Edition #7 - 5.25.2021

FOMC Projections & Assumptions, Ray Dalio on BTC, and More Transparency on the Blockchain's Energy Consumption.

Economy:

Yesterday morning, the Markets Group of the Federal Reserve Bank of New York released a report for the FOMC titled “Open Market Operations During 2020”. I have yet to read the report in its entirety but found several interesting aspects that were extremely insightful. Some of the most important of these insights came from pages 46 through 50, in which the Markets Group gave their projections & assumptions for asset purchases, liabilities, and interest rates going forward. Here are the primary takeaways from this section of the report:

“The [FOMC] has provided outcome-based guidance on asset purchases, and the size of the balance sheet will evolve along with changes in economic conditions & progress toward the Committee’s goals. As such, the outlook for the balance sheet remains uncertain and the projections presented here are meant to be purely illustrative and to demonstrate a range of possibilities for the path of the portfolio, the size of the balance sheet, and income.”

“The SOMA (System Open Market Account) portfolio could grow through ongoing asset purchases to reach $9.0 trillion by 2023, or 39% of GDP.”

“The projections assume that the portfolio will evolve in four phases: growth, reinvestment, normalization, and organic growth.”

“Treasury and agency MBS purchases [are estimated to] continue at the current pace through 2021 before gradually reducing to zero at the end of 2022. The reinvestment phase, during which principal payments… are reinvested fully into Treasury and agency MBS ends in the fourth quarter of 2025.”

“The median expected level of the effective federal funds rate (FFR) is assumed to be steady at 12.5 basis points (0.125%) through the third quarter of 2023, to rise just over 2% by the end of 2026, and to reach 2.25% in the longer term.”

“Reserve balances also peak by the end of 2022, at $6.2 trillion”.

Quickly, I’d like to address each of these points:

Exactly as I would expect, the FOMC is acknowledging that they are using an outcome-based approach to determine monetary policy. This indicates that they will remain flexible with incoming data & the projections that are provided could be abandoned in the event of better or worse-than-expected economic data/progress. No surprise here.

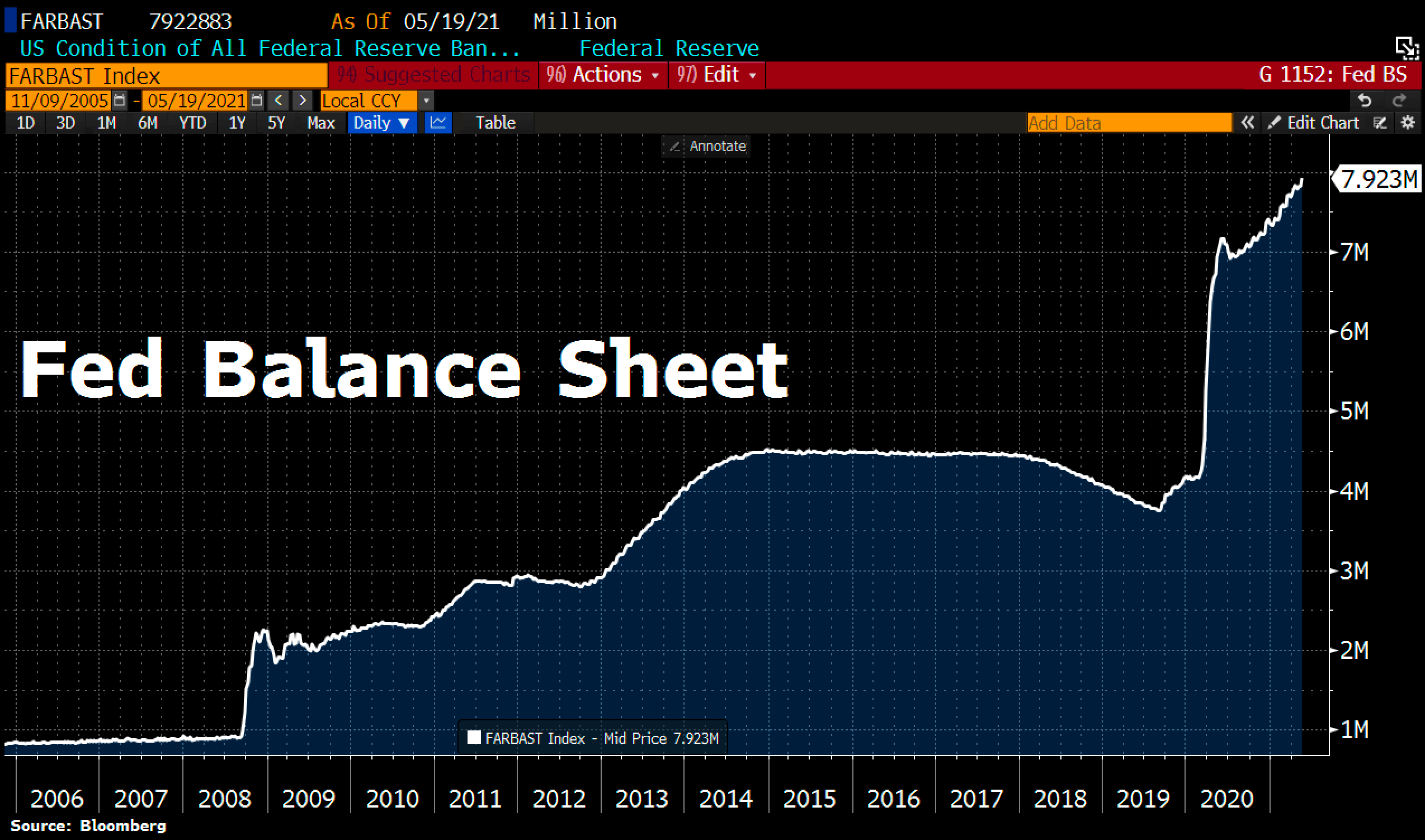

As I’ve continued to reiterate, one of the absolute guarantees that I see in the economy & financial market is a further expansion of the Fed’s balance sheet. At the present moment, here is the historical chart of the Fed’s B/S:

As of 5/19/2021, the B/S increased by $92.2Bn over the prior week & hit new ATH’s at $7.923Tn. Recall, the Fed has committed to purchasing approximately $80Bn/month in Treasury securities & $40Bn/month in agency MBS. For context, it may be relevant to point out that the Fed’s holdings of agency MBS increased by $79.8Bn from 5/12/2021 - 5/20/21, far outpacing their $40Bn/month guidance.

Plenty of market participants appear too eager for the Fed to enter into the normalization period, with far too little regard for the reinvestment period. While this “skip ahead” behavior might be a product of elevated inflation fears, I find this too hasty. Similar to the trajectory following the Great Recession, I think the Fed will stay in the reinvestment period for much longer than the market (and the Fed) initially expected at the start of their QE program. The normalization period refers to the time at which the Federal Reserve will begin to tighten monetary policy & the FOMC will become net sellers of assets. This will theoretically shrink the money supply, increase the federal funds rate & cause financial conditions to become tighter.

Adding to the point above, it appears that the expectation is for the reinvestment period to end in Q4 2025. While I think that’s a fair assessment, I would be more surprised to see this happen sooner rather than later.

In the most recent FOMC minutes from the policy review meeting on April 27 & 28 (my summary can be found here), the median effective FFR between the inter-meeting period was 0.07%. I believe the 0.125% projection is accurate & reasonable, falling in line with potential hikes in 2023. The interesting part of this point is that the Fed believes it will only be able to raise rates to 2% by the end of 2026. Note that during the Fed’s last rate hike cycle, the effective FFR rose from 0.12% in November 2015 to 2.4% in January 2019. They’re indicating that they likely won’t be able to get back to those levels for the foreseeable future. As I continue to reiterate, I believe rates will be lower for longer, with the long-term trajectory having lower highs (ie. not be able to return/exceed prior rate-hike cycle highs). This opinion is contingent on not experiencing hyperinflation or stagflation in the United States, which I don’t believe are the most likely outcomes.

As it relates to total reserve balances, the most recent weekly average of reserve balances held at Federal Reserve banks was $3.92Tn. Considering that the Fed expects to the balance sheet to grow to $9Tn by 2023, it’s quite amazing to see that they expect reserve balances to increase by $2.3Tn by the end of 2022. It seems that they believe a substantial portion of the increase in money supply will largely stay out of the economy & remain in the financial system. I would also agree with that general theme, but the $6.3Tn projection gave me a brief shock.

With all of these points being reviewed, I want to reiterate my optimism on asset price inflation going forward. While I recognize that inflationary pressures are mounting, I am of the opinion that we will experience elevated levels of consumer price inflation over the next 12-18 months, followed by a decline in the rate of CPI inflation back towards the long-term 1.5% to 2.5% trajectory. I remain bullish on stocks, real estate, alternative assets, commodities, bitcoin & ethereum, and dollar-denominated assets.

Stock Market:

I didn’t see any interesting items related to equities, so I’m not going to force the issue. Hopefully something will catch my eye for tomorrow’s newsletter.

Cryptocurrency:

There were two primary headlines that caught my attention today. The first was from an interview with Ray Dalio, the founder and co-CIO of Bridgewater Associates, the world’s largest hedge fund, at the “Consensus by CoinDesk” event. The link to part of the interview can be found here, but Dalio briefly discusses the threat that Bitcoin poses to the traditional institutions (hinting at governments & central banks). Dalio, a long-time Bitcoin sceptic, recognizes that as Bitcoin continues to compete for capital & becomes more of a savings instrument, funds will flow out of bonds and into BTC, which can’t be controlled. Dalio confessed that he “would rather have bitcoin than a bond” and announced that he “owns some Bitcoin”. Credit to Dalio for remaining flexible in his perspective on Bitcoin, but I also agree with his sentiment that “Bitcoin’s greatest risk is its success”, hinting at regulation or punitive policies to suppress the market.

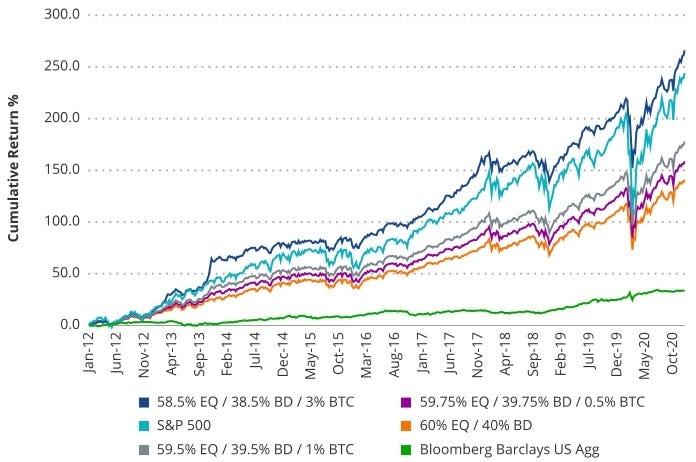

As a way to highlight Bitcoin’s asymmetric return, take the following chart from VanEck, published on March 31, 2021 with data ending 12/31/2020:

A traditional 60/40 portfolio would have generated approximately +140% return from the period between 2/1/2012 - 12/31/2020. Meanwhile, reducing the allocation to 59.5/39.5 and the remaining 1% in Bitcoin would have produced a return of 175% “while only minimally impacting its volatility”. A 1.5% reduction in each the equity and bond exposure, reallocated into Bitcoin for a total allocation of 3% would have generated over 260% return during the same period. That’s not investment advice, but certainly some good food for thought.

The second major news item regarding Bitcoin came from Michael Saylor, CEO & founder of MicroStrategy, and Elon Musk. I’ve attached the relevant tweets below:

As it relates to the controversy surrounding the carbon footprint required to support the Bitcoin network, this is a fantastic step towards improving the use of renewable energy that miners use to validate the blockchain. While I personally have thought that the fear, uncertainty & doubt that has been instilled from the concerns of energy inefficiency were overstated, I’m 100% supportive of having more transparency around the energy that is being sourced to operate the miners & support Bitcoin’s blockchain.

In fact, according to a paper by the University of Cambridge in September 2020, “a significant majority of hashers (76%) use renewable energies as part of their energy mix; however, the share of renewables in hashers’ total energy consumption remains at 39%”. With 76% of bitcoin miners using some form of renewable energy to support their energy needs & the total reliance on renewables being 39%, I’d say that’s a fairly strong ESG score. The paper clarifies that the majority of this 39% is sourced from hydroelectric energy. The paper also mentions that “coal-based mining is principally adopted in regions such as the Chinese provinces of Xinjiang and Inner Mongolia”.

With the increased regulation in China & the announcement to ban Bitcoin (for the Nth time), China’s BIT Mining Limited announced a $25.74 million investment to build a data center in Texas, of which “98% of the total power capacity would be generated by clean & low-carbon energy”. Saylor has even previously discussed the importance of cracking down on Chinese miners to support ESG goals. This is a step in the right direction, as China is the largest culprit of CO2 emissions, has some of the weakest controls on environmental protections, emitted twice as much CO2 as the United States in 2018, and is responsible for nearly 28% of the world’s total carbon emissions.

At the end of the day, the transition towards more clean & renewable energy sources is a net positive, but I think it’s important that we don’t have a double-standard and hold the operations of the Bitcoin network to a higher standard than all else. This initiative by Saylor, and the willingness to listen & learn from Musk, was a pivotal moment in this transition. A council of the leading Bitcoin miners does not compromise the decentralized nature of the Bitcoin protocol & will be used for homogenous & aggregate reporting purposes. These miners are still competing to solve the mathematical calculations & increase their individual hash rates to earn more BTC. It’s important to note that this Council is comprised only of North American miners, at the moment. I’m hopeful that the membership will expand to international miners as well.

Until tomorrow,

Caleb Franzen