Economy:

Yesterday afternoon, the Federal Reserve released the newest edition of the Beige Book, which is a summary of commentary on current economic conditions on a nationwide level as well as for each of the 12 Federal Reserve districts. This report is published eight times per year, which helps to give keen insights on the underlying data that the Fed is monitoring to evaluate economic conditions & help to guide policy decisions.

Here are the most important takeaways I noted from the 32-page report:

Overall Economic Activity:

“Supply-side disruptions became more wide-spread, including shortages of materials and labor, delivery delays, and low inventories of many consumer goods” and “many contacts expressed uncertainty or pessimism over the easing of supply constraints.”

“Residential construction softened in several Districts in response to rising costs, while commercial construction was mixed but up slightly on balance.”

“Bank lending activity increased slightly or modestly in most Districts.”

My takeaway: There’s nothing very surprising here in this data & really just affirms what we already know. In my opinion, this means that while the economy is improving, some of the biggest hurdles have yet to be cleared. In a strong recovery, we’d expect to see higher levels of capital investment, strong demand for loans, and easing supply-side constraints.

Employment & Wages:

“Healthy labor demand was broad-based but was seen as strongest for low-skilled positions” and “low wage workers enjoyed above-average pay increases.”

“Labor shortages were often cited as a reason firms could not staff at desired levels, with firms in three Districts delaying expansion or scaling back services due to understaffing.”

“All Districts noted an increased use of non-wage cash incentives to attract and retain workers.”

“Firms in several Districts expected the difficulty finding workers to extend into the early fall.”

My takeaway: This also reaffirms some of the same problems we’ve been talking about & highlighting in this newsletter. Firms are doing as much as they can, under uncertain economic conditions, in order to attract employees. I see a lot of anecdotal examples of restaurant owners raising wages to $15 or $17/hr and still have trouble hiring, or even examples of offering sign-on bonuses of up to $500. With a substantial amount of unemployment benefits set to terminate in September & October, along with health & safety uncertainty regarding COVID variants, I would not be surprised to see labor market slack for the majority of the rest of the year & perhaps even spill into the first quarter of 2022.

Prices:

“Prices increased at an above-average pace, as seven Districts reported strong price growth and the rest saw moderate gains. Pricing pressures… grew most acute in the hospitality sector, as the reopening of hotels and restaurants confronted limited supplies of materials and workers. Construction costs remained high, but lumber prices reportedly eased a bit. Container prices returned to very high levels after having moderated in the spring.”

“While some contacts felt that pricing pressures were transitory, the majority expected further increases in input costs and selling prices in the coming months.”

My takeaway: Excuse my language, but no shit. The 12-month CPI has increased from +1.4% in January 2021 to +5.4% in May 2021. Attentive followers know that I have been keen to discuss dynamics in the lumber market & container/shipping/trucking prices. Once again, this really just reaffirms what we already know to be true, but in a seemingly nonchalant way. The biggest highlight for me is the last bullet point, which seems to imply that the majority of businesses, economists, and bankers (aka “contacts”) are prepared for further increases in input costs, which will in turn be passed along to the end consumer. While the financial markets have been easily persuaded by the Fed that inflation spikes will be transitory, the actual economy seems to be prepared for more persistent higher prices.

The full Beige Book report can be viewed here in its entirety.

Stock Market:

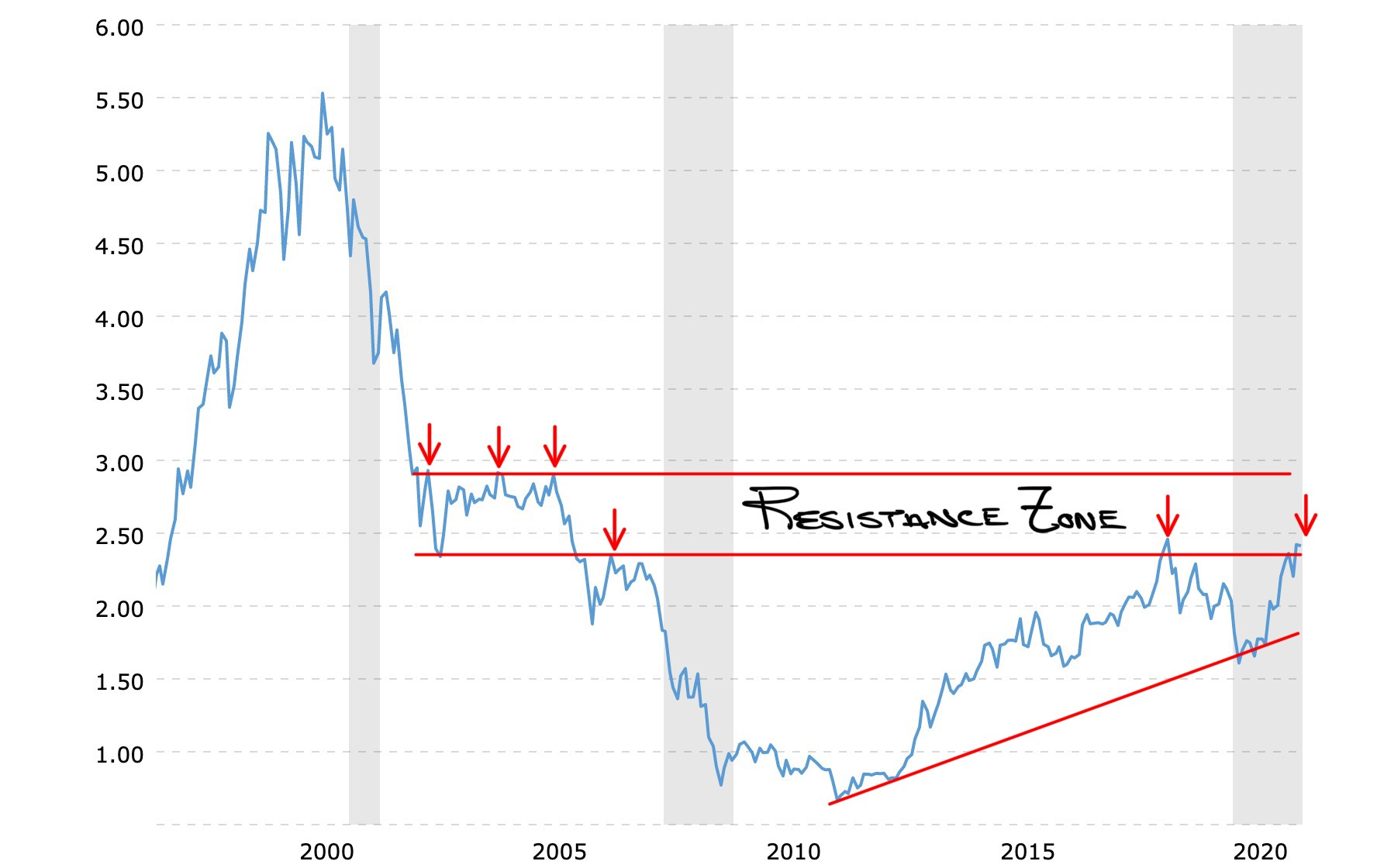

In Edition #37 from 6/30/2021, I posted a graph showing the ratio of Gold/S&P 500. In that post, I was highlighting how the ratio was preparing to make multi-year lows, illustrating how the S&P 500 was significantly outperforming gold in recent years. I wrote the analysis at the time to shine light on the fact that the current market was rewarding risk & willing to accept risk, with seemingly more demand for equities than gold.

Unfortunately, the chart I was sharing only dated back to 2018, so it was hard to discern any historical significance outside of the 3 year range that chart was showing. As such, I wanted to find a chart showing essentially the same ratio with greater historical context. The only difference is that this data is showing the S&P 500/Gold vs. the other way around in my post on 6/30, so instead of making multi-year lows, this chart is showing that the ratio is preparing to create multi-year highs.

After taking a quick look at the trend, I was able to discern a few key patterns, notably the resistance range as shown by the red band. During the initiation of the downtrend in the early 2000’s, the ratio experienced some sideways consolidation & was rejected 3 times at the upper-bound. As the downtrend continued, the ratio was rejected at the lower bound in 2005 before making multi-decade lows. In fact, the ratio reached its lowest level since March 1989 (not pictured). After reaching these multi-decade lows, the S&P 500 began outperforming gold in the wake of the Great Recession until the ratio once again hit the resistance range & was rejected!

Once again, the ratio is retesting this potential resistance zone. Will the pattern of rejection persist somewhere between this 2.4-2.9 range, or will the S&P 500 continue to outperform as it has since 2010? With the S&P 500 currently at/near all-time highs, it’s hard to bet against the strong momentum, but this will certainly be worth monitoring over the next 2-3 months for any potential signs of a reversal or a breakout.

Cryptocurrency:

No update.

Until tomorrow,

Caleb Franzen