Investment Outlook for 2022

Macroeconomics, Stock Market Returns, and Twenty-Two Stocks for 2022

To investors,

On the first trading day of 2021, I published my investment outlook for the year to discuss how we got “here” and where I thought the market was going. With 2021 coming to a close, I think it’s safe to say that the macro perspectives in that report gave investors an excellent roadmap for navigating the market in 2021. As we enter 2022, there are an entirely new set of questions and uncertainties around the markets, particularly in light of historic inflation levels. This investment research paper is not intended to break down those uncertainties or to review the economic developments of 2021, but rather to discuss my outlook for 2022 as monetary policy dynamics and macroeconomic data unfold. The goal of this paper is to briefly review 2021 market returns, reconcile them against the outlook I published at the beginning of the year, discuss the data & principles guiding my outlook for 2022, and then highlight the individual stocks that I think are primed to have strong returns in the upcoming year.

How We Got Here (2021 Recap):

2021 was an undeniably strong year for U.S. stocks, seeing each of the major indexes climb higher by substantial amounts. The calendar year returns for the major U.S. indexes were:

• Dow Jones Industrial Average ($DJX): +18.7%

• S&P 500 ($SPX): +26.9%

• Nasdaq-100 ($NDX): +26.6%

• Russell 2000 ($RUT): +13.7%

It’s amazing to see such an extensive follow-through move after an extremely impressive year for stocks in 2020. The S&P 500 has now gained +47% since January 1, 2020 and a remarkable +117.5% since the March 2020 lows. The average return of the S&P 500 over the prior twenty-five years is +11.2%, therefore 2021’s return of +26.9% is significantly above average. More specifically, 2021 falls in the top 80th percentile of calendar year returns over the past twenty-five years. The S&P 500 extended to new all-time highs seventy times in 2021, the second highest calendar year output in history. With a maximum drawdown of -5.2% between 9/2/21 and 10/4/21, it’s evident that the market consistently overcame adversity in 2021. Unequivocally, U.S. equities had a stellar year in the context of its historical performance.

I think it’s important to highlight the most significant risks that the market faced during the year, as a reminder that stocks have continued to overcome negative and adverse events. Here were some of the headline topics that caused markets to react to the downside, in no particular order:

• Suez Canal blockage

• Yield tantrum

• Government debt ceiling

• Infrastructure bill headwinds

• COVID-relief headwinds

• Delta/Omicron variants

• Evergrande default

• Federal Reserve tapering schedule

• Historic inflation (39-year high)

• Meme stock exuberance

• January 6 Capitol riot

• Afghanistan withdrawal

This should serve as a reminder that stocks perform at their best when they climb a wall of worry, which is precisely what I said in my paper last year. Despite continuous headwinds & uncertainties throughout the year, the market was able to consistently generate higher highs and higher lows. By very definition, the market is in an uptrend.

In the outlook that I published at the start of 2021, I expressed clear expectations and conditions for my optimism:

“The stock market in 2020 was both rational and irrational in a bullish manner. As we look forward to 2021, I strongly believe that this sentiment will continue. More specifically, this belief is contingent on two separate factors: that the Federal Reserve maintains its existing level of asset purchases & continues to grow the balance sheet, and that the vaccines/COVID treatments are efficacious. I believe both of these factors are highly probable.”

Both of these contingencies were met, as I had suspected. The Federal Reserve continued to purchase their target of $120Bn/month in government Treasuries & mortgage-backed securities (MBS) for the first 10 months of the year, and then announced their $15Bn/month tapering schedule in early November. Additionally, strong consumer trends persisted and economic activity increased amidst a reopening economy adapting to the virus. We saw plenty of irrational behavior when Gamestop, AMC, and other highly shorted stocks got squeezed to unpredictable levels. We also saw plenty of rational behavior when the darlings of 2020 (Zoom, Peloton, Roku, Teladoc, Twilio, and others) got re-priced as Treasury yields rose.

While I didn’t give a return target for 2021, I was extremely clear about my bullish perspectives:

“With a clear understanding of how a low interest rate environment has been accretive to equity returns, I retain an overweight position for equities in 2021, especially with the consideration that U.S. interest rates will most likely remain at/near the zero-bound over the intermediate future.”

Indeed, the federal funds rate did remain in the target window of 0.00% to 0.25%, enabled by the Federal Reserve’s historic asset purchases and monetary stimulus. In last year’s paper, I outlined the clear correlation between monetary stimulus and stock market returns as the primary justification for my bullish outlook in 2021. It’s safe to say that the correlation, which I continue to argue is more of a causation, has been an effective guide to forecast asset returns. The Federal Reserve purchased $120Bn/month in assets, providing ample liquidity for financial markets to thrive. My understanding of the monetary policy environment is exactly why I thought it was worthwhile to have an overweight position for U.S. stocks in 2021. This phenomenon was not unique to U.S. stocks, as real estate, cryptocurrencies, and commodities all soared to record or multi-year highs in 2021. All in all, monetary stimulus was accretive to most asset prices.

Where We’re Going (2022 Outlook):

Since 2015, I’ve had a bullish outlook on U.S. equities as we enter the upcoming calendar year; however, this is the first year where I’m taking a more apprehensive stance in my outlook. My decreased optimism shouldn’t be misconstrued as saying U.S. stocks and asset prices will crash in 2022, as I certainly don’t believe that will be the case. I believe the likely case scenario for 2022 is for below-average returns for the S&P 500. Considering that the average annual return for the S&P 500 in the post-WW2 period is +12.5%, I think the most likely case is a return between -5% to +12% in 2022. While I believe that this is the most likely case scenario, I will also touch on a caveat that could result in better than expected returns.

Forecasting market dynamics & returns can be a futile game when played in absolutes. The smartest investors in history instead forecast returns through probabilistic measurements and outcomes. They allocate in favor of those assessments and remain flexible as the odds change in favor of other possibilities. That is the approach I’m taking in my outlook for 2022. Generally, my assessment of the probabilities for 2022 returns is the following:

• Stale Returns: 70% chance of below-average returns, specifically between -5% and +12.5%.

• Bull Market Returns: 20% chance of above-average returns, greater than +12.5%.

• Risk-off Consolidation: 10% chance of poor returns, worse than -5%.

Nothing is concretely certain in financial markets; however, the market appears to have unanimous consensus that monetary stimulus will wane in 2022. We’ve already transitioned from extreme monetary stimulus to a decelerating monetary stimulus, and it seems that we’ll reach a new inflection point in 2022 with monetary tightening. After more than 18 months of historic monetary stimulus, the Fed recently began reducing their asset purchases in November 2021 and are expected to tighten monetary policy in the second half of 2022. More specifically, the current median projection is for three interest rate hikes in 2022. The Fed is walking a metaphorical tightrope regarding monetary policy – carefully trying to maintain the economic expansion while simultaneously combating inflation. Based on their framework of economics and monetary policy, this will be an extremely tough balancing act. The Federal Reserve’s framework states that tightening monetary policy and contracting the money supply will produce higher interest rates and slow down economic activity, which will therefore reduce inflation. With inflation at 39-year highs, the Fed has signaled that they are prepared to take the necessary steps to combat inflation while aiming to minimize the negative externalities and economic repercussions.

One of my favorite quotes about investing is: “Don’t fight the Federal Reserve”. While it may seem elementary to use the Fed’s expected monetary policy actions as the guiding principle for my market outlook, it’s proved to be extremely effective. The rules of this framework are simple:

• Remain overweight U.S. equities and dollar-denominated assets in periods of monetary stimulus and expansion of M2.

• Shift towards caution as the Federal Reserve reduces their rate of asset purchases and begins to transition into a period of monetary tightening (stagnant/contracting M2).

• De-risk during periods of blatant monetary tightening, reducing exposure to tech and emphasizing strong cash flows, profitability, dividends, and share buybacks. Note that de-risk doesn’t mean to sell everything, but simply to shift allocations.

I believe we are currently in the second category, with a strong chance of entering the third category by the end of 2022. As a result of this framework, I’m reducing my optimism for U.S. stocks in 2022, most appropriately described as cautious optimism. In the event that monetary policy remains accommodative for longer than we currently expect, I believe asset prices could continue to generate stronger-than-expected returns. Conversely, if the Fed is forced to tighten monetary policy more hastily, caused by relentless inflationary pressures, I believe asset prices could face worse-than-expected returns.

To substantiate this outlook, it’s vital to evaluate the relationship between the S&P 500 and M2 money supply. In doing so, we can actually see the relative performance of one variable vs. the other. In the graph below, we can see this relationship by dividing the S&P 500 by M2:

As we can see, the ratio between these two variables is roughly equal to the pre-pandemic level, implying that the S&P 500 and M2 have increased at roughly the same rate since January 2020! Priced in M2, the S&P 500 has only risen +2.3% since January 2020 compared to a raw return of +47%.

I want to be clear that I don’t believe the S&P 500’s success over the past 24 months is entirely attributable to the Fed’s monetary stimulus. Stock prices have benefitted from plenty of fundamental catalysts, such as record nominal earnings, strong revenue growth, and flourishing balance sheets. Despite these fundamental improvements, which have expanded valuations, I do believe that the Fed’s monetary policy deserves the lion’s share of the credit. Very quickly, let me explain why I believe this to be true through the following analogy:

Suppose you own an apple orchard and want to increase the output of apples harvested each year. While you could potentially use better soil or switch to genetically enhanced seeds, let’s imagine that you receive a subsidy to buy more land and double the number of apple trees in your orchard. This investment would require little to no cost because the subsidy would be used to expand capacity. At the end of the next harvest, you were able to produce twice as many apples as a result!

It’s necessary to acknowledge that the doubling of your orchard was the primary determinant for the increased yield. The trees in your orchard weren’t individually more productive, given that the output of apples is correlated to the number of trees in the orchard. Additionally, the expansion required little to no cost because the subsidy was used to buy the land and the apple trees.

This example is analogous to how the Federal Reserve creates money out of thin air via monetary stimulus (subsidy to expand farming capacity), resulting in increased asset prices (apples) that grew linearly to the increased money supply (apple trees). If the price of stocks is measured in dollars, and the amount of dollars increases, it’s logical to expect for the dollar-cost of stocks to rise in a proportional fashion. This is why the S&P 500 is only marginally higher by +2.3% when measured against the increase in the money supply.

As further evidence that liquidity and monetary policy help drive stock market returns, here’s how the relationship between these variables has evolved since the start of 2020:

Generally, we can see that these variables have a similar rate of change and are growing in a similar fashion. Some skeptics may criticize that this is a small sample, however, this isn’t a new phenomenon and it isn’t exclusive to the United States! Last year, I showed the following chart to highlight the correlation between global liquidity and the MSCI World Index, spanning between 2015-2020:

As global liquidity rises, driven by stimulus from the major central banks, asset prices have risen in lockstep. When global liquidity began contracting in 2018, the MSCI World Index similarly contracted and faced downside pressure. When global liquidity started to increase in December 2018, the MSCI World Index started to accelerate higher.

• Monetary Stimulus ↑

• Liquidity ↑

• Interest Rates ↓

• Asset Prices ↑

Considering that monetary stimulus in the U.S. is waning, and then expected to transition into monetary tightening, I expect to see the S&P 500 produce a below-average return in 2022. However, a deceleration in monetary stimulus doesn’t guarantee a deceleration in stock market returns. There have been recent years where U.S. stocks had strong returns during periods of monetary tightening. For example, the Federal Reserve hiked rates for the entire calendar year in 2016 and 2017, yet the S&P 500 had returns of +9.5% and +19.4%, respectively. This is why I’m leaving the door open for a double-digit positive return in 2022.

In 2018, as the Fed continued to raise interest rates, the stock market became shaky and delivered an annual return of -5.3%, pushed lower by a -20% drawdown between October and mid-December. Therefore, it’s important to note that we’ll need strong fundamental catalysts for the S&P 500 to produce above average returns this upcoming year. One of the primary catalysts that prompted strong returns in 2016 & 2017 was the deregulation and tax cuts that took place under the Trump presidency. Like it or not, these policies helped to create tailwinds for asset prices, particularly in an economy with historically low unemployment, minimal inflation, a resurgence in business optimism, and strong consumer trends.

As we enter 2022, the critical questions for the economy and financial system seem clear:

• Will the 12-month CPI inflation rate, currently at +6.8% as of November 2021, continue to accelerate throughout 2022 or will it begin to abate and return towards the long-term target of 2%?

• Will the Federal Reserve need to raise rates more substantially than the market currently anticipates to ward off inflationary pressures, and how will markets respond?

• Will supply chain bottlenecks, port backups, and shortages persist or get resolved?

• Will geopolitical issues in the Middle East, Russia/Ukraine, China/Taiwan/Hong Kong, and North Korea increase or remain relatively muted?

• Will internal political disagreements create additional roadblocks for policy & potential stimulus? Midterm elections in 2022 could shake things up.

The risks presented by these questions are extremely nuanced, and several of them are intertwined. Risk is merely an assessment of uncertainty, therefore it’s a two-sided coin. While the questions above pose various threats to markets, we must also consider the potential for these risk-events to have surprisingly positive outcomes. These positive outcomes could cause asset prices to rise as those uncertainties subside.

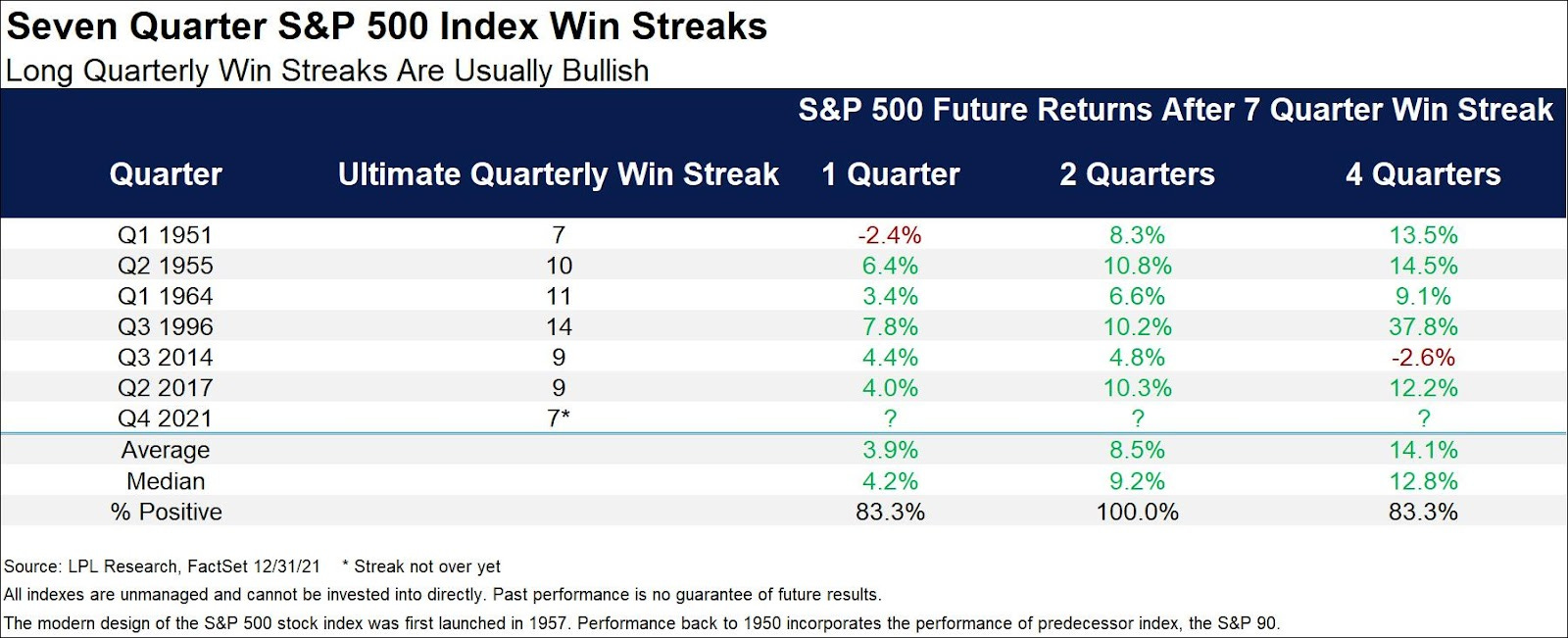

Additionally, markets can be path-dependent, meaning that momentum and investor psychology can be extremely correlated to future returns. Ryan Detrick, the Chief Market Strategist of LPL Financial, recently shared compelling data about the S&P 500’s ability to use momentum to produce strong future returns:

With 2021 officially coming to a close, the S&P 500 has officially produced seven consecutive quarters of gains, a rare accomplishment. In the past, this milestone has produced very strong returns over the subsequent four quarters, with an average return of +14.1% over that time period. Albeit the small sample size, this could provide investors with a sense of encouragement for the upcoming year.

In last year’s paper, I said that the market performs at its best when it climbs a wall of worry. As I mentioned at the beginning of this paper, the market was able to overcome a variety of risk events that seemed to pose significant risks to the global economy, U.S. economy, and financial markets. In each case, those risks were resolved and the market continued to make ATH’s. These negative risks almost always act as fuel to push the markets to new highs. As such, I would not be surprised to see the S&P 500 continue to make all-time highs in 2022.

Top Stocks for 2022:

I’ve spent a considerable amount of time consolidating the 1,000+ stocks I research and track into a concise list of potential winners. After much deliberation, I’m highlighting twenty-two stocks within four categories that I think will provide the best downside risk in a consolidating market, but retain strong upside momentum if the market continues to grind higher. Each of those stocks have an established track record of profitability while still being able to produce above-average revenue growth. Many of these stocks pay dividends, have approved significant share buyback programs, and hold substantial amounts of cash on their balance sheets.

I would classify all of these companies as mature businesses that toe the line between value and growth. As such, I think they will outperform in a market environment that prioritizes either value or growth stocks. Aside from conducting a deep-dive on their financials and business outlook, I considered a handful of qualitative factors in my selection process. First and foremost, I wanted leaders within their respective industries & sectors. Leaders have an established moat around their business model, have experience navigating supply chain issues (if applicable), and their stock typically outperforms their industry peers. They are essentially the “North Star stock” in their industry.

Considering that the Fed is decelerating their monetary stimulus and will likely begin raising rates in 2022, I want to prioritize stocks that have a track record of performing well during various monetary policy environments and are less rate-sensitive than pure tech or growth stocks. As such, I’m not trying to find the next Apple, Microsoft, or the stock that could gain 10x in the upcoming year. That would put me too far out on the risk curve during a period where monetary stimulus is being withdrawn. Without further delay, here are the four investment groups and my twenty-two favorite stocks as we enter 2022, in no particular order:

1. Mega-Cap Technology:

• Apple ($AAPL) - Technology & Consumer Products

• Microsoft ($MSFT) - Information Technology & Software

• Alphabet ($GOOGL) - Information Technology & Innovation Conglomerate

• Amazon ($AMZN) - Internet Retail & Web Services

2. Semiconductors:

• Applied Materials Inc. ($AMAT) - Materials Engineering Solutions

• Broadcom Inc. ($AVGO) - Semiconductor Development & Infrastructure Software

• KLA Corp ($KLAC) - Semiconductor Manufacturing (Nano-electronics)

• Lam Research Corporation ($LRCX) - Semiconductor Manufacturing (Wafers)

• ASML Holding NV ($ASML) - Semiconductor Equipment & Development (Memory & Logic)

• Microchip Technology Inc. ($MCHP) - Semiconductor Manufacturing & Licensing

3. Consumer Discretionary & Retail:

• Lululemon Athletica Inc. ($LULU) - Athleisure Clothing

• Ulta Beauty Inc. ($ULTA) - Beauty Products

• LVMH Moët Hennessy Louis Vuitton ($LVMUY) - Luxury Retail

• Lennar Corporation ($LEN) - Homebuilding

• Chipotle Mexican Grill ($CMG) - Food & Dining

• Sherwin-Williams Co ($SHW) - Paint Manufacturing/Retail

4. Healthcare:

• Zoetis Inc. ($ZTS) - Pet & Livestock Healthcare Products/Treatments

• Thermo Fisher Scientific Inc. ($TMO) - Medical Devices & Equipment

• IDEXX Laboratories Inc. ($IDXX) - Pet & Livestock Healthcare Products/Treatments

• Intuitive Surgical Inc. ($ISRG) - Medical Devices & Surgical Equipment

• Iqvia Holdings Inc. ($IQV) - Healthcare Data Science & Clinical Research Solutions

• Edwards Lifesciences Corp ($EW) - Medical Devices & Cardiovascular Solutions

Conclusion:

Fear and greed are market dynamics that aren’t going anywhere. There will always be new risk events that cause investors to panic, then proceed to subside. There will always be new bubbles, either in individual assets or broader asset classes, that burst and reset. The market is a pricing mechanism for risk, fear, and greed in real-time. Therefore, it’s always possible that the risks we currently perceive for the future are less impactful and extensive than we think they will be. My optimistic nature makes me believe that technological innovation and human ingenuity will overcome future risk factors, and that the market will overcome each wall of worry like a track hurdler. Eventually, the track runner will clip their foot against a hurdle and fall, equivalent to the market downturns in 2001, 2008, and 2020. Without failure, the runner gets up and continues to run the race.

I don’t think that the stock market will trip on a hurdle in 2022, but we must acknowledge that it’s a non-zero possibility. The flip-side of that coin is that the market overcomes the known and unknown risks in 2022, and proceeds to make new ATH’s within the existing bull market. I think the latter is certainly more likely than the former.

We can’t know for certain what the market will do in 2022, which is why I prefer to assess the probabilities of various outcomes. While I certainly think that the market is experiencing some degree of exuberance at the present moment, the market gains we’ve experienced in the past eighteen months is proportional to the increase in money supply. It appears that the Federal Reserve’s tapering and tightening in 2022 will likely cause a reduction in stock market returns and risk appetites. Nonetheless, the S&P 500 and other U.S. indexes didn’t rise exponentially in 2021. Momentum and investor psychology are extremely important to future market returns, which makes me think there is a strong probability that the market continues to grind higher despite the outlook for monetary policy changes. In 2021, U.S. stocks consistently created new all-time highs in a stair-step manner by producing higher highs and higher lows. There’s no doubt in my mind that we’re in a bull market, and I think there’s a possibility that the market is able to shrug off reduced liquidity and continue to grind higher in the upcoming year.

Caleb Franzen