Key Trends You Need To Know

Investors,

Recession predictions sound louder than ever, particularly as stocks faced pressure on labor market data that was either softer than expected or softer than prior results.

However…

I find it difficult to see an imminent recession when same-store sales growth is running at +6.3% YoY and steadily trending higher for the past 12 months, according to the latest results of the weekly Redbook Index:

As we can see from the chart above, the result of +6.3% matches the result from November 2023, which is the highest reading since December 2022.

The difference between today’s result compared to December 2022 is that retail sales growth is accelerating vs. the constant & steep deceleration in 2022 (and H1 2023).

The good news is that nominal growth of +6.3% is drastically outpacing inflation.

For example, if we strip out the Shelter component from CPI (because it’s not a retail spending item), then the latest inflation data is running at +1.7% YoY. While this is a simple way to estimate what retail inflation is, it provides a clear conclusion that real retail sales growth (nominal sales growth adjusted for inflation) is likely somewhere between +3% and +4% YoY. In this particular case, using these datapoints, the real growth for the Redbook Index is +4.6% YoY, which is far from recessionary.

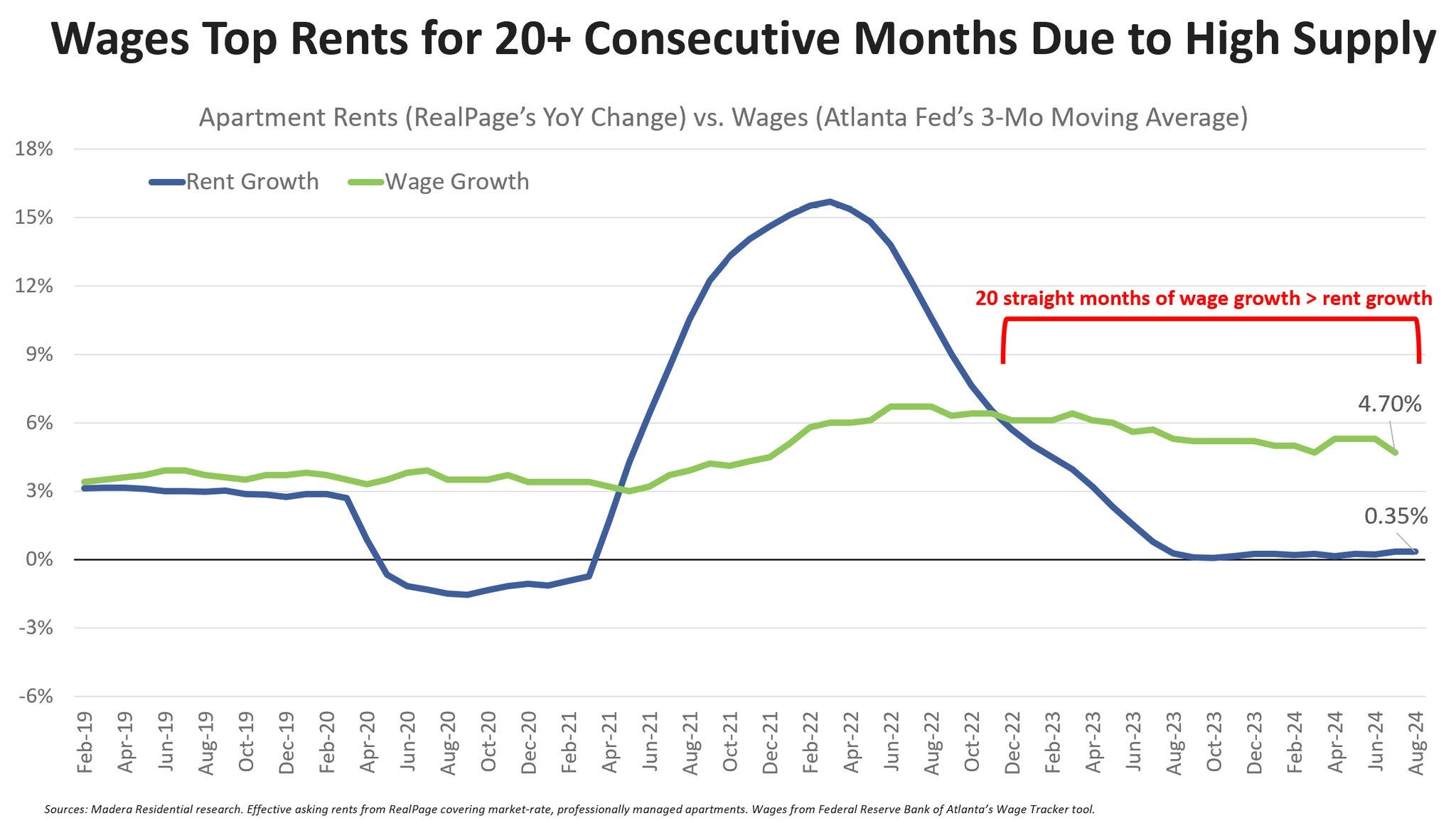

Speaking of inflation-adjusted data, I thought this chart of average hourly earnings vs. rent inflation was very interesting, now showing 20 straight months of real gains!

Even if we use the average hourly earnings growth from the latest NFP data, which came in at +3.9% YoY, nominal wages are still outpacing rent inflation. This suggests that U.S. workers are experiencing experiencing real wage gains.

The ongoing expansion isn’t perfect… there are weak aspects and strong aspects.

There are strong aspects that are weakening.

There are weak aspects that are strengthening.

This is what makes macro so confusing and difficult for investors to understand.

But hey, maybe we aren’t in an expansion… but as investors, do we need to be in a strong expansion to produce strong returns?

Maybe not.

At the very least, it’s clear that we aren’t in a recession or an outright contraction.

My view has been that the economy, the labor market, and the consumer are resilient & dynamic, which is going to persist amidst some modest & steady softening.

Throughout 2024, this has been the correct theme.

I expect this will continue, amidst a disinflationary environment with steady softening.

In the remainder of this premium report, I’m going to expand on last week’s analysis on value stocks, particularly on a relative basis, and highlight the key market dynamics that I’m focused on as we go into the upcoming week.

At the end of the day, the macro picture is important but merely to set the stage.

The way that I’ve been able to stay on top of the market trend over the past several years has been due to my focus on price action, the internal dynamics within the market, and using statistical indicators to identify the best way to position myself as an investor.

These reports are the way that I document & share what’s important to me and the different opportunities (or the lack thereof) that I’m seeing in the market.