Investors,

As we inch towards the end of the year, I am beginning to write my 2023 market outlook. This report will be entirely free, available for all, and is set to be published on January 1, 2023. It feels like we are on the precipice of an extremely bifurcated path as we enter the new year, more so than prior years. Going into 2022, the market was aware of inflationary dynamics & the beginning of monetary tightening. Most investors got completely blind-sided when both of these factors influenced market dynamics significantly more than anticipated. Investors are now concerned by a myriad of factors, overwhelmingly associated with one simple question:

Can the Fed accomplish a soft-landing that cures inflation?

Everything revolves around this question as we enter 2023. There will be a time and a place for me to dive into this topic further, but this isn’t it… so stay tuned for 1/1/2023!

As a quick thought on the macro-related dynamics before diving into the key market charts that you need to know about, many investors are highlighting how the latest inversion of the 2Y Treasury yield & the federal funds rate (FFR) means that the Fed is done tightening. I have two rebuttals for this misguided perspective:

1. The people who are pointing this out are the same people who refused to acknowledge the relationship between the 2Y/FFR earlier this year. The selective hearing & cognitive dissonance around this topic is laughable. I first analyzed this key relationship in February 2022, highlighting how the Fed was going to need to play catch up & tighten policy quickly. Most investors ignored this at the time, despite multiple follow-ups and occasions where I highlighted it again. Now that the inversion has occurred, everyone is celebrating it as if the Fed is done tightening and assets will go up again. Don’t fall for this narrative too soon.

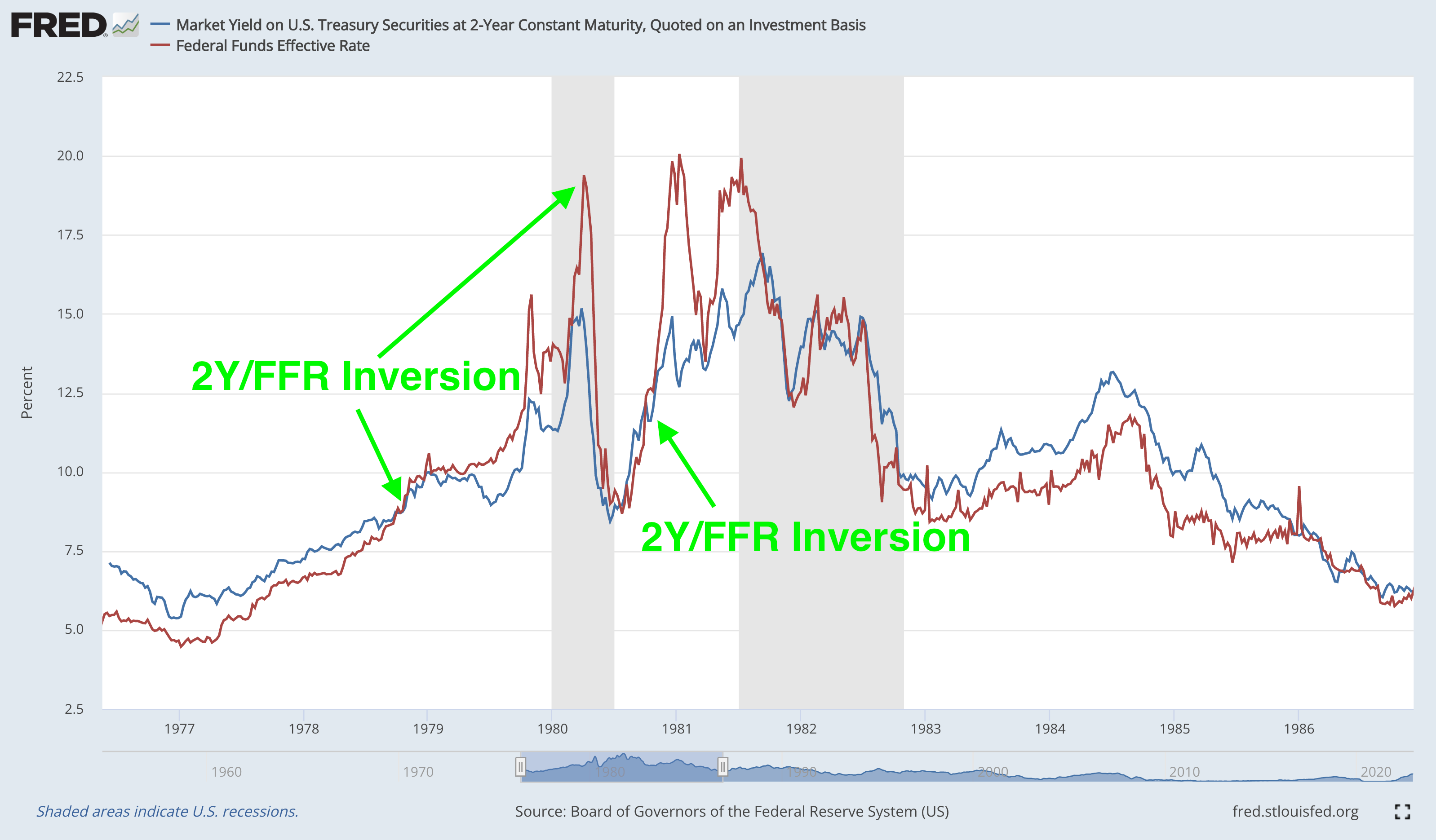

2. The inversion of this relationship has indeed signaled that the Fed is done raising rates, typically. However, these “typical” scenarios are during non-inflationary regimes, where inflation is within the Fed’s target or within a comfortable distance. Therefore, such pauses are understandable and warranted. However, this isn’t the case during an inflationary regime with historically high inflation. Consider the following chart comparing the 2Y Treasury yield (blue) vs. the federal funds rate (blue):

Even after the FFR > 2Y Treasury yield in Q4 1978, the Fed continued to raise rates to combat inflation and the inversion persisted through July 1980. The curve re-inverted in October 1980, then remained inverted for the next 11 months. Essentially, this inversion does not guarantee that the Fed is done tightening, as many have suggested. We should continue to exercise patience, recognizing that we are in an inflationary regime not seen since the 1970’s/80’s, and that we can’t use non-inflationary regimes to extrapolate how monetary policy will evolve in an inflationary regime.

While the inversion may signal that the hiking process is in the latter stages of the cycle, I’m not willing or comfortable to decisively say that the Fed is done tightening. Anyone who expresses resolute confidence on this issue should be avoided, in my humble opinion. Stay flexible, nimble, and willing to recognize that the Fed has proven to be steadfast in their approach to combat historic inflationary pressures.

In today’s newsletter, I’ll focus on market-specific dynamics that are currently unfolding and how these key charts & datapoints are impacting my overall thesis at the moment. Specifically, I’ll be sharing the three important indicators & charts for the S&P 500 and the most important crypto chart that investors need to be aware of.

As we enter the upcoming week, here’s what you need to know: