I Suggest You Panic

Investors,

Panic was the predominant theme of the market this week, almost entirely unwarranted given the fact that the S&P 500 generated a weekly gain of +0.7%. It’s extremely important to put this into context — the S&P 500 hit new YTD highs on Wednesday, 7/19, and fell -0.9% into the weekly close on Friday.

People are panicking? Good, panic.

I suggest you panic so that I (and other readers of Cubic Analytics) can maintain our composure and buy long-term stocks at a marginal discount and/or enter short-term trades at attractive risk/reward zones.

Seriously, let’s put this into context…

The S&P 500 is trading above all 3 major moving averages, which all have rising slopes.

🟡 21-day EMA

🔵 55-day EMA

🔴 200-day EMA

This statistical behavior doesn’t occur in downtrends and is a key characteristic of an uptrend! Until proven otherwise, which could happen in the coming weeks/months, equities are in an uptrend. It’s important to note that the 55-day EMA is trading above the August 2022 highs (green zone), which are both valid potential support zones.

Therefore, even if the $SPX falls -4.3% to -5%, it would retest these strong potential support levels and I believe that stocks will rebound if/when we get there.

For what it’s worth, all 4 of the U.S. stock market indices have this relationship with their short, medium, and long-term moving averages. Additionally, in each case, the 21-day EMA is trading above the 55 EMA, which is trading above the 200 EMA. That is bullish behavior, yet investors (or perhaps speculators) seem to believe that uptrends only occur in exponential fashion without any material pullbacks.

As I’ve been saying for months, I hope we get a pullback. I even dedicated an entire newsletter to this topic in late June:

Maybe this is the precipice of that pullback. I’m ready for it.

If you’re an emotional investor, I selfishly hope that you panic. If you’re an avid reader of Cubic Analytics, I hope that you stay composed, have a plan, and execute on that plan with appropriate risk management & levels of invalidation.

In the remainder of this report, I’ll analyze the key charts & data that rose to the top of my radar throughout the week. Before diving in, I’d encourage you to check out what the team at MicroSectors is doing right now by following them on Twitter. With gold prices starting to regain upside momentum, investors might be interested in researching the ETN solutions provides by MicroSectors:

Macroeconomics:

I think that the importance of liquidity dynamics will take center stage relatively soon, particularly with rates surging back towards/above their former YTD highs. In a week absent of any major significant news, in my opinion, I wanted to share some updates on where key Federal Reserve & commercial banking data stands today.

1. The Federal Reserve’s balance sheet has erased all of the gains from the bank failures/shutdowns in March/April and makes new multi-year lows:

As of Wednesday, July 19th, the amount of assets held on the Fed’s balance sheet declined by $22.37Bn relative to the prior week. Despite falling by $460Bn since the peak in mid-March, we’ve seen bank failures subside and asset markets party higher.

The Fed’s balance sheet has now contracted -7.0% YoY, the largest YoY contraction since September 2019.

2. Deposits outflows increased per the most recent commercial banking data, showing a steep YoY contraction:

Deposits at U.S. commercial banks have been contracting at the fastest pace on record (albeit the data series only goes back to 1974). The chart above highlights the YoY rate of change, currently at -4.2% YoY. On a week-over-week basis, deposits declined by $78.7Bn, which was the largest WoW decline since early April 2023.

While I don’t have theories as to why deposits declined this past week, I think this is a trend that is likely to persist on a YoY basis for some time, which is partially why I continue to believe that disinflation will remain the predominant theme in 2023.

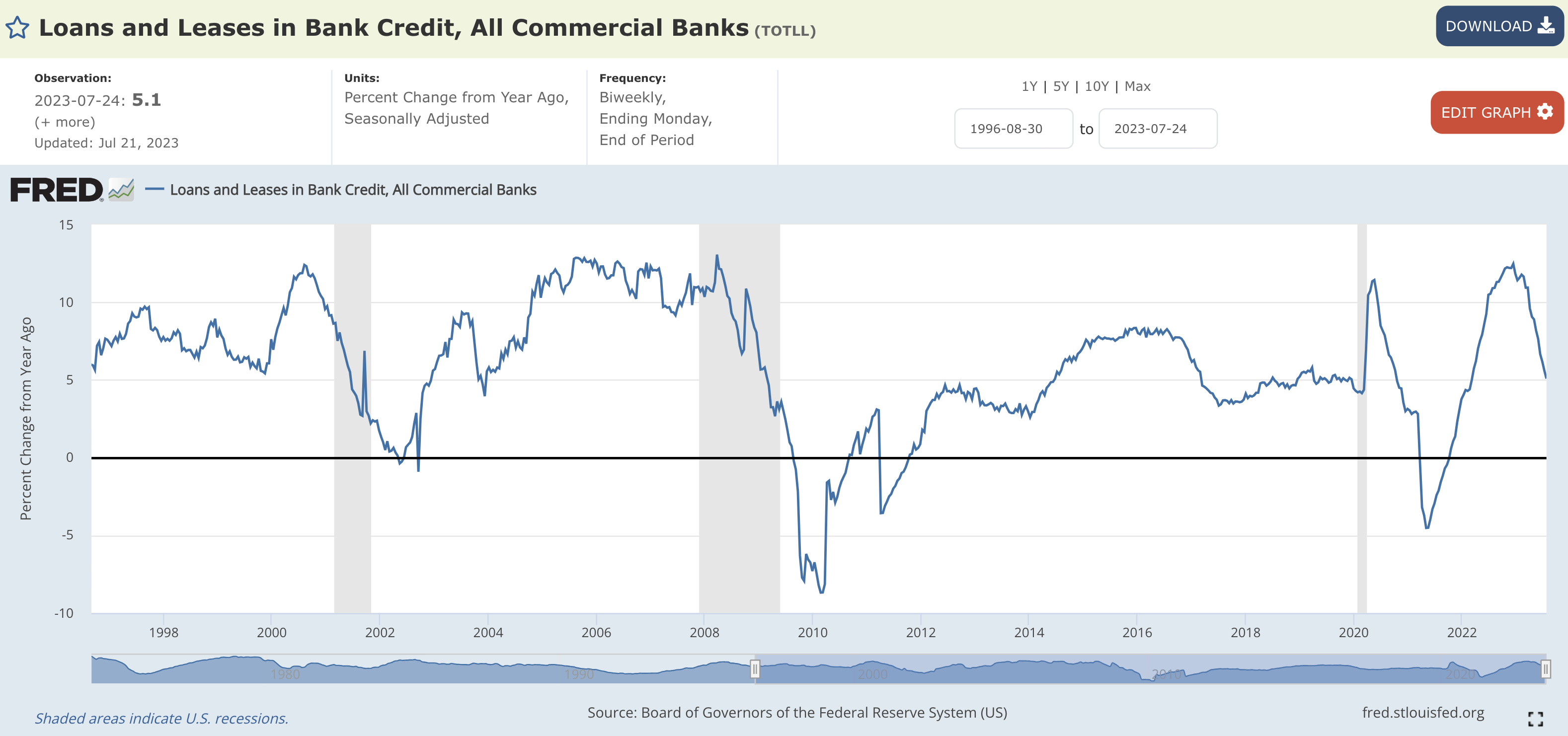

3. Credit creation & loan growth continues to decelerate, one of the major forecasts that I made in February 2023:

Given the stress on deposits, it’s a no-brainer that banks are going to reduce their lending activity as they shift into a defensive stance. On the other side of the lending equation, businesses & consumers are saturated with credit and likely don’t have as much demand as they did in 2021 or 2022. Both of these factors, in addition to high interest rates, are causing credit creation to decelerate. To be clear, loans & leases are still growing, but at a slower pace than they were in Q4 2022 & Q1 2023.

My expectation is that loan growth will continue to normalize & decelerate in the months ahead, likely towards ±0.0%.

Tying it all together:

Given the ongoing contraction and/or deceleration in key Federal Reserve & commercial banking data, I expect to see two things going forward:

An ongoing deceleration of inflation, aka disinflation.

A heightened risk of another credit event and/or failure.

The former is good. The latter is not. Neither are guaranteed, and the severity of the latter will determine the impact on financial markets & asset prices.

Stock Market:

In light of the palpable levels of fear in the market and the resurgent voices of bearish commentary, I want to remind you of the following:

Bears complained when FANG+ stocks were doing well.

Bears complained when mega-cap tech stocks were doing well.

Bears complained when expanded tech stocks were doing well.

Bears complained when nonprofitable tech stocks were doing well.

Bears complained when equal-weight S&P 500 was doing well.

Bears complained when international stocks were doing well.

Bears complained when financial stocks were doing well.

Bears complained when small caps were doing well.

Bears complained when meme stocks were doing well.

Bears complained when industrials stocks were doing well.

Bears complained when consumer discretionary stocks were doing well.

Bears have found every single reason (not an exaggeration) to highlight how something is bearish, yet market dynamics have been bullish for the significant majority of the year. The price action and YTD returns prove this to be true.

Yet bears have continued to complain, constantly moving the goal-post to justify their bearish outlook & biases.

What are they complaining about now?

That utility stocks, healthcare stocks, and consumer staples stocks are doing well.

These defensive stalwarts of the market, which are largely viewed as mature companies that are more recession-proof than the broader market and pay strong dividends, have finally started to pick up momentum.

Focusing on utility stocks in particular, it’s clear that the sector had a strong week:

The SPDR Select Sector Utility ETF is now trading above the 200-day moving average cloud, but it’s important to acknowledge that the MA cloud has a falling slope. That’s a stark contrast vs. each of the U.S. stock market indices, which all have a rising 200-day moving average cloud. Despite gaining +5.3% since the intraday lows on July 18th, the utilities ETF has a negative YTD return of -2.9%.

Premium members will know how much I’ve loved buying utility stocks this year in long-term accounts that I help to manage, consistently scooping up shares in a variety of boring businesses that pay strong dividends and lacked the upward momentum of the broader market.

Notably, I’ve been buying:

Republic Services Inc. ($RSG). This is a waste management company which hit new all-time highs this week.

American Water Works ($AWK). This is a water and wastewater services company, which continues to show strong fundamentals.

NextEra Energy Inc. ($NEE). This is a renewable electricity company.

In a similar vein, though they aren’t considered utility stocks, I’ve also been buying:

Service Corp ($SCI). This is a funeral home business.

Union Pacific Corp ($UNP). This is a railway transportation business.

To be clear, I’ve still being buying tech and a variety of other stocks in 2023, but I did want to highlight the utility stocks that I’ve been buying in light of their recent performance & participation to the upside.

On a relative basis, utilities vs. the S&P 500 is still within a downtrend:

Based on this RSI analysis, it’s possible that the recent bullish divergence could foreshadow some strength in utilities relative to the broader market in the coming weeks & months. We don’t know for certain, but the bearish RSI divergence September 2022 market the start of the downtrend for utilities relative to the S&P 500.

This will be something to watch going forward, particularly as a way to confirm that we are moving into a defensive market environment.

Bitcoin:

Last weekend, I shared data about Bitcoin HODL waves and even decided to share a Twitter post dedicated to the topic. It went “viral” for my standards, which are quite low, but received a tremendous amount of pushback regarding lost coins, Satoshi’s stack, and even the death of Bitcoin holders from COVID (yes, seriously).

I didn’t respond to any of these retorts; however, I’ll do so now in one sentence:

Lost coins don’t trend up & to the right, or have volatility with periods of downtrends.

Simple enough.

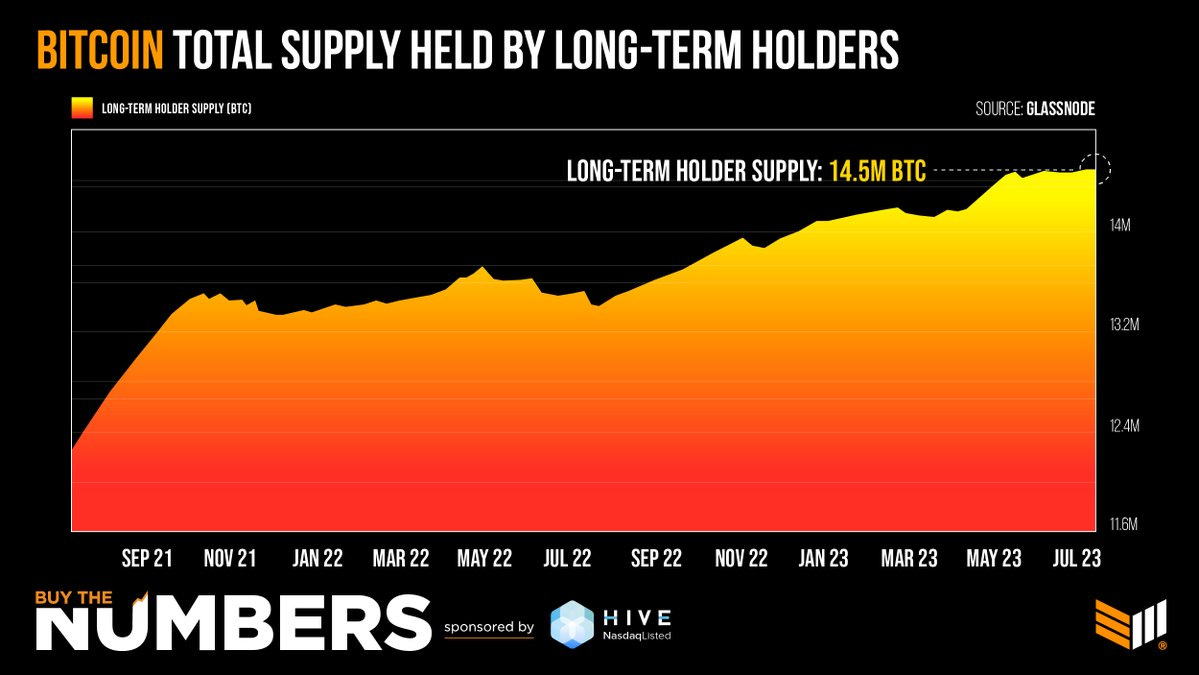

Adding onto this concept of HODL waves and “dormant” Bitcoin as a measurement of conviction & patience in the investor-base, I saw the following chart from the team at Bitcoin Magazine:

At the present moment, the amount of Bitcoin classified as a long-term holder supply has reached 14.5M Bitcoin, or roughly 74.6% of current circulating supply. That’s a new all-time high; however, I want to acknowledge a flaw in this classification of “long-term holder supply”.

According to on-chain data resource Glassnode, the definition of long-term supply is Bitcoin that hasn’t been moved in less than 6 months (or 155 days to be exact).

This isn’t even remotely close to being considered “long-term”, from my perspective.

For example, even the IRS bifurcates short vs. long-term capital gains by a threshold of 365 days. I’ve always thought even that period of time was considered generous for being “long-term”, but it’s a simple & easy rule of thumb for tax clarity.

My view is that long-term realistically starts around the 3-year mark.

Either way, this data is extremely compelling and shows some of the fundamentals of the Bitcoin monetary network and the investor base. These guys probably know a thing or two.

Best,

Caleb Franzen

SPONSOR:

This edition was made possible by the support of MicroSectors, a financial services and investment company that creates an array of unique investment products and ETN’s. Their NYSE FANG+ products are the only one of their kind, allowing investors to gain exposure, leveraged/un-leveraged and direct/inverse, to the NYSE FANG+ Index. They have a suite of products ranging from big banks, to oil and gas, and even gold/gold miners.

I started a partnership with MicroSectors because I’ve been using their products for over a year and this was an organic and seamless fit with my views.

Please follow their Twitter and check out their website to learn more about their services and the different products that they offer.

DISCLAIMER:

This report expresses the views of the author as of the date it was published, and are subject to change without notice. The author believes that the information, data, and charts contained within this report are accurate, but cannot guarantee the accuracy of such information.

The investment thesis, security analysis, risk appetite, and time frames expressed above are strictly those of the author and are not intended to be interpreted as financial advice. As such, market views covered in this publication are not to be considered investment advice and should be regarded as information only. The mention, discussion, and/or analysis of individual securities is not a solicitation or recommendation to buy, sell, or hold said security.

Each investor is responsible to conduct their own due diligence and to understand the risks associated with any information that is reviewed. The information contained herein does not constitute and shouldn’t be construed as a solicitation of advisory services. Consult a registered financial advisor and/or certified financial planner before making any investment decisions.

This report may not be copied, reproduced, republished or posted without the consent of Cubic Analytics and/or Caleb Franzen, without proper citation.

Please be advised that this report contains a third party paid advertisement and links to third party websites. These advertisements do not constitute endorsements and are not necessarily representative of the views or opinions of the newsletter author. The advertisement contained herein did not influence the market views, analysis, or commentary expressed above and Cubic Analytics maintains its independence and full control over all ideas, thoughts, and expressions above. The mention, discussion, and/or analysis of individual securities is not a solicitation or recommendation to buy, sell, or hold said security. All investments carry risks and past performance is not necessarily indicative of future results/returns.

Your articles are worth gold! I absolutely rely on your analysis and look forward to every single one. The sprinkle of humor in this one was my favorite part. Thank you!