Edition #42 - 7.8.2021

Currency & Credit, S&P 500's Correlation to Consumer Confidence, Realized Price Distribution of BTC

Economics:

Because so much of my economic analysis is primarily dependent on monetary policy and I have been outspoken about the Federal Reserves historic levels of money printing & stimulus, it’s easy to jump to the conclusion that I’m predicting the demise of the U.S. dollar. In reality, that couldn’t be further from the truth. While I used to be a devout “gold bug”, courtesy of Peter Schiff’s economic lessons & doom-and-gloom commentary, I recognized that the gold-centric investment style is a poor investment thesis. It also sucks to live life as a pessimist & in a state of fear for an impending collapse.

Therefore, when I discuss monetary policy & the current framework of a low-interest rate environment, I’m doing so in order to substantiate my bullishness on equities & asset prices. One of my top investment rules is to never fight the Fed, which is why I remained optimistic on equity prices even in March 2020 & was a net-buyer of stocks during that time.

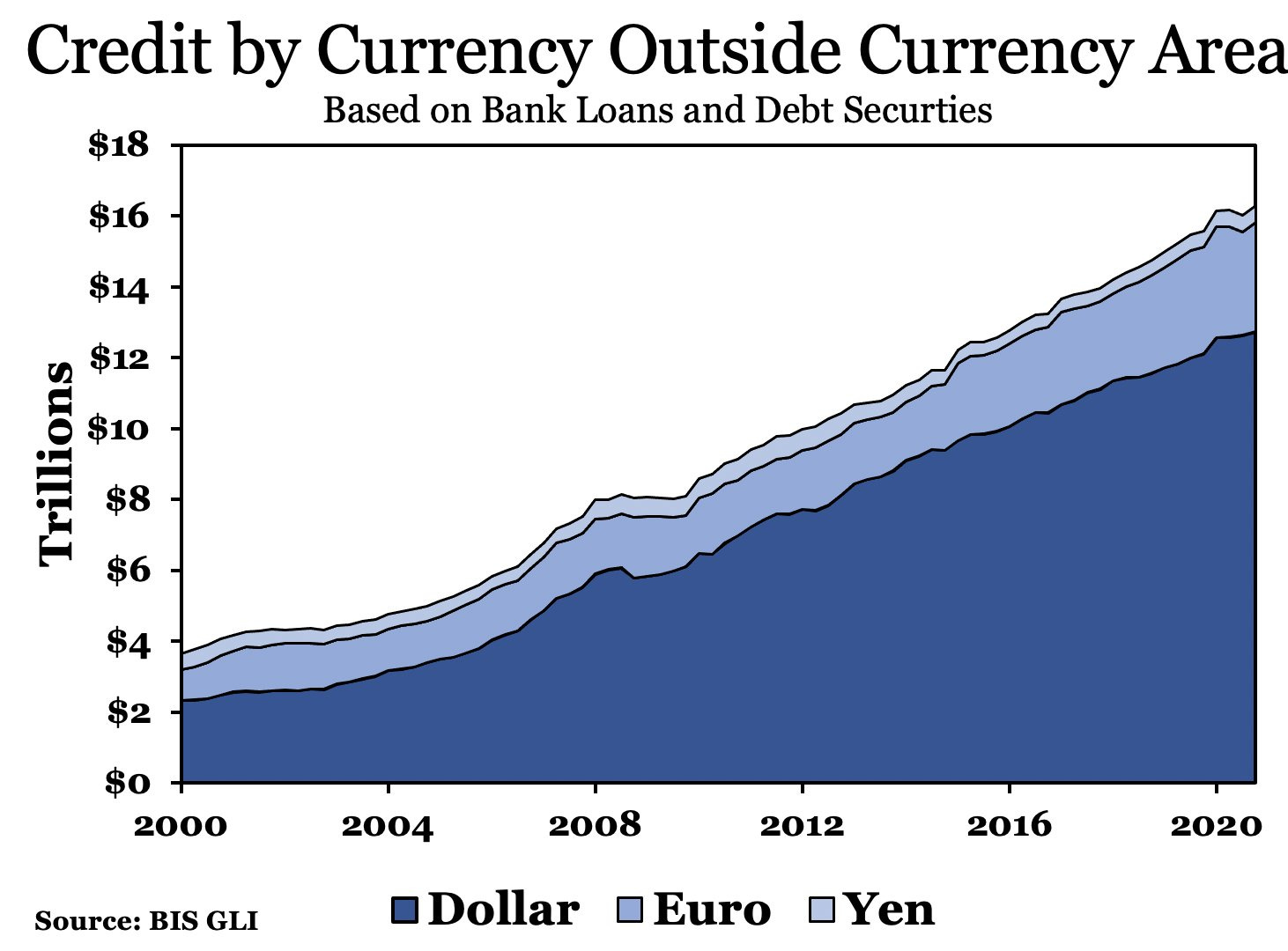

In fact, I truly despise the doom-and-gloom commentary that arises from gold fanatics and I don’t believe that gold or another fiat alternative will threaten the USD’s status as reserve currency for the foreseeable future. Here’s a chart that I saw yesterday which helps to reaffirm & support my opinion, which I had never previously seen or considered:

From a fundamental standpoint, let’s understand what we’re looking at here. Take for example the darkest shaded blue representing the USD. If a business in South America, perhaps a subsidiary of a larger United States holding company, decides to take out a loan in USD, it would be counted in this graph as “credit in a currency outside currency area”. Therefore, we can interpret this chart as foreign corporate demand for USD-financing, then compare USD-financing to the foreign demand for euro and yen-financing. Based on my best alignment estimate, USD credit to borrowers outside of the U.S. (or other countries that have the USD as legal tender, such as Panama, El Salvador, Puerto Rico, etc.) is slightly greater than $12Tn. The euro appears to have slightly less than $4Tn in credit held by “foreign” borrowers, and the Japanese yen has less than $1Tn.

As the world becomes more globalized, particularly since the 1990’s, it’s no surprise to see the upward trajectory of credit held outside of the currency area. The yen has remained remarkably steady in terms of volume over the last 20+ years, and the euro has also kept a consistent pace. With that said, it is interesting to note the composition of these three currencies as an aggregate of their sum. In 2000, the aggregate of the dollar, euro, and yen was slightly less than $4Tn in total credit held outside the currency area, in which the USD comprised more than $2Tn, or roughly 50%. In 2021, these three currencies have an aggregate of roughly $16Tn held outside their currency areas, in which the USD is nearly 75% of the pie. So proportional to the total volume of credit, the dollar’s presence has grown substantially, while the euro and yen have both shrunk on a relative basis.

Essentially, the global demand for dollars continues to remain strong, and increasingly so. This will be a valuable chart to have on hand the next time someone mentions the demise of the U.S. dollar or its status as reserve currency. Individuals and institutions vote with their pocket books, and they favor the USD as a means of business when left to make their own decisions.

Stock Market:

I saw this fantastic chart on Twitter, provided by Chris Weston (@ChrisWeston_PS), showing the correlation between the year-over-year percent change in the S&P 500 (green)) and the YoY % change in consumer confidence. These rolling delta’s are an interesting way to evaluate the data & to prove the correlation.

Dating back to the year 2000, we can see how closely these two measures have moved together: the peaks & troughs occur almost simultaneously. We could extrapolate that investor psychology & consumer psychology are influenced by the same economic & financial conditions, therefore the correlation is reasonably expected. While the correlation in and of itself is interesting to see, it’s even more intriguing to see that these two variables have diverged dramatically since the beginning of 2020.

Often times, traders & economists will refer to these divergences as “alligator jaws” or some other animal, to infer that they will chomp shut (aka converge). Clearly, that convergence can happen in three ways: both compromise their position & move closer to one another, or either the upper or lower jaw shifts dramatically towards the other. I don’t have a crystal ball to know how this dynamic will resolve, but it will be interesting to see how it develops over the course of the next 6-18 months. I’m hopeful that consumer confidence will rise dramatically in Q4 2021, based on underlying economic data & projections.

Cryptocurrency:

This section is truly going to be for the hardcore Bitcoin fans, as it’s certainly an in-depth & nuanced data point. Below is the chart that we’ll be discussing, courtesy of Glassnode:

At its most basic level, this graph is essentially showing the amount of transaction volume conducted at various price levels. UTXO stands for unspent transaction volume, which is still something I haven’t quite wrapped my mind around, but is essentially analogous to 1 BTC. By looking at this chart, we can easily identify three key distributions (bell curves) within the overall price distribution: $650-$15k, then $30k-$41k, and $43k-$64k.

Let’s consider that the current halving cycle, in which the amount of incoming new BTC supply was decreased from 12.5 to 6.25 BTC per block validation (roughly every 10 minutes), was initiated on May 11, 2020. At the time, the price of 1 Bitcoin was roughly $8.7k.

I want to call attention to the grey bar that’s essentially in the middle of the chart, which is at a price of exactly $34.3k. At the time of writing, the current price of BTC is also exactly $34.3k. As we can see, this is one of the largest bars representing transaction volume. This shows that the market is very familiar and comfortable with the price at this level. With the current halving cycle being initiated at $8.7k, the only two levels with higher transaction volume in this current cycle are the $9.7k and $11k levels. We also have strong bars in the $31.7k to $33k range, indicating that these could likely continue to be strong support levels.

It’s almost impossible to tell where buyers/sellers will be comfortable to transact in the short/intermediate future based on the asset’s volatility, but the price structure analysis I have provided on this newsletter seems to agree that these are important levels that will potentially act as support going forward.

Until tomorrow,

Caleb Franzen