I’ve shared a handful of individual stocks that I’ve been buying so far in 2023 as core portfolio holdings in long-term accounts; however, I’ve simultaneously shifted my exposure away from tech, semiconductors, and growth in favor of REIT’s, utilities, and high-dividend stocks. Especially after a massive rally in tech/growth to start 2023, I don’t want to chase these risky segments of the market higher and I’m happy to wait for the market to come to me. The market selloff this past week justified my strategy because it allowed me to:

Sell stocks at a gain that we’re previously at a loss (NVDA, LRCX, EQIX, IDXX)

Raise cash

Shift towards defensive & high-dividend stocks (EXR, DLR, RSG)

The fact of the matter is, I’m excited to see market pressure return because it allows me to be opportunistic and buy stocks at a discount. I think more discounts are around the corner, and I will gladly increase my exposure to core portfolio holdings. In fact, I’m even expanding my list of core portfolio holdings during this market environment! If tech/growth returns back to levels from the start of 2023, I’ll gladly begin to start building a position in some individual names.

This is why I’m excited to keep conducting my deep-dive series for premium members! On Wednesday, March 1st, I’ll share exclusive analysis of Facebook ($META) with premium members. This will be the second edition in this series, after reviewing Chevron CVX 0.00%↑ at the start of February. These reports provide an unfiltered breakdown of the company, analyzing the qualitative and quantitative investment thesis in order to provide actionable takeaways on the stock. The Chevron report was more than 5,000 words long, so rest assured that I’ll be conducting a thorough review of the company. To upgrade your subscription and receive this report, take advantage of the 20% discount like below & become a premium member!

Over the course of the past two weeks, we’ve seen a resurgence in economic data and inflation dynamics. The January CPI data came in hotter than expected, but still decelerated on a YoY basis. The January PPI data came in hotter than expected, but still decelerated on a YoY basis. In last week’s edition, “Disinflation. Disinflation Everywhere!”, I highlighted one primary concern that I was having with the inflation data: median CPI accelerated on a YoY basis.

With hotter than expected data, I questioned whether or not incoming data would also re-accelerate or if this was a “one-off” hiccup.

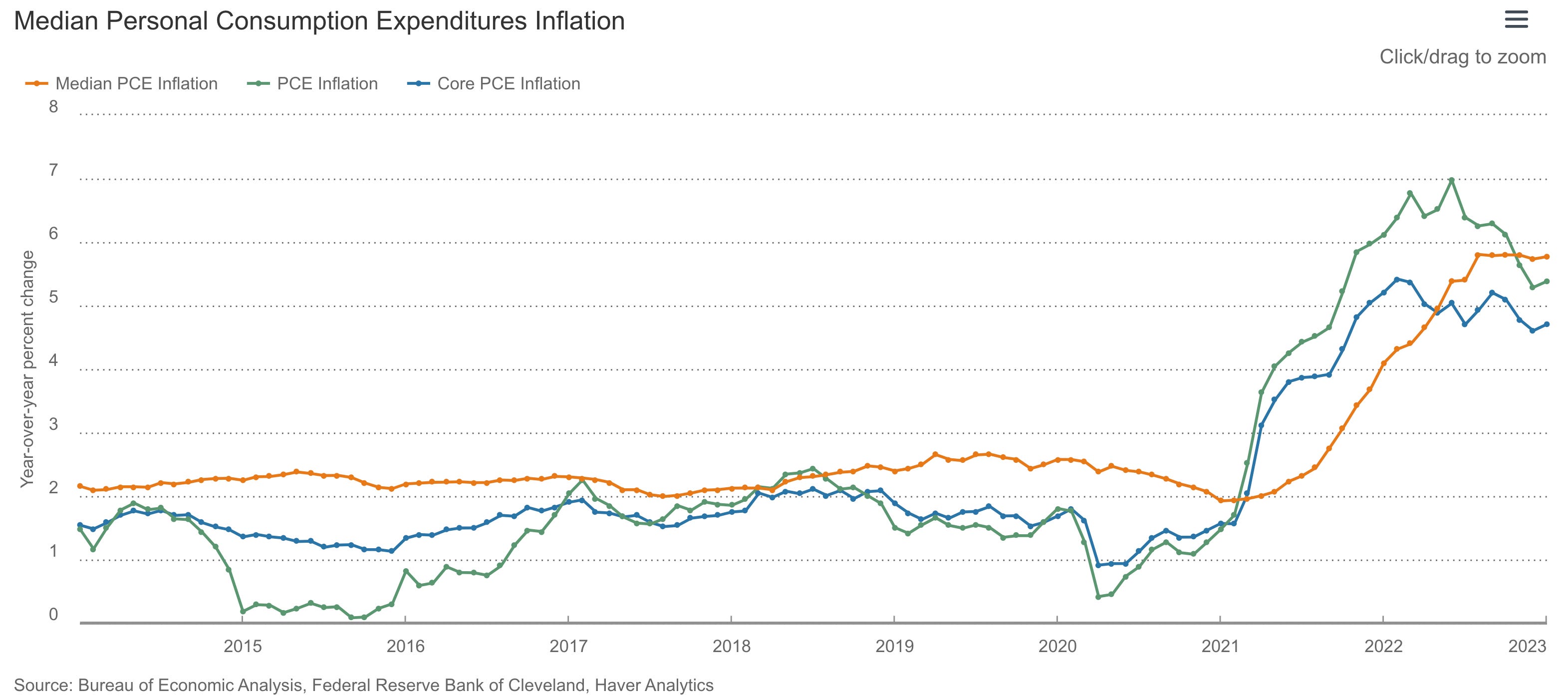

Unfortunately, the January 2023 Personal Consumption Expenditures (PCE) data was published on Friday morning, which also indicated a re-acceleration. Estimates were projecting for a YoY increase of +5.0% and a MoM increase of +0.5%, but the actual results were +5.4% and +0.6%, respectively. Core PCE also came in hotter than expected & prior month results, at +4.7% YoY and +0.6% MoM.

Both headline & core PCE are well-below their peaks in mid-2022, but this 1-month resurgence has put economists and investors on notice.

Courtesy of Holger Zchaepitz

Median PCE is also accelerating after moving sideways for the past four months. I place a heavy significance on the median data, which is why I focused on median CPI last week, so it will be important to monitor this metric in future inflation reports.

Each of the individual inflation reports, along with strong January retail sales, have caused the market’s expectations of Federal Reserve policy to jump higher. The “higher for longer” market theme has repeatedly been dismissed and reestablished for the past 6-8 months, but the market is once again awakening to the reality that the Fed isn’t done tightening with the intention of keeping rates elevated. Across the maturity spectrum, yields are spiking higher.

For attentive & frequent readers of Cubic Analytics, the recent breakout in yields is unsurprising, based on my February 11th piece when I wrote the following:

The 5, 10, and 30-year Treasury yields all broke out above important resistance trendlines, shown in the charts below:

A New “First” For Bitcoin

Since posting these charts, we’ve seen each of these yields accelerate higher with minimal pullbacks. Simultaneously, we’ve seen risk assets struggle to maintain upward momentum and even outright weaken. As we all know, all else being equal, interest rates and asset prices have an inverse relationship.

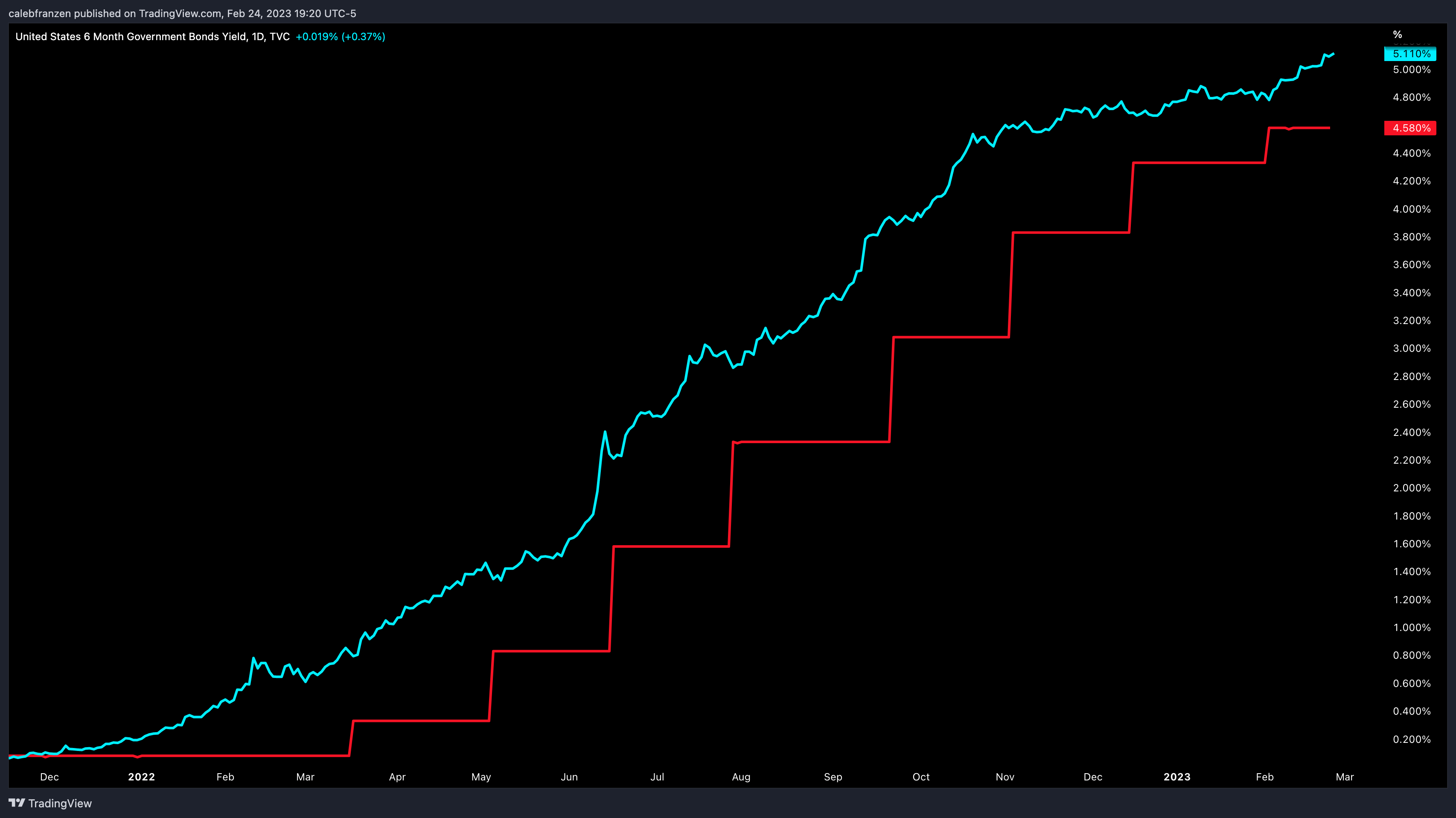

Since December 2022, I’ve shared my belief that market participants should be focusing on the 3-month and 6-month Treasury yield rather than the 2-year Treasury yield as “the arbiters of truth” for Fed policy. While the 2, 5, 10, and 30-year yields were declining in Q4 2022 & January 2023, the short-duration yields were continuing to push higher.

Why is this important? Because it’s forecasting exactly where the Fed is going!

As of Friday’s close, the 6M Treasury yield is 5.11% while the effective federal funds rate is 4.58%, generating a spread (or difference) of 0.53%.

6M Treasury yield (blue) vs. EFFR (red)

In other words, the bond market is currently expecting that the Fed will raise rates by +0.25% at least another two times. All investors should have this as their base-case for policy dynamics within the next 6 months, though I wouldn’t be surprised if the Fed raises by more than an aggregate magnitude of +0.5% by September 2023.

Stock Market:

As mentioned above, the inverse relationship between interest rates and asset prices (all else being equal) remains the its position as the most critical dynamic to understand in the market. With yields ripping higher this week, asset prices crumbled. Each of the indexes had their worst week of 2023, giving back a significant portion of the YTD gains from just a few weeks ago. Here’s key data to understand:

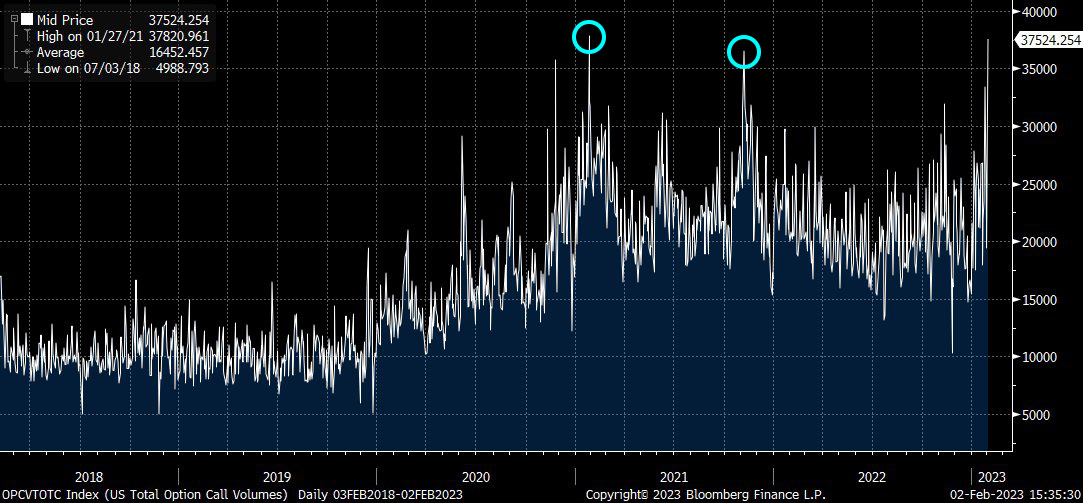

In many ways, this latest decline in risk assets is warranted. Premium members will know that I’ve been highlighting under-the-hood deterioration for the S&P 500 for the past three weeks, almost perfectly when each of the indexes hit YTD highs on February 2nd. On February 5th, I published “Irrationality” and highlighted how call option volume hit new all-time highs that week.

This volume corresponded with levels last seen in January/February 2021 (peak ARKK, tech/growth, SPAC’s, etc.) and November 2021 (peak crypto, Nasdaq-100, and FANG+ stocks). Essentially, peak exuberance & speculation translated into peak asset prices.

I stumbled across a piece from the Financial Times, “Meme-stock 2.0: Wall Street’s retail trading boom is back”, which highlighted how retail investors are allocating capital at a historic pace. Of note, the article was published on February 14th, so the data is at least one week stale:

This essentially confirms the sentiment from the call option volume data. The market even reached levels of extreme greed, peaking on 2/2/23 and falling rapidly since then. Fear is returning to the market, but only by a marginal amount so far.

Nonetheless, speculative stocks are still having a phenomenal YTD return so far in 2023. Using ARKK as a gauge, Cathie Wood’s flagship fund is still up +23% YTD, though it had gained as much as +45% in the first 22 trading days of the year! It’s been a crazy start to the year, with a massive momentum thrust to the upside. I think the craziness is just getting started, with violent moves in both directions. It’s essential to build a thesis, have conviction in it, develop a plan around that thesis and execute on it. This is why I’ve been able to maintain my composure this year, de-risk my portfolio, and shift my allocation. Maybe my thesis is incorrect, I don’t know.

Time will tell.

Bitcoin:

With risk assets taking a nose-dive this week, crypto was impacted quite substantially. Bitcoin was trading slightly above $25,000 on Tuesday but is hovering above $23,000 as I write this on Friday evening. I’ll keep this section short & sweet, because there isn’t much crypto-specific news that’s driving market conditions right now. Similar to 2022, everything is macro-driven.

Nonetheless, Bitcoin is doing an excellent job of adhering to key structural levels & statistical indicators. For example, I’ve been highlighting the 200-week moving averages since mid-2022. Initially, this zone acted as potential support; but it’s since flipped into resistance since August 2022. In mid-January, I told investors on Twitter that the 200-week moving average cloud was a logical upside target:

After a perfect retest, Bitcoin is getting rejected on this level once again…

To be clear, this hasn’t been a significant rejection yet, but it’s clearly acting as a “glass ceiling” for the price of the digital asset. Acting as support for the entirety of Bitcoin’s lifecycle, the ongoing bear market is the first time where this level has acted as resistance (August 2022 & Q1 2023). While it’s still possible that price is able to break above this zone, I also want to point out one other interesting dynamic with this indicator…

For the first time in Bitcoin’s history, the 200-week exponential moving average (teal) is falling below the 200-week simple moving average (yellow). To understand why this is significant, we must understand how these two moving averages are calculated:

Simple moving average: an equal-weighted average, in this case measuring the average closing price of the past 200 weeks.

Exponential moving average: an average calculation that puts more weight on recent price data than older price data.

Essentially, the EMA helps to provide more context about the recent trend of price data while the SMA provides a smoothed out version that gives each data point an equal representation. With the 200-week EMA crossing below the SMA for the first time, this means that recent price data over the past 200 weeks (roughly 4 years) is facing more downside pressure than the equal-weighted version. In plain english, the downside momentum is historically significant right now.

Once again, I don’t feel any need to rush into buying Bitcoin at current levels and I’d prefer to wait for sub-$21k to resume DCA purchases.

Best,

Caleb Franzen

DISCLAIMER:

This report expresses the views of the author as of the date it was published, and are subjected to change without notice. The investment thesis, security analysis, risk appetite, and time frames expressed above are strictly those of the author and are not intended to be interpreted as financial advice. As such, market views covered in this publication are not to be considered investment advice and should be regarded as information only. Everyone is responsible to conduct their own due diligence, understand the risks associated with any information that is reviewed, and to recognize that the information contained herein does not constitute and should be construed as a solicitation of advisory services. Cubic Analytics believes that the information & sources from which information is being taken are accurate, but cannot guarantee the accuracy of such information.

This report may not be copied, reproduced, republished or posted without the consent of Cubic Analytics and/or Caleb Franzen, without proper citation & reference.

As always, consult a registered financial advisor and/or certified financial planner before making any investment decisions.

Great piece