Edition #9 - 5.27.2021

Global Central Bank Policy, Price/Sales of The Big 4, Apple & PayPal Accelerate Crypto Adoption

Economy:

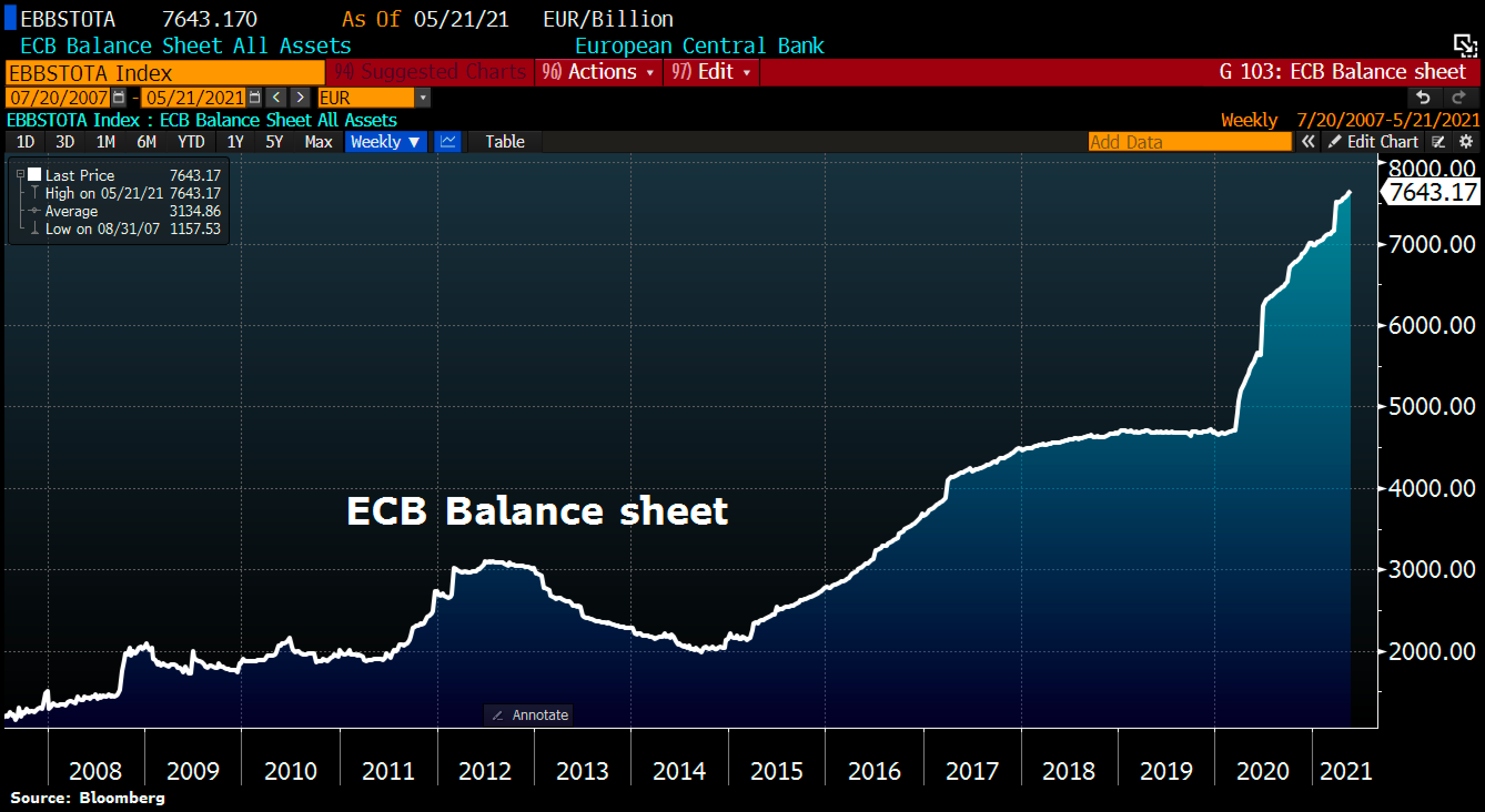

I saw a great chart from Holger Zschaepitz on Twitter (@Schuldensuehner), who I follow for his informative posts on central banks, monetary policy, and global financial conditions. Unlike other journalists I follow, Zschaepitz posts on the activity of the European Central Bank (ECB), which helps me to frame the actions of the Federal Reserve here in the U.S. While these two central banks have different mandates & objectives, the policy tools they use are nearly identical, and merely vary in the magnitude, duration, and justifications for such policy choices.

Zschaepitz recently posted the following chart of the size of the ECB’s balance sheet, along with the below quote:

“ECB balance sheet hit fresh ATH at €7.643.2tn as Lagarde keeps printing press rumbling. Total assets rose by €27.5bn on QE. ECB balance sheet now equal to 77% of Eurozone GDP vs. Fed's 36%, BoE's 38.4%, and BoJ's 133%.”

For context, feel free to return back to Edition #7 where I provided the most recent version of the Fed’s balance sheet. The growth trajectories are nearly identical, with some minor differences. The important thing that I want to call attention to is how the ECB and Bank of Japan (BoJ) have significantly greater size of the balance sheet relative to their national GDP’s than the Fed. For those who are unfamiliar with these figures, they’ll be even more surprised to see that the size of the BoJ’s balance sheet is 33% larger than the Japanese economy. Considering that the Q1 GDP in the United States was roughly $22Tn, that would imply that the Fed’s balance sheet would be over $29Tn if it was an equal ratio to that of the BoJ. Even if the Fed grew its balance sheet to the same relative size of the ECB, that would mean the Fed’s assets would grow to nearly $17Tn. As of the most recent information, the Fed’s balance sheet is currently $7.923Tn.

When I hear perma-bears (people who continuously predict the downfall of the U.S. economy, end of the dollar’s status as the world’s reserve currency, and implosion of domestic asset prices) shout that the Fed has exhausted its toolkit, this info is always the first counter-argument that comes to my mind. Additionally countries like Japan and several within the Eurozone have negative-yielding debt, in which the nominal yield on government bonds is less than zero. While U.S. Treasury yields are near historical lows, they haven’t slipped below zero. Additionally, the Bank of Japan is currently the only central bank in the world to purchase domestic equities and has been doing so since 2010! In fact, according to an article by Marcus Lu of Visual Capitalist, the BoJ is currently the largest owner of Japanese equities, valued at $434Bn as of November 2020. Clearly the Federal Reserve has more tools at its disposal.

Perhaps it is a subject for a future deep-dive paper, but one of the reasons I believe the U.S. dollar has yet to lose significant value or face substantial inflationary pressures is because the other major central banks in the world are conducting the same monetary policy at larger magnitudes, printing more & faster, doing so for even longer, and expanding their asset purchase programs to corporate bonds & equities. When the policies of global central banks have pushed nominal interest rates negative, no wonder global investors are still flocking to the USD and dollar-denominated assets. Relative to the value of their own currencies, the USD is a significantly more attractive investment, particularly as the United States conducts an easing monetary policy which is beneficial to USD-denominated assets. It’s a win-win, they get to buy USD, which yield a positive nominal yield & can invest in U.S. assets which are historically the best performing markets.

Based on the trajectory of interest rates globally & the likelihood that the inter-bank lending rates will continue to remain at/near/below zero percent, I remain optimistic on asset prices in the intermediate & long-term.

Stock Market:

Here’s an interesting chart provided by Charlie Bilello (@charliebilello), showing the trailing twelve-month revenues of the four largest U.S. companies (ranked in order of market capitalization):

Apple Inc. ($AAPL) $2.117Tn

Microsoft ($MSFT) $1.894Tn

Amazon ($AMZN) $1.647Tn

Alphabet ($GOOGL) $1.615Tn

Charlie mentions that the sum of their respective TTM revenues, $1.101Tn, is a record high for the four largest companies in the U.S. & is greater than all but 14 country’s GDP. That is absolutely astonishing, highlighting just how brilliant & significant these companies play in our daily lives. There isn’t a single day that I don’t use at least 3 products/services from these companies, and the likelihood that I use all 4 is quite high. Look at the amazing growth trajectories of each of their revenues, all of them with an increasingly positive slope.

After seeing this chart & taking some time to reflect on the magnitude of it, I had one glaring curiosity: what is the cumulative price to sales ratio of these four companies? By taking the aggregate market cap divided by the aggregate TTM sales, we can get a sense of how much investors are willing to pay for a single dollar of revenue! In traditional finance, this is often used as a gauge for valuation in which a low price/sales would indicate that a stock is inexpensive and undervalued, implying that it is more attractive. I never subscribed to that notion because my perspective was that investors would be willing to pay a premium (aka a high price/sales ratio) for higher quality and/or future growth potential. Just because something is expensive today doesn’t mean it won’t continue to be just as expensive (or more) in the future. Additionally, the price of a McDonald’s cheeseburger isn’t necessarily undervalued just because it costs less than Shake Shack, Five Guys, or In-n-Out. I think most people would agree that the latter three brands make a significantly better product with better ingredients than McDonald’s, hence the higher price. Consumers, and investors, are willing to pay a higher price for higher quality goods/investments.

According to YCharts, the TTM price/sales ratio of the entire S&P 500 is 3.07 as of April 30, 2021. This means that an investor who theoretically buys the S&P 500 is willing to pay $3.07 for every $1 generated by the cumulative companies within the index. With that context in mind, the price/sales of the four companies is given by:

$7.273Tn / $1.101Tn = 6.6

Essentially, investors are willing to pay more than a 2x premium for $AAPL, $MSFT, $AMZN, and $GOOGL than they are for the broader S&P 500. Considering that these four companies are the largest allocations within the S&P 500, that implies that they are pulling the index’s price/sales ratio higher. Said differently, the price/sales ratio of the S&P 500 ex-Apple, Microsoft, Amazon, and Alphabet would be some value less than 3.07. I’m genuinely surprised that the price/sales of the top four largest companies isn’t higher.

So why would investors be willing to pay a 2x premium for these companies? Aside from a fundamental argument about the cash flows these companies generate, the dividends they pay, the value of their assets, success of management, etc., investors make an important decision regarding opportunity costs when they invest. By allocating a single dollar to one stock, an investor can no longer allocate that same dollar to another stock. With a finite amount of dollars to invest, an investor will choose to allocate their capital where they believe it will generate the best return per unit of risk! Therefore investors are willing to pay a premium, in regards to the price/sales ratio, to own these four companies because they think that the investment provides the best risk/reward relative to the available alternatives to meet their specific financial goals.

Perhaps I’ll dive into this more in the future. I have some interesting information to add onto this point, but I’ll end it with one final thought for the sake of efficiency. I expect that $AAPL $MSFT $AMZN $GOOGL will outperform the broader market for the foreseeable future.

Cryptocurrency:

News spread yesterday when Apple posted a new job listing on 5/25 for a Business Development Manager, specializing in Alternative Payments. In the list of key qualifications, one of the bullet points listed the desire for “5+ years of experience working in or with alternative payment providers, such as digital wallets, BNPL, Fast Payments, cryptocurrency and etc”. With the recent announcement on May 12 that Samsung Galaxy phones can now directly connect to certain hardware wallets and generally manage a users crypto assets, it’s great to see Apple expand their crypto accessibility. While there are many useful applications that can be downloaded in the App Store to support functional crypto use, a built-in system (potentially built within Apple Pay) could be a very interesting new feature.

I find it really exciting to see how adoption continues to accelerate & seeing the different infrastructures being built around the Bitcoin network & general cryptocurrency.

Additionally, PayPal Executive Jose Fernandez da Ponte was being interviewed during Coindesk’s Consensus conference yesterday, in which he announced that PayPal is “exploring how we can let people transfer crypto to and from their PayPal wallets to other addresses”. Since PayPal launched their crypto platform in October 2020, users have only been able to buy/sell a few specific cryptocurrencies, but notably Bitcoin & Ethereum. One downfall of their platform so far is that users can’t send/spend their crypto, a key feature of a digital currency, to another user, a 3rd party wallet, or another blockchain address. As such, the crypto functionality that PayPal offers is quite limited and essentially contained to buying/selling the digital assets as an investment & not as a means of transaction.

On March 30, 2021, PayPal took a big step in the right direction by announcing that customers will soon be able to pay for goods & services with “millions of global online businesses” and merchants using crypto. The company explained that this feature will be rolled out in the coming months, with the CEO explaining that “enabling crypto to make purchases at businesses around the world is the next chapter in driving the ubiquity and mass acceptance of digital currencies”. While this certainly addresses the current inability to complete transactions in crypto on PayPal, da Ponte’s announcement yesterday is another major key advancement in PayPal’s suite of crypto services & functionality. This new rollout would allow a PayPal user to send their Bitcoin & other crypto to another exchange (Coinbase, Gemini, Kraken) or send it to a DeFi platform like Blockfi to lend/stake. Generally, it will allow for more fluidity of coins & allow for private transactions. Other exchanges, like Coinbase, Gemini, Kraken, and others already have this feature.

PayPal’s acquisition of Curv, a cloud-based infrastructure provider of digital asset security, in March 2021 is likely enabling & accelerating the rollout of these new features. I’m hopeful that this newest announcement can be operational by the end of 2021, ideally in Q3.

Until tomorrow,

Caleb Franzen