clustered the histogram to group calendar year returns by 10%, which shows that the market generally tends to produce solid gains over time, despite short-term deviations of negative returns. In other words, the U.S. stock market is unequivocally the greatest long-term creator of wealth in history, regardless of the volatility that might happen this year or next.

Compounding truly is the “eighth wonder of the world”, as Albert Einstein said.

Bitcoin:

The apex digital asset looks good. Really good.

Despite news on Friday that the SEC found recent spot Bitcoin ETF’s by BlackRock, Fidelity, WisdomTree, Invesco, Ark Invest, and VanEck to be “inadequate”, Bitcoin is still trading at $30,600. In fact, all of the institutions named above have already re-filed their applications in accordance to the SEC’s comments. Given the rapid turnaround & response times, my immediate reaction is that the “inadequacies” were quite minor; otherwise, they likely would have required more time to be resubmitted.

I think it’s important to note the following, which I shared on Twitter on Friday:

Bitcoin is up +85% YTD, down roughly -55% from the ATH’s in November 2021.

I was on the right side of the downtrend for the majority of 2022 and I’ve been on the right side of the uptrend in 2023. While I was unfortunately too short-term bearish at the end of 2022, I was able to stack BTC during the 3rd quarter of the year and have continued to be a buyer in 2023. My entries haven’t been perfect, but I’ve been able to achieve my goal of steadily increasing my allocation to Bitcoin over time.

Thankfully, I backed up the truck while Bitcoin was retesting the 200-week and 200-day moving average clouds, which I continued to share in real-time both on this newsletter and on Twitter. I will adhere to the DCA strategy that I outlined in this March 31st post. In other words, I will be waiting for the next 10% decline before allocating another 10% of my cash position into BTC.

Best,

Caleb Franzen

SPONSOR:

This edition was made possible by the support of MicroSectors, a financial services and investment company that creates an array of unique investment products and ETN’s. Their NYSE FANG+ products are the only one of their kind, allowing investors to gain exposure, leveraged/un-leveraged and direct/inverse, to the NYSE FANG+ Index. They have a suite of products ranging from big banks, to oil and gas, and even gold/gold miners. I’m currently using two of their products, GDXD -0.81%↓ and OILD 0.80%↑ as short-term trades to bet against gold miners and energy stocks!

I started a partnership with MicroSectors because I’ve been using their products for over a year and this was an organic and seamless fit with my views.

Please follow their Twitter and check out their website to learn more about their services and the different products that they offer.

DISCLAIMER:

This report expresses the views of the author as of the date it was published, and are subject to change without notice. The author believes that the information, data, and charts contained within this report are accurate, but cannot guarantee the accuracy of such information.

The investment thesis, security analysis, risk appetite, and time frames expressed above are strictly those of the author and are not intended to be interpreted as financial advice. As such, market views covered in this publication are not to be considered investment advice and should be regarded as information only. The mention, discussion, and/or analysis of individual securities is not a solicitation or recommendation to buy, sell, or hold said security.

Each investor is responsible to conduct their own due diligence and to understand the risks associated with any information that is reviewed. The information contained herein does not constitute and shouldn’t be construed as a solicitation of advisory services. Consult a registered financial advisor and/or certified financial planner before making any investment decisions.

This report may not be copied, reproduced, republished or posted without the consent of Cubic Analytics and/or Caleb Franzen, without proper citation.

Please be advised that this report contains a third party paid advertisement and links to third party websites. These advertisements do not constitute endorsements and are not necessarily representative of the views or opinions of the newsletter author. The advertisement contained herein did not influence the market views, analysis, or commentary expressed above and Cubic Analytics maintains its independence and full control over all ideas, thoughts, and expressions above. The mention, discussion, and/or analysis of individual securities is not a solicitation or recommendation to buy, sell, or hold said security. All investments carry risks and past performance is not necessarily indicative of future results/returns.