Growth Is Crushing Value

Here's why that's important for Bitcoin...

Investors,

The stock market is at all-time highs relative to U.S. Treasuries. This isn’t a new trend, as the S&P 500 continued to make all-time highs relative to TLT throughout 2022. I highlighted this development several times, but this latest chart is from my good friend and a great analyst, Larry Thompson:

If you thought equity investors have had it rough over the past 18 months, fixed income investors have had it even worse. Given the consistency of the uptrend and strong momentum, this isn’t necessarily a trend that I want to fight in the short-run.

In other words, why be a fixed income investor (right now) when you can be an equity investor and benefit from these relative tailwinds?

Even during a week where the S&P 500 fell -1.14%, the 20+ Year U.S. Treasury ETF ($TLT) declined by -3.75% and had the lowest daily close of 2023. TLT is in a clear downtrend, trading below the 200-day moving average cloud, and even using it as resistance throughout 2023:

Retest, reject. Retest, reject. Retest, reject.

That’s not a bullish sign. Until proven otherwise, we should expect this pattern to continue. Given that the 200-day EMA & SMA are both downward sloping, it’s clear that momentum is to the downside and investors should continue to exercise caution.

Please note that my latest deep-dive is now available, focused on the data analytics & AI company, Palantir Technologies. The stock is up +140% YTD and hasn’t showed signs of slowing down. If you’d like to know more about this company, read this:

Macroeconomics:

There’s plenty to say about the labor market, but much of it has already been said after a week full of new labor market data. Amidst JOLTS, ADP Private Payrolls, Initial Unemployment Claims, and Nonfarm Payrolls, the main takeaway is that the labor market continues to be resilient and dynamic.

There was an interesting hypocrisy between ADP Private Payrolls, which beat estimates by an astounding margin, and the Nonfarm Payroll data from the BLS, which came in well-below expectations. Nonetheless, the unemployment rate declined to 3.6%, the labor force participation rate was unchanged at 62.6% (4th consecutive month), and average hourly earnings actually accelerated to +4.3% YoY. Also, the prime-age labor force participation rate (measuring the participation of individuals between the age of 25-54) hit a new multi-decade high of 83.5%.

There are (and have been) fundamentally strong aspects of the labor market.

However, both April and May’s NFP data were revised lower by a combined 110k jobs, indicating that prior reports weren’t nearly as strong as we initially expected. Regarding the latest data, a dive under the hood shows that almost all of these 240,000 jobs created were in the leisure/hospitality industry. There’s nothing wrong with those jobs, but it’s important to understand that they are predominantly part-time and cyclical positions in order to meet demand during the summer. The NFP data showed that 232,000 jobs were added in this industry — welcoming a large cohort of temporary waiters, bartenders, restaurant hosts, and cooks.

Again, this isn’t bad, but it isn’t ideal either.

I see no reason to panic about the labor market right now, particularly when many metrics remain historically tight and resilient.

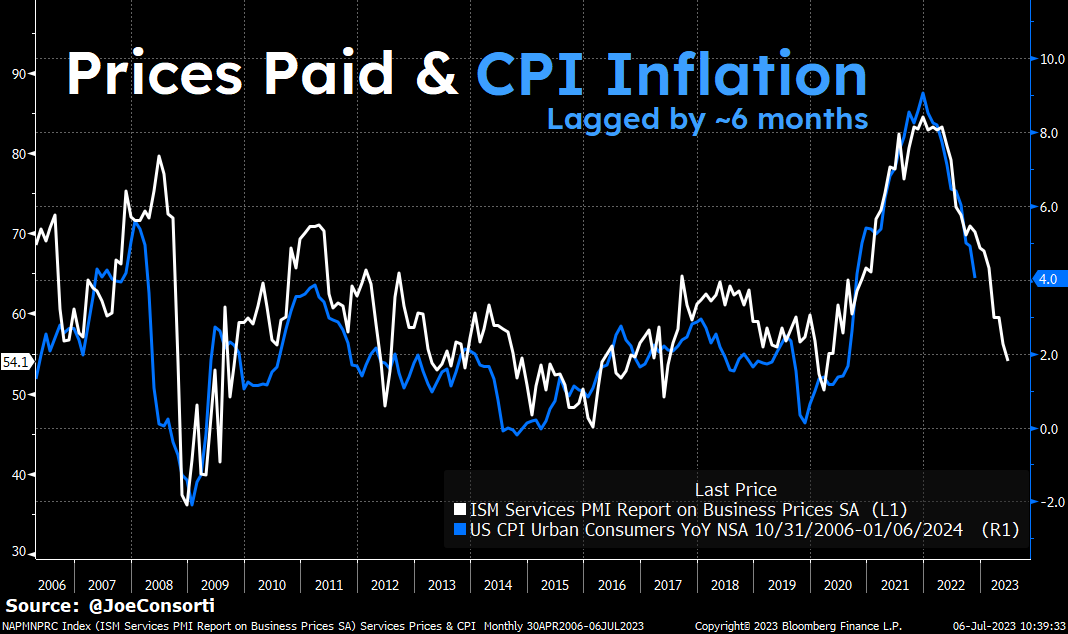

In my opinion, the most important datapoint from this past week was the ISM Services data and the Price Paid component in particular. Overall, the Services PMI was 53.9 (the highest reading in 4 months), indicating that the service sector is expanding at a faster pace. The Prices Paid component fell to 54.1 and it’s been rapidly falling for months.

Why is this important? I’ve shared the data before, but for the new readers, ISM Services Prices Paid leads CPI inflation by ~6 months. Therefore, it’s telling us where the CPI is likely headed at the end of this year: right around +2% YoY.

I reiterate my confidence that headline CPI will be at/below 2% by year-end.

Stock Market:

2022 was all about the outperformance of Value vs. Growth. So far, 2023 has been the exact opposite, with growth regaining momentum relative to value. This is a surprising development given that interest rates are still elevated (and hit new highs this past week). Specifically, I’m focused on the relationship between Vanguard’s growth and value ETF’s, VUG/VTV:

This relationship of Growth/Value is trading at the highest level since February 2022, retracing more than 61.8% of the peak/trough decline for all of my friends who appreciate fibonacci analysis.

Based on current market conditions, my expectation is that growth will continue to gain ground relative to value in the months ahead, particularly if interest rates start to subside. However, I still think value stocks are providing excellent opportunities as a long-term investor right now. I bought a substantive amount of stock at the end of Friday’s trading session, almost exclusively outside of the growth/tech area:

Even if these aren’t considered “value” stocks, they certainly aren’t “growth” either. These are not trades or short-term investments, and I am buying these stocks with the intention of holding them for quite some time, with the intention of buying more in the near future. I am not going “all-in” on these stocks and I continue to have a substantial cash position that I intend to keep allocating into U.S. equities.

There will be a time to buy more tech as long-term holdings, but now isn’t the time. That was the second half of 2022 through Q1 2023. If you missed that window, I’m confident that you’ll have another chance and I’d encourage you to avoid FOMO.

Bitcoin:

I want to piggy-back on the VUG/VTV analysis above, because it’s interesting to note that Bitcoin is heavily correlated with the growth/value ratio:

The correlation isn’t perfect, with plenty of divergences & gaps, but it’s pretty damn good. Still, their major peaks & troughs occurred almost in tandem. They’ve notably diverged since May 2023, indicating that the jaws of this gap will need to close.

My overall bullish bias for Bitcoin makes me think that BTC will play catch-up:

As a final note on Bitcoin, I wanted to focus specifically on one of the metrics I highlighted in the post above: realized price. This variable simply calculates the total per coin cost basis of all Bitcoin currently in circulation, which has provided a meaningful signal at the end of bear markets before a halving event:

So long as price of BTC remains above this realized price, I think good things will happen on a long-term basis. Falling below this level has provided long-term Bitcoin investors with an ability to buy BTC when conditions appear extremely unfavorable; however, history shows us that it’s best to buy when there’s blood in the streets.

Stay optimistic, but vigilant my friends.

Best,

Caleb Franzen

SPONSOR:

This edition was made possible by the support of MicroSectors, a financial services and investment company that creates an array of unique investment products and ETN’s. Their NYSE FANG+ products are the only one of their kind, allowing investors to gain exposure, leveraged/un-leveraged and direct/inverse, to the NYSE FANG+ Index. They have a suite of products ranging from big banks, to oil and gas, and even gold/gold miners.

I started a partnership with MicroSectors because I’ve been using their products for over a year and this was an organic and seamless fit with my views.

Please follow their Twitter and check out their website to learn more about their services and the different products that they offer.

DISCLAIMER:

This report expresses the views of the author as of the date it was published, and are subject to change without notice. The author believes that the information, data, and charts contained within this report are accurate, but cannot guarantee the accuracy of such information.

The investment thesis, security analysis, risk appetite, and time frames expressed above are strictly those of the author and are not intended to be interpreted as financial advice. As such, market views covered in this publication are not to be considered investment advice and should be regarded as information only. The mention, discussion, and/or analysis of individual securities is not a solicitation or recommendation to buy, sell, or hold said security.

Each investor is responsible to conduct their own due diligence and to understand the risks associated with any information that is reviewed. The information contained herein does not constitute and shouldn’t be construed as a solicitation of advisory services. Consult a registered financial advisor and/or certified financial planner before making any investment decisions.

This report may not be copied, reproduced, republished or posted without the consent of Cubic Analytics and/or Caleb Franzen, without proper citation.

Please be advised that this report contains a third party paid advertisement and links to third party websites. These advertisements do not constitute endorsements and are not necessarily representative of the views or opinions of the newsletter author. The advertisement contained herein did not influence the market views, analysis, or commentary expressed above and Cubic Analytics maintains its independence and full control over all ideas, thoughts, and expressions above. The mention, discussion, and/or analysis of individual securities is not a solicitation or recommendation to buy, sell, or hold said security. All investments carry risks and past performance is not necessarily indicative of future results/returns.