Edition #71

Deep-Dive of July's Labor Market Data

Hey everyone,

In my last free newsletter on Friday, the focus was entirely dedicated to the stock market & investor psychology during bull markets. The deviation from my standard newsletter format seemed to be a refreshing change based on the feedback that I received & it’s something that I look forward to mixing in more often. I’ll be coming out with an announcement about this on August 16 to explain in more detail. With that said, there was some surprisingly strong labor market data that was released on Friday that I want to dive into, especially considering that there wasn’t any significant news about the stock market or crypto over the weekend. I saw a variety of data & specific information regarding the non-farm payroll (NFP) report for July 2021 that are all worthy of being disseminated & broken down. Let’s dive right in.

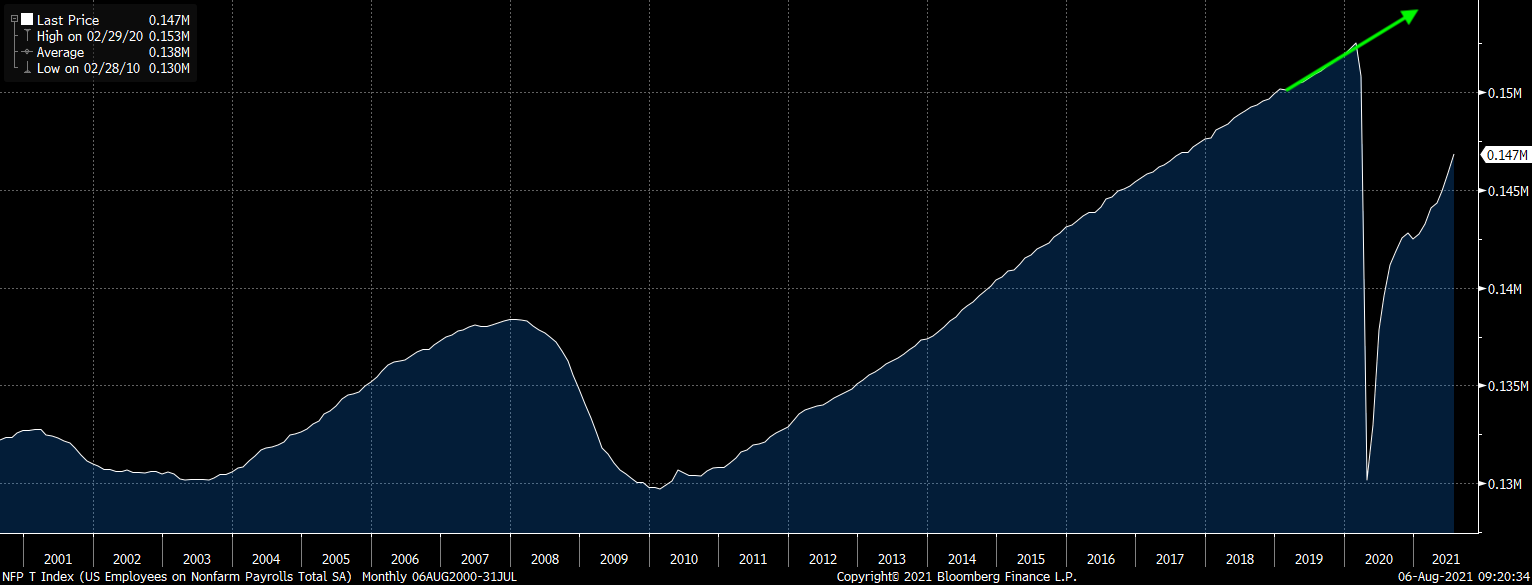

Analysts were expecting for an increase of +858,000 new jobs, but the data came in surprisingly higher at +943,000. Considering that we’ve been covering the weekly filings for initial unemployment claims (which have been extremely disappointing) and also covered the ADP payroll data for July (another disappointment), this was somewhat of a head-scratching result. Nonetheless, it was a welcomed result and represented an acceleration relative to the prior month’s data. With June 2021 initially being reported as an increase of +850k jobs, the figure was upwardly revised to 938k. Both of these are extremely strong reports. Below is a graph tracking the NFP data going back to 2000:

In regard to the headline data, we can dive into the details a bit more to find out which sectors saw the biggest changes in July (vs. change in June):

Leisure/hospitality +380k (+394k)

Government +240k (+169k)

Education, health +87k (+60k)

Business services +60k (+75k)

Trade, transport +47k (+119k)

Manufacturing +27k (+39k)

Construction +11k (-5k)

Retail trade -6k (+73k)

It’s great to see leisure/hospitality continue to roar back & is without a doubt the driving force in the job market recovery. The largest month-over-month acceleration came from the government sector, which significantly outpaced the increase in June. Trade & transport hiring clearly slowed down, but still expanded. As did business services; however, retail not only slowed down but it also contracted. That will be an important sector to track going forward. The positive flip in construction is very encouraging, reflecting a high degree of capital investment.

One concern that I have is that government employment is growing at a faster & faster pace, meanwhile manufacturing + construction is growing at a decreasing rate. The charts below show the divergence between these sectors:

An increase in government jobs are not desirable, considering that they pull capital out of the private sector & create a deadweight loss. Since government operates from two sources of funding, tax revenue & debt, the private sector is needed to support the people working in government. We want capital staying in the private sector & to see an expansion in private sector labor, not in government. This data must be taken with this grain of salt in mind.

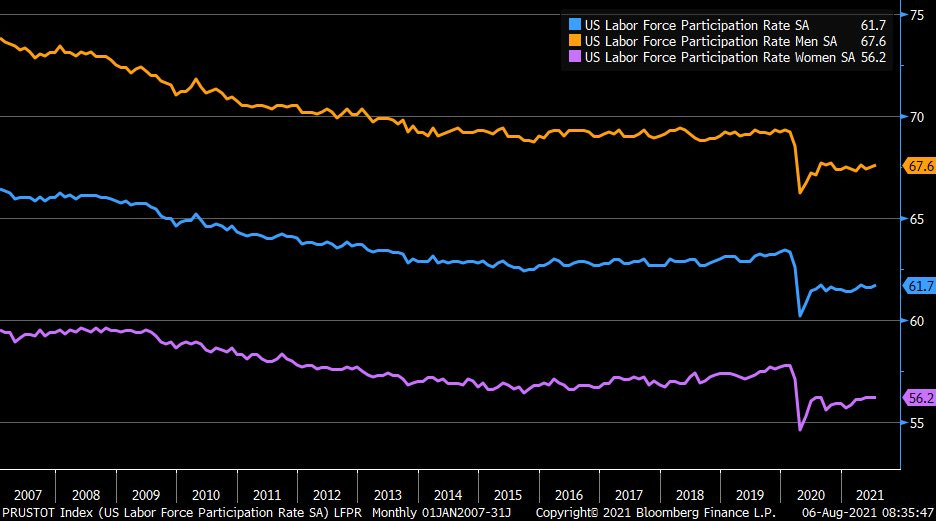

Along with the actual increase in payroll data, this report also included statistics on the unemployment rate and the labor force participation rate (LFPR). As a reminder for new subscribers, in Edition #17 I outlined the non-farm payroll data for May 2021 and wrote the following excerpt about the relationship between the unemployment rate & the LFPR:

“The LFPR simply measures the percent of the working aged population (16 and older) that is currently employed or seeking employment. Essentially, the LFPR takes a broad measure of the entire labor market by calculating how many eligible potential workers are participating in the labor market. When the LFPR decreases, it’s a sign that eligible workers are leaving the labor force and no longer looking for employment opportunities.

As unemployed individuals search for work, but become disgruntled by the opportunities or choose to prioritize their leisure time, they leave the labor force by no longer looking for employment. When they leave the labor force, all else being equal, the unemployment rate should decrease! Considering that the unemployment rate simply takes the number of unemployed individuals in the labor force divided by the total size of the labor force, a decline in the labor force will cause the LFPR and unemployment rate to decrease…

I’d actually prefer to see temporary increase in the unemployment rate due to an increase in the labor force participation rate. In doing so, that would reflect a growth in the participants of the labor market & a competitive environment for jobs. It might also indicate that people outside of the labor force are attracted back to the job market due to higher incentives for work, aka higher wages, benefits, flexible schedules, etc.”

With that framework in mind, let’s analyze the data for July 2021. The unemployment rate declined from 5.7% to 5.4% and the LFPR inched higher from 61.6% to 61.7%. Both of these moved in the right direction, although I would need to see larger increases in the LFPR to be really enthusiastic. In order to get substantial gains in the LFPR, we’ll need to see the unemployment rate tick higher. In my opinion, these results for these two data points are a double-edged sword. On one hand, it’s great to see the unemployment rate decrease, but that can’t happen at the expense of the labor market staying stagnant. We want to see the labor market expanding, not flattening. Monitoring the dynamic between these two variables will continue to be key for the Federal Reserve’s taper timeline, as I highlighted in Edition #17. Here’s some excellent data tracking the LFPR by gender & on the aggregate going back to 2007:

The final thing that I want to note is the average hourly earnings, in which analysts were anticipating an increase of +3.9% relative to July 2020 and the result was +4.0%. This was a good reading, slightly higher than the June result of +3.7%. An acceleration in hourly earnings is a good sign, particularly as leisure/hospitality (which aren’t considered to be high-paying jobs) are making up the bulk of monthly job increases. On the other hand, we must also consider that employers are the ones facing these wage pressures, which are likely to get passed along to the consumer via higher prices. This will likely keep a floor under inflation, which will exacerbate the recent increases we’ve seen in the monthly CPI data. Additionally, as consumers/employees earn higher wages and have higher levels of disposable income, suppliers/producers are able to justify charging higher prices. This essentially creates a double feedback loop. At the end of the day, higher wages are a good thing, but there are always two sides to every coin & we must be considerate of the impacts that these higher hourly earnings could have on consumer prices.

If we look at the historical context of this +4.0% increase, we’re well above the data between 2010 and 2019:

Logically, we had a massive spike in average hourly earnings due to the significant decline in lower-paying service sector positions via layoffs in response to COVID. As these positions continue to come back to the market, I’d suspect average hourly earnings to begin to move back to the sub-3.0% levels of 2010-2018. With more data reflecting that employers are having a hard time attracting skilled labor, the biggest incentive they can give is to increase salaries & provide additional monetary incentives/benefits. As I’ve said on this newsletter, I believe labor shortages will continue through the majority of Q4 2021, which could imply that we’ll see wages continue to rise during that period.

Overall, this was a great report for labor market data. I remain cautiously optimistic, and would rate this report as a B+. It would be in the A range had the labor force participation rate increased by a more substantial margin and if government jobs weren’t such a considerable amount of the month-over-month increase in payrolls. The Federal Reserve will be analyzing all of this data that we just covered at length in order to help them determine where we are on the path towards full employment. I still believe we’re a considerable way away from full employment, but we continue to trend in the right direction. With that said, we’ll need to see continued strength for these monthly reports in August, September and October in order to give the Fed confidence that the economy & market is prepared for tapering.

I am still operating based on my opinion that the Fed will begin to taper in Q1 2022 at the earliest. I think this labor market data supports that timeline.

Until tomorrow,

Caleb