Edition #95

Retail Sales Maintain Momentum, Semiconductor Stocks, On-Chain Ethereum Analysis

Economy:

As some metrics for economic conditions have seemingly weakened over the past few months, in addition to high levels of inflation that haven’t been seen in over a decade, economists have begun to reduce their expectations for many economic data points. In the most recent case, the August 2021 retail sales data was released on 9/16, with an expectation of a month-over-month decline of -0.8%. Technically, this would have been an improvement relative to the prior month data, which saw a -1.8% contraction in the month of July.

The data came in with a surprising upside bounce, resulting in a +0.7% growth in retail sales for August 2021. Adjusted for seasonal variation, U.S. retail & food services sales were $618.7Bn, on track for an annualized amount of $7.424Tn. As we can see from the chart below, provided by the New York Times, retail sales have been very stagnant since March 2021; however, the August 2021 result represents a +15% increase relative to August 2020.

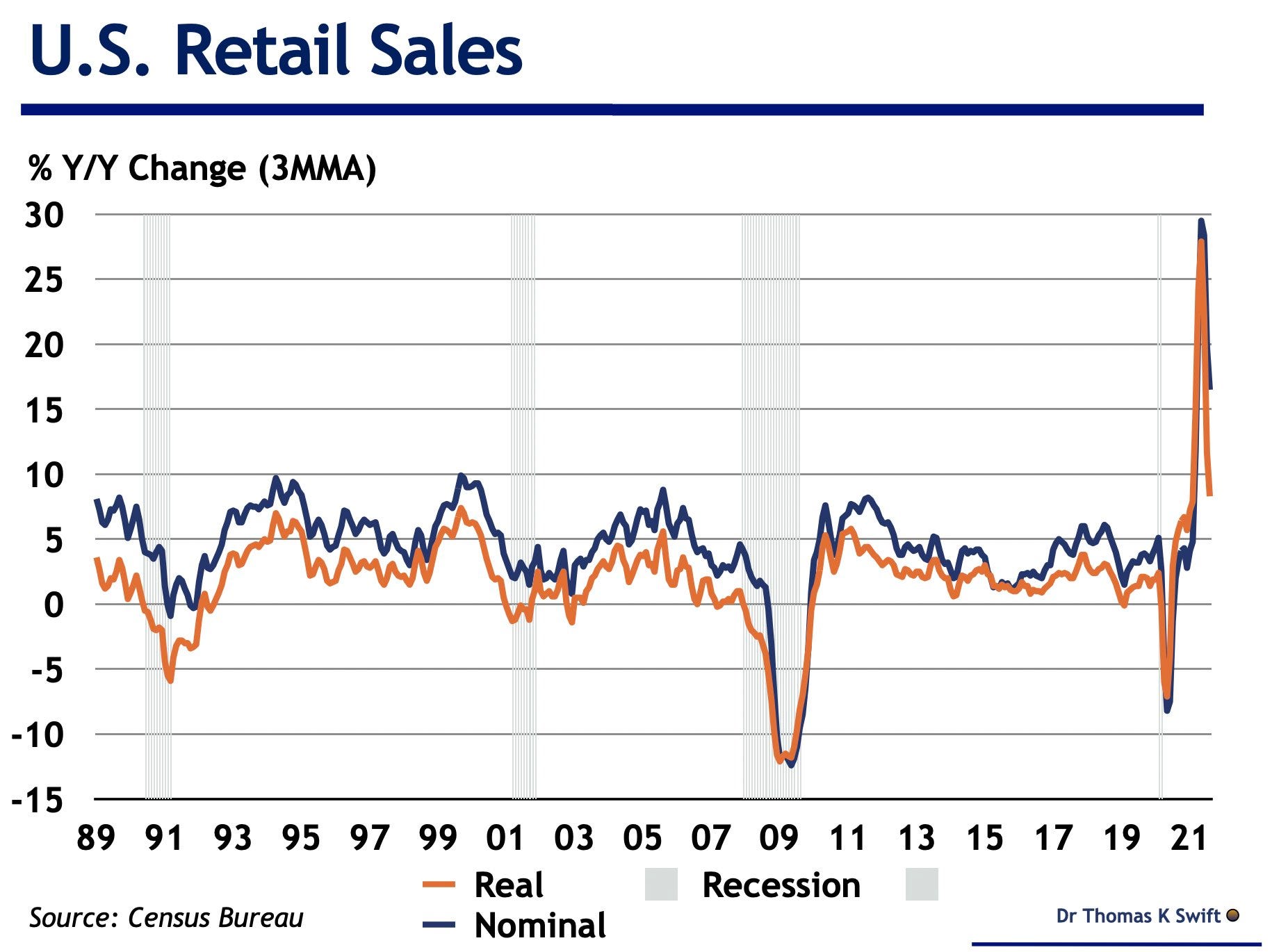

If we instead wanted to track the year-over-year change in nominal and real terms, the chart below helps give us perspective on the relative change in retail sales on this basis. I think this gives a complete gauge on retail sales, in combination with the data that we’re seeing in the chart above from the NYT.

On this basis, the spike that we saw a few months was clearly unsustainable. In a post-recessionary environment, we fully expect to see a massive rebound in consumer activity. The unique thing about the COVID-induced recession is that the lows of the decline were more muted than the Great Recession, but the highs of the rebound have been much more magnified! I fully expect the YoY tracking to fall in line with the historical trend, but likely sustain in the 5-10% range for longer than prior economic recoveries.

Stock Market:

Very quickly, I saw an excellent chart regarding semiconductor stocks that I thought served as a useful follow-up to the newsletter I published on Thursday. The chart below shows the pure price action of an equal-weight basket of semiconductor stocks, which have been in the early stages of a breakout to new all-time highs. However, while the aggregate (or nominal) value of semiconductor stocks is moving to new ATH’s, the value relative to the broader stock market is still moving within a base and has yet to breakout.

In my opinion, I see this as a bullish development because it reflects that the semiconductor sector still has ground to regain relative to the S&P 500. Once again, I reiterate my bullish outlook on semiconductor stocks. As a reminder, here are the semiconductor stocks I’m most interested in trading/owning:

$NVDA, $TSM, $AMBA, $LRCX, $AVGO, $SITM, $CDNS, $KLAC, $AMAT, $MCHP, $AMKR, $XLNX. I forgot to include $AMD in my list from Thursday, but it should also be included.

Cryptocurrency:

For the first time in four months of writing this newsletter, we won’t be discussing Bitcoin in the Crypto section. In the young life of this newsletter, the data that I’ve shared re: Bitcoin has been primarily focused on adoption, network growth, Metcalfe’s Law, and the idealogical value/purpose of Bitcoin. While my entire crypto exposure is 100% allocated to Bitcoin, and Bitcoin comprises more than 60% of my liquid net worth, I’ve also been a massive proponent of Ethereum. I’ll save the specifics for a future newsletter as I start to incorporate more ETH discussion, but I wanted to share some baseline data that helps to show why I remain so enthusiastic about this specific digital asset.

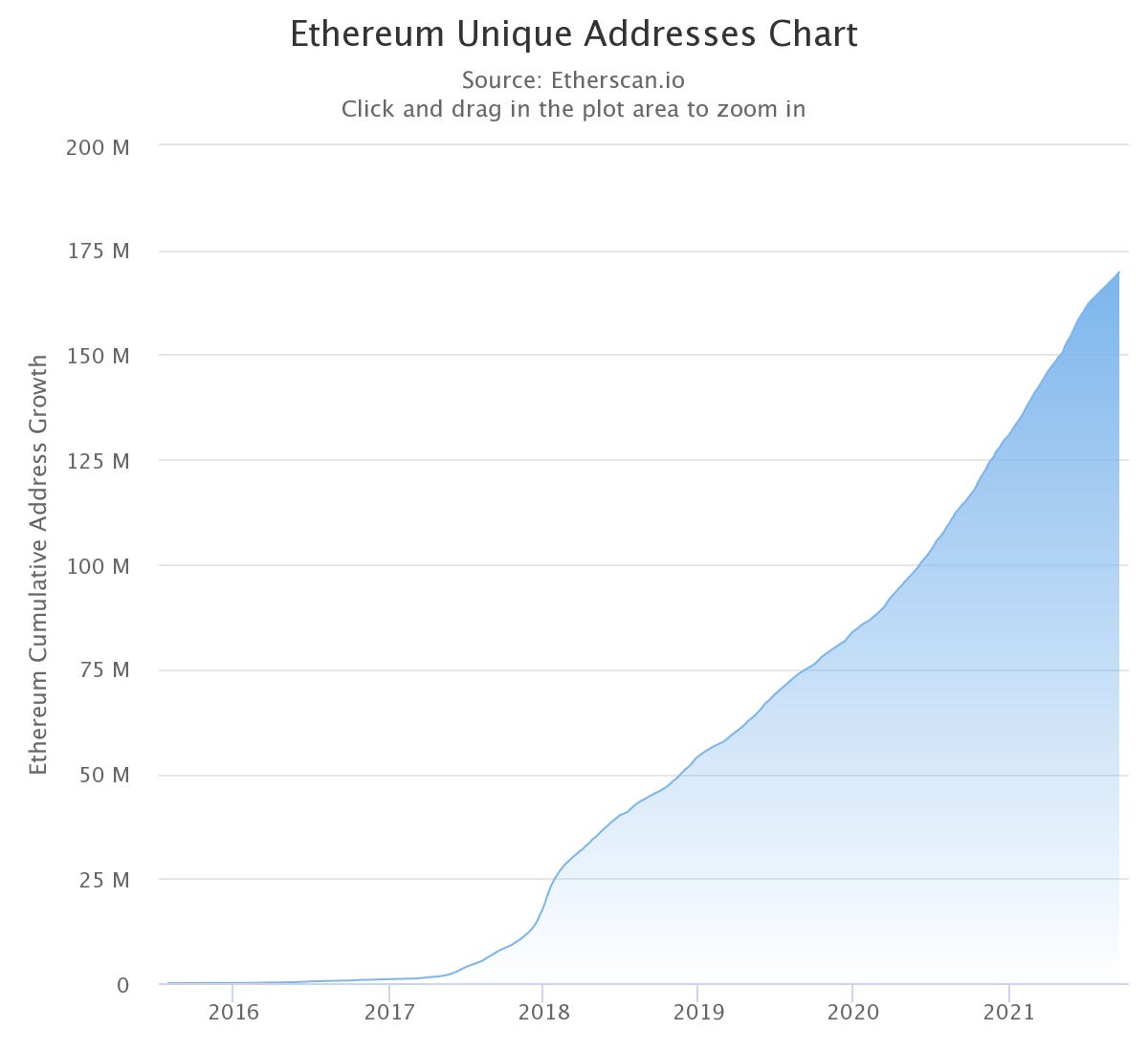

First of all, adoption continues to accelerate at a consistently high rate. The curious thing is that the adoption curve doesn’t actually appear to be very exponential! The chart below shows the cumulative amount of unique ETH addresses (169.7M as of 9/17/2021):

After being created in 2015, we can see an exponential growth curve in the 2017 cycle, followed by a steady & linear increase in addresses thereafter. You could make the case the we saw an acceleration in growth in 2020, in the aftermath of the COVID-induced crash; however, the rate of the increase was quite minimal. I believe the digital asset will soon see an exponential growth curve again in this current cycle, reflecting a higher demand for ETH as new users come into the market at an increased rate.

Aside from cumulative addresses in existence, we can also examine active addresses as measured by the aggregate amount of addresses sending/receiving ETH on a daily basis.

As of 9/16, there are 782,000 active ETH addresses transacting on a daily basis. This is well-below the all-time highs of 1.168M daily-transacting addresses in May 2021. The current reading of 782k represents 0.23% of the United States population and 0.01% of the global population. Again, we’re still ridiculously early in the adoption curve despite the tremendous growth the network has already experienced.

The final chart I want to cover in this introductory analysis & overview is related to some of the current on-chain analytics. Because the blockchain is a decentralized & public ledger, on-chain analytics is a way to gauge and study some of the “under-the-hood” movements and trends within a specific crypto asset.

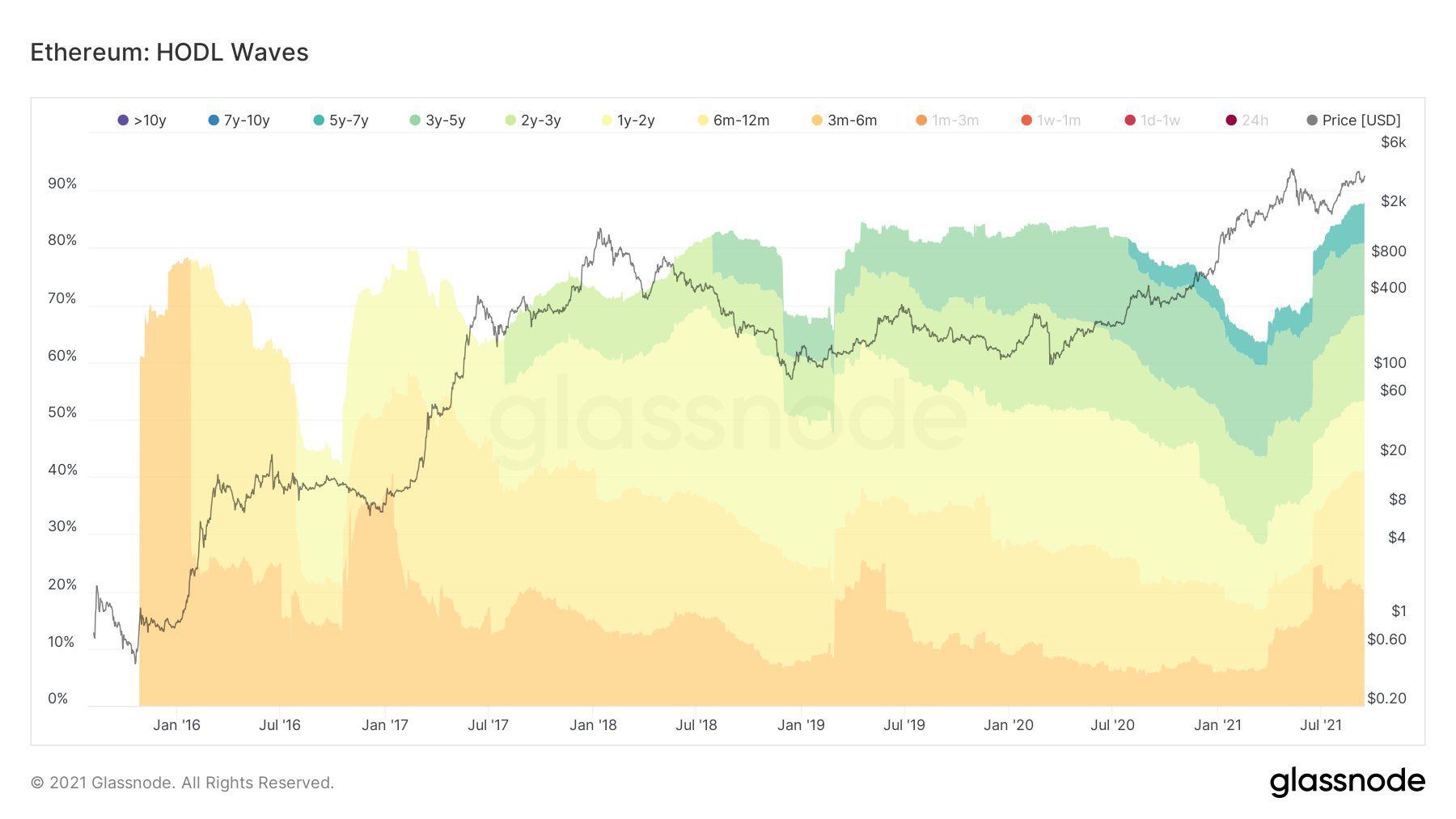

For example, because all of the data is public, on-chain analysts are able to determine the “age” of each wallet address and the amount of time that each particular ETH is held in said wallet. We can visualize how frequently (or infrequently) a digital asset is moved as a way to gauge the owner’s conviction in holding the asset. The chart below does exactly that, with the amount of time that ETH’s are held in a particular address by groups of time.

Based on this, we can see that nearly 90% of total ETH supply has not been moved in at least 3 months. Additionally, about 40% has been held in the same wallet address for 12 months or less. This means that ETH investors and users have extremely high conviction in the digital asset. Over time, I suspect these figures will become “younger” as there are more use-cases for owners to spend their digital assets and as smart-contracts become more widely adopted. This will happen over time as the digital asset becomes less of an investment security and more of a currency and transaction layer security.

Talk soon,

Caleb Franzen

Interesting insight, thanks Caleb!