Edition #35 - 6.28.2021

Monetary Policy's Impact on Equities, Growth > Value Rotation, BTC Price Action

Economics:

Throughout the brief history of this newsletter, one of the primary topics I’ve focused on in regards to the economy is monetary policy. Quite simply, this is because my investment thesis is largely derived from my views on monetary policy, a topic I wrote about at length in my paper, “Investment Themes & Top Stock Picks for 2021”. I continue to reiterate that I expect rates to be lower and for longer than the market anticipates, particularly if/when inflation pressures begin to subside & inflation expectations have continued to decline.

This was my view when the pandemic commenced last year, as I recognized that the Federal Reserve was about to fire a bazooka of monetary stimulus, which correlates to strong stock returns. As such, I never sold any positions during the pandemic decline in assets beginning in February 2020 & began to purchase relatively conservative ETF’s on March 6 and March 18, 2020. In hindsight those were no-brainer investments (the market bottomed on March 23, 2020), but they were very difficult to make in the moment when the overwhelming narrative was a potential collapse of the entire economic, financial & social systems.

With all of this being said, where do we stand today in terms of the monetary policy that made me so bullish in the midst of the 2020 equity market chaos?

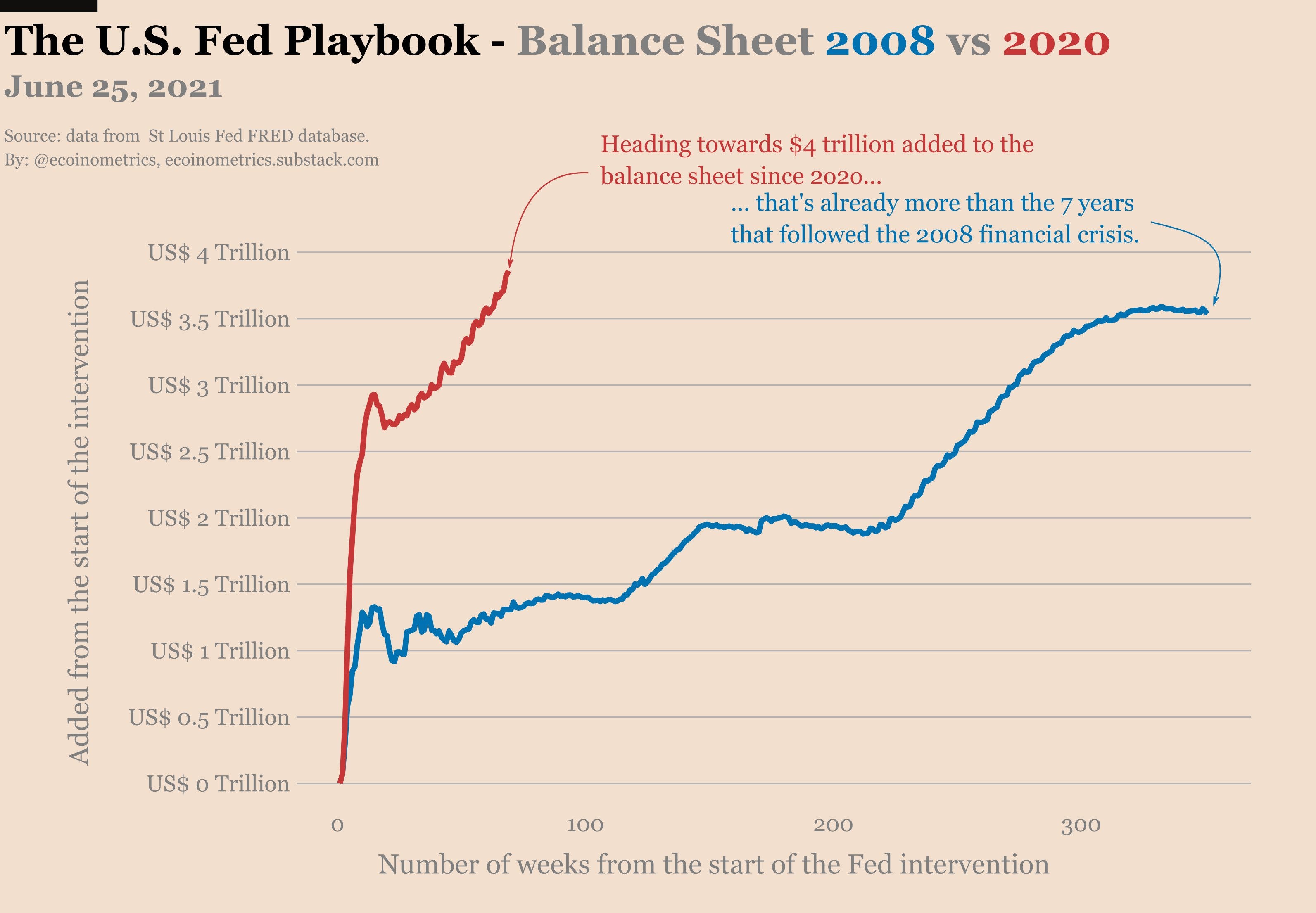

This chart above shows a comparison of the monetary response in terms of the growth in the Fed’s balance sheet (ie. how many assets they’ve purchased, notably U.S. Treasury securities & agency mortgage-backed securities) in the COVID pandemic vs. the Great Recession. Essentially, we achieved the same amount of stimulus at a substantially faster pace. I’m not making any statement on whether that stimulus was right or wrong, and I’m not in a position to make a judgement as to whether or not it is good or bad. However, it certainly explains why this has been the fastest recovery in stock market history, reaching new ATH’s faster than any other bear-market recovery & continuing to accelerate to new highs today. Recall, the S&P 500 achieved a record-high close in August 2020, only 6 months after the start of the bear-market. In the first 65 days from the market bottom on March 23, 2020, the S&P 500 gained +41%. The Fed’s policy, while perhaps being necessary for the well-being of the economy, also carries a substantial price.

In a social & political climate that strives towards equality and inclusiveness, the Fed’s policy should begin to raise some eyebrows in terms of facilitating one of the greatest wealth transfers in history by continuing to accelerate asset prices. I’ve always made the case that the Fed’s low-interest rate policy and asset purchases have had a tremendous impact on widening the wealth gap, considering that the wealthiest individuals in the country are the predominant owners of assets. For greater context, here’s the graph of the Fed’s balance sheet over time:

It’s an interesting dilemma to be in: having to balance economic pressures with economic outcomes. I know that I am not envious of the Fed as they continue to navigate murky waters, and I sympathize with their situation. In the meantime, I keep smiling knowing that they’re helping provide the tailwinds for a continued rise in asset prices. Long assets.

Stock Market:

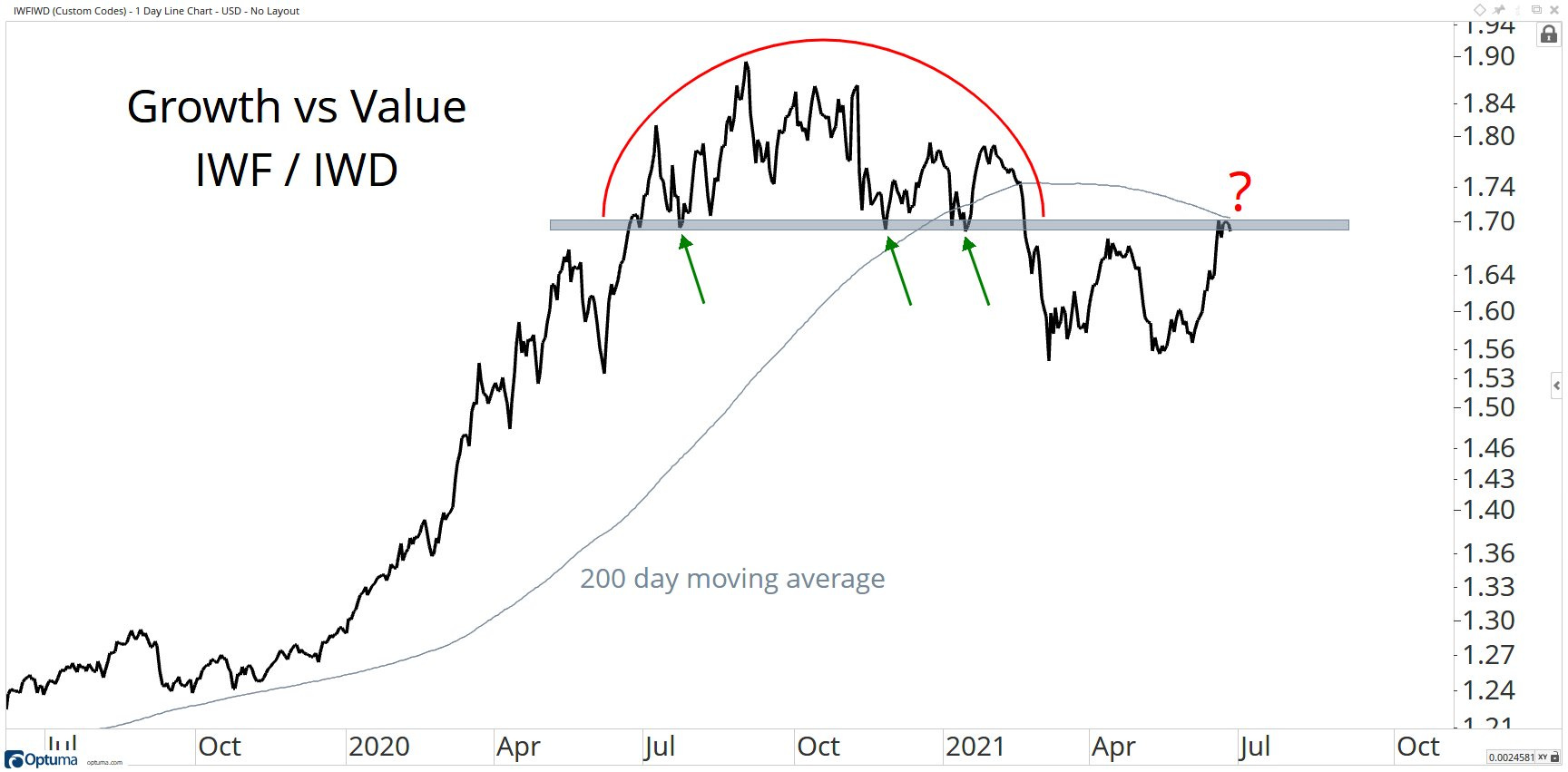

As I continue to highlight the impact of lower inflation expectations, a potential decrease in nominal yields, and continued struggles in the labor market, the tech/growth > value rotation continues to develop in a positive manner. One way we can evaluate this rotation is by simply comparing the relative performance of a growth fund and a value fund!

This chart above does exactly that, allowing us to evaluate & provide technical analysis on the relationship between these themes. No question that the big winner in 2020 was growth, with a massive decrease in the federal funds rate, nominal yields, and inflation. We can see a rounded-top here, which isn’t particularly insightful in and of itself; however, with the context of the grey area it can be rather important!

We can see that the grey range acted as support on three, and nearly four, separate occasions over the last 12 months. With the mass exodus out of tech/growth in the February 2021 yield tantrum, growth stocks evaporated in favor of value and the relationship between these two ETF’s pierced below the support level. The relationship “bottomed” in March 2021, which was retested again in May before accelerating higher in June.

We’re at an inflection point right now, indicating that this week could provide a meaningful direction for the growth vs. value debate. I often say that prior resistance can become future support, typically when referring to breakout structure strategies, but the opposite also holds true: prior support can become future resistance! If growth, as represented through $IWF, can outperform value over the next 1-2 weeks, we may be gearing up for another substantial move higher in this ratio.

Cryptocurrency:

No major update here. As of the time of writing, the price of BTC is currently $34.4k. The price structure that I have repeatedly shown via this newsletter & on Twitter continues to act as a guideline for price movements. Fundamentally, I remain hyper-bullish on Bitcoin. In terms of technical analysis, I need to see either a breakout or breakdown in order to decide on a bullish/bearish sentiment. Until then, the price action in between the white channel is essentially no-man’s land. You could now make the case that the yellow line is the “support of last resort”.

Until tomorrow,

Caleb Franzen