Edition #55 - 7.22.2020

Debt/Income of U.S. Cities, Stock Market Conviction, Bitcoin Energy Consumption

Economy:

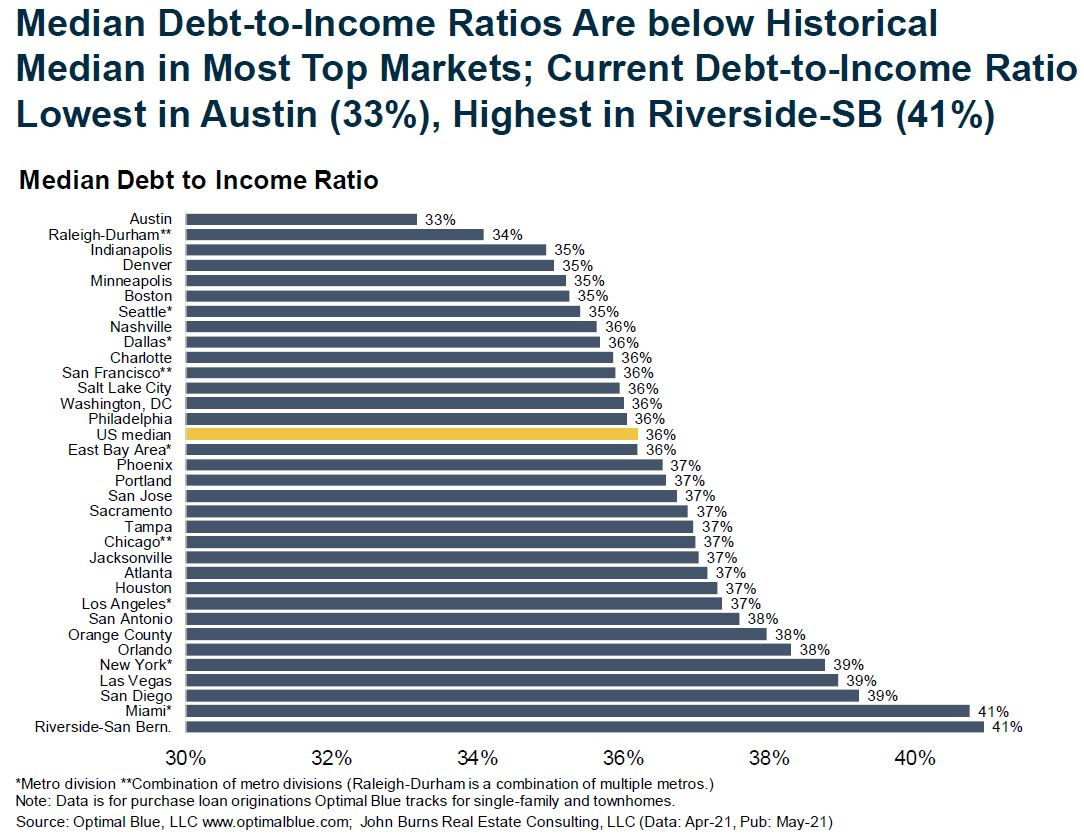

I’ve been spending a fair amount of time lately looking at the housing markets of a variety of cities, partially as a way to evaluate how the housing market data is continuing to develop as a general indicator of economic health. In doing so, one of the things that I’ve been paying attention to is the debt to income ratio of each of the cities that I’ve been looking at.

While it may be a basic measure of financial health, it’s an interesting ratio to evaluate particularly from one city to another. Thankfully, I just recently came across the below chart showing the debt/income ratios of some of the more notable cities throughout the United States:

There isn’t some golden nugget takeaway that I was able to glean from this data, but it can perhaps show some of the markets where real estate is undervalued (low ratio) vs. overvalued (high ratio), or which cities have a population with the best financial health. Thankfully, with interest rates being at/near historic lows, the cost to service debt is also at/near historic lows. As such, having a “high” level of debt can be permissible considering that people can afford to acquire & service the debt.

To hit this point home, here’s an excellent chart showing the monthly principal and interest payments for a mortgage as a percent of the homeowners disposable income:

We can thank the Federal Reserve for making this our reality. Notice the rapid decline since the Great Recession? Prior to the burst of the housing bubble, the Federal Reserve used to conduct monetary policy primarily through the buying/selling of government Treasuries. However, with the sudden lack of buyers of mortgage-backed securities in the wake of the housing crisis, the Fed decided to step into the mortgage market & began buying MBS as part of Quantitative Easing. Since then, the Federal Reserve has amassed a portfolio of mortgage-backed securities currently worth $2.3Tn as of July 15, 2021.

Per the most recent release of the Fed’s balance sheet components, their holdings of MBS increased by more than $11.8Bn over the course of 1 week and have increased by more than $407Bn relative to July 15, 2020. To reaffirm, the Fed has remained committed to purchasing at least $40Bn/month in agency-MBS, as they have done since the onset of the COVID pandemic. At the present moment, the $2.3Tn worth of MBS comprises about 28.5% of the Fed’s total assets on their balance sheet.

Stock Market:

For a period of exactly a week, the stock market saw a substantial increase in volatility & selling pressure. The elevated level of tumultuousness subsided beginning on Tuesday of this week, with the major indexes having two consecutive strong days. In fact, this rebound has been so widespread that more than 90% of stocks trading on the New York Stock Exchange (NYSE) had positive gains on 7/20.

The news of this data led me to see the following chart, provided by Bank of America’s investment research team:

Based on the data going back to 2005, this is a relatively unique accomplishment in the market. If we look at where these “up days” are heavily grouped, it typically happen during a market bottom. We can see a variety of these days at the end of 2008 and the beginning of 2009, as well as at the bottom of the market selloff in 2010 and at the end of 2011. Fast forward to the February/March 2020 collapse from COVID, and we can see several of these 90% up days at/near the bottom. All in all, this is actually a great sign for the market looking out over the next 4-8 months, although new market factors could certainly develop over that time to negate the positive signal.

It’s also worth noting that the NYSE data for 7/21 closed above 80%, but at one point was over 90% intraday. With that in mind, we nearly had two consecutive days of 90% up volume in the NYSE.

Cryptocurrency:

Yesterday was the long-awaited conference called “The ₿ Word”, in which the headline event was a roundtable discussion with Jack Dorsey, Elon Musk, and Cathy Wood. The conference had been on my radar since mid-June when Jack, the CEO/founder of Twitter and Square, had some back & forth with Elon about attending to discuss Bitcoin’s energy consumption.

Aside from the headlining event, there were two hours of other talks held by a variety of experts within the field, which had some great discussion about some of the nuances around Bitcoin & its blockchain. One of the more interesting events was hosted by Nic Carter who addressed many of the recent focus on BTC’s energy usage. Here was my favorite slide from his talk (apologies for the lower quality image):

The data speaks for itself, which is why I don’t really pay any mind or credence to arguments that try to demerit Bitcoin based on energy consumption. Surprise surprise, important things require energy, some less than others apparently.

Until tomorrow,

Caleb Franzen