Edition #33 - 6.25.2021

Infrastructure Deal, Strongest Bull Market Start Ever?, Bitcoin in Practice

Economics:

The biggest news in regards to economic impact was the announcement of the long-awaited infrastructure agreement. The full fact sheet, provided by the Biden administration, can be found on the White House website here. There has been a lot of drama surrounding the infrastructure plan, with Senate Democrats pressing for a $6Tn plan (lol) last week, seeming to be much more of a posturing for political theater. Comments from GOP leaders were combative & not necessarily constructive, so it’s great to see that a “bi-partisan” agreement/plan has come to fruition. There’s still limited info about the plan, but here is what I’ve been able to dig up so far:

The size of the deal is for $1.2Tn in spending, aimed at improving, modernizing, and expanding the transportation systems (road, railways, bridges, public transit). The deal will also address an expansion of broadband infrastructure, EV charging stations, and clean water provisions.

It’s a sizable plan, which will certainly provide a boost to jobs & have the potential to create long-term efficiencies & improvements. As with all government programs & proposals, a plan is one thing, but the execution can be an entirely different story. From a political standpoint, this will be a big point of emphasis for the Biden administration to hang their hat on if/when he runs for re-election in the next cycle. With a significant theme of the proposal being clean energy, climate change, etc., this could be a big badge if accomplished successfully.

In terms of the impact for financial assets, I don’t think this necessarily carries any weight or significance for a specific asset class or the market overall. Yes, some companies will win bids to carry out parts of the building, construction & development. However, I don’t have a crystal ball to know which companies specifically are set to benefit. Some that immediately come to my mind are $CX (cement), $BLNK (EV charging), and $URI (construction equipment). None of these are investment advise.

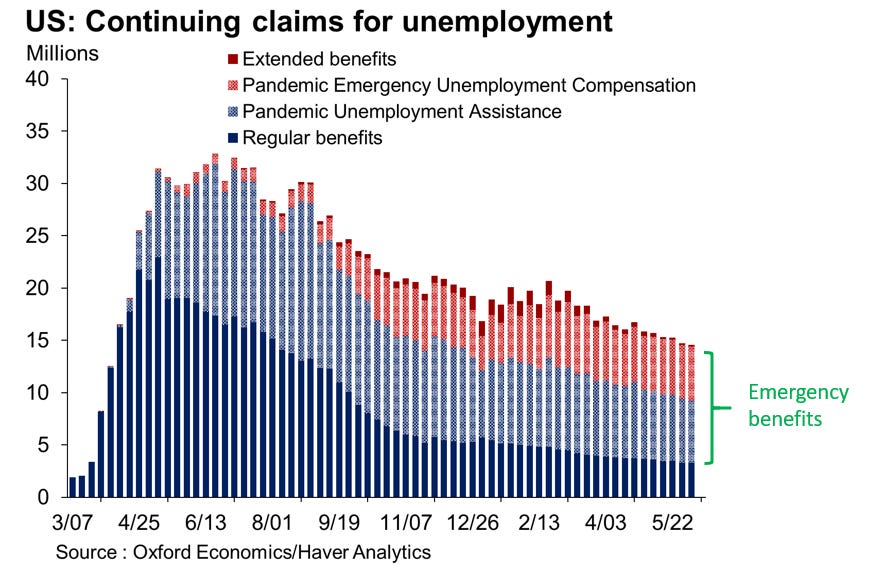

Unrelated to the infrastructure plan, I also wanted to acknowledge the updated weekly figures for initial unemployment claims & some data on unemployment insurance benefits as well. For the week ending June 19th, the seasonally adjusted claims were 411,000 vs. expectations of around 380,000. Additionally, the prior week’s figure was revised higher from 412,000 to 418,000. This was another unfortunate miss in the weekly initial unemployment claims figure, showing further proof of slack in the labor market and a deceleration in the labor market recovery.

Here’s a fantastic graph showing the amounts of unemployment insurance since roughly the start of the pandemic in March 2020. Emergency benefits continue to comprise the majority of unemployment insurance disbursements, although regular benefits have now fallen dramatically from the situation in April - September 2020.

Based on the data, there are currently 3.3M people on regular benefits, 5.5M people on long-term benefits, and 6M on Pandemic Unemployment Assistance (PUA) for a grand total of 14.8M claimants. With a civilian non-institutional labor force of 160.9M as of May 2021, that means that roughly 9.2% of the civilian non-institutional labor force is currently unemployed & collecting insurance benefits. This is why looking at the labor force participation rate, currently at 61.2% as of May 2021, is so important to consider alongside the official unemployment rate data.

Stock Market:

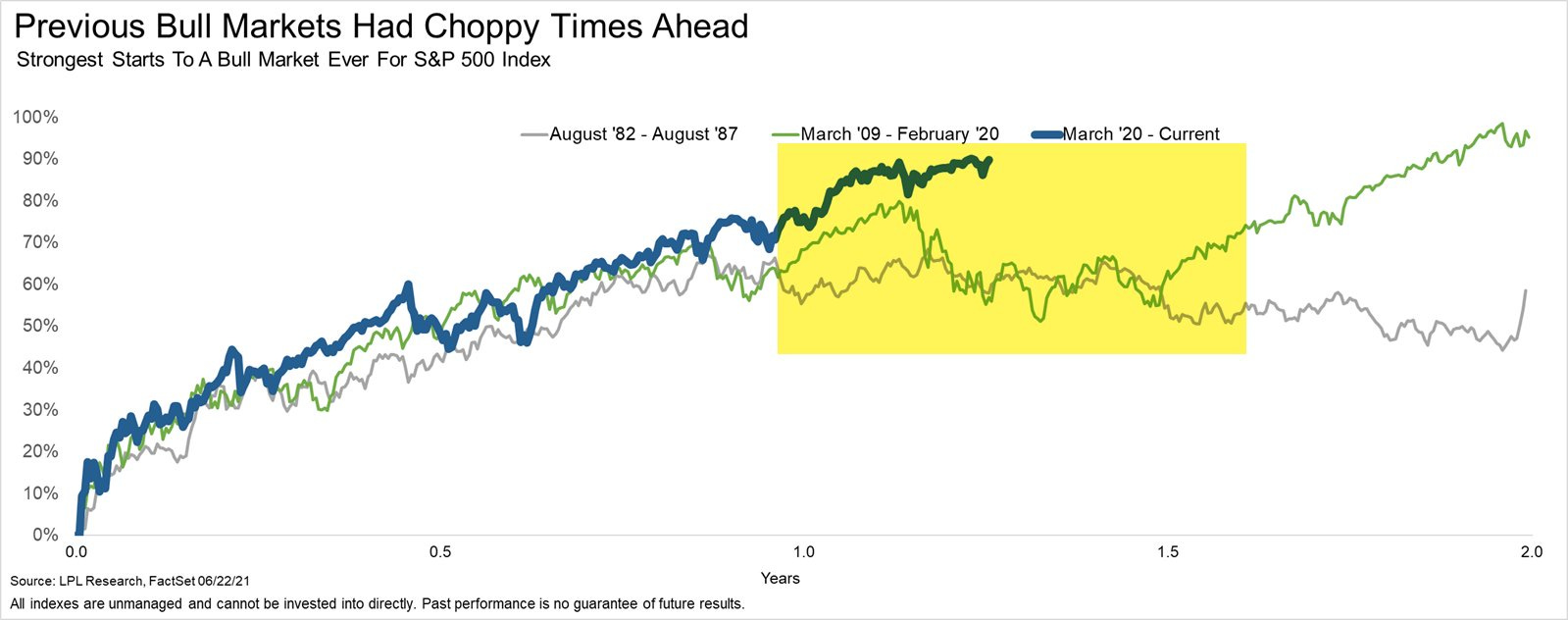

Back in February of this year, I saw an excellent chart from LPL research, overlaying the beginning of the last three bull markets on the same graph. The point of the chart was to show how U.S. equities have historically hit bumpy roads around the 10-13 month mark after stocks bottomed in the bear market cycle. The chart showed that U.S. equities had historically hit an invisible wall and began a downward/sideways consolidation for the next 4+ months, hinting towards the potential for choppy market conditions. As someone who trades & invests based on momentum indicators, choppy markets are a nightmare scenario. Breakouts become failed breakouts, and retests of critical support levels tend to get cut like a hot knife through butter.

Within a week after seeing that graph, the equity market had a tantrum due to the persistent rise in nominal yields. After letting the market correct for a few days, as I wasn’t necessarily worried at the onset, I quickly moved to a majority cash position by exiting positions at solid gains, minor gains, and in some cases, losses of up to -20%. This intentional liquidation was not fun and was full of uncertainty at the time, as I was unsure how the dust would settle & how long it would take. Some of those positions that I sold at losses, such as $EXPI and $JMIA, continued to fall an additional -40% or worse over the proceeding months. Losses aren’t fun, but “holding the bag” isn’t ideal either.

While tech stocks & companies with high revenue growth expectations got punished during this period, investors flooded into “value” stocks with consistent & stable profitability, a track record of dividend growth, and generally had clean balance sheets. The rise in yields also prompted a rotation into financials, energy, and basic material sectors. As such, while the Nasdaq experienced significant pressure, the Dow Jones continued to accelerate higher and the S&P 500 also managed to rise.

Within two weeks of selling the majority of my positions, I was fully-allocated back in the market but shifted away from tech/growth & into financials, energy, and small-cap value stocks. This has been the focus in my portfolio now for the last several months, up until the last 2 weeks in which I have finally rotated back into tech/growth, based on the encouraging data that I’m seeing & have covered here on this newsletter.

So where is that chart today, and did the current bull market align with the prior two cases?

As we can see from the data, the bull market beginning in August 1982 began to experience sideways consolidation after “being born” for 10 months, then didn’t start to gain upward momentum until 14 months later. Similarly, the March 2009 bull market didn’t begin to consolidate until after the 1-year mark, around 13 months in, but had a snappier recovery just a few months later. At the time I had initially seen the chart, the current bull market was only 11 months old, and you can identify the brief rollover just before the 1-year mark. Since the lows from the -5.7% maximum drawdown of that consolidation, the S&P 500 has gained +14.5% as of yesterday’s close.

The bull market is in full effect, and barring any substantial deterioration in the economy or financial system (extremely unlikely in my opinion), I suspect all consolidations of -5% to -10% will be quickly gobbled up before making an extension to new ATH’s.

Cryptocurrency:

I watched a great mini-documentary on YouTube, approximately 12 minutes long, that shines some light on Bitcoin adoption in the country of El Salvador. Considering that the bill to make BTC legal tender in the country was passed earlier in the month, this marks a milestone in the history of Bitcoin & cryptocurrency in general.

I think as Americans, or at the very least, members of a developed economy, we find it hard to understand how a country could have 70% of its population not linked to the banking system, and thus find it difficult to acknowledge some of the practical aspects of Bitcoin. Considering our financial system generally works well, although I’d make the case that BTC accomplishes the same ends in a more optimal means, many Bitcoin skeptics aren’t able to comprehend the magnitude of the innovation for members of 3rd world countries. I touched on some of BTC’s optimality in a post yesterday afternoon after seeing comments from the Federal Reserve’s John Williams, stating that he was “struggling to understand what payments problem cryptocurrencies address” and that it’s “not a store of value either”. My response was noted by Mace News, an independent news source, which was an exciting development to be quoted by them. Here was their tweet that captured my response back to Williams.

Regardless, I highly encourage you to watch the video below - I found it informative & thought it gave a brief glimpse into the future.

Until next week,

Caleb Franzen