Edition #31 - 6.23.2021

Correlation of USD & Commodity Index, Nasdaq-100 Technical Analysis & Breakout, Crypto Adoption Curve

Economics:

There are a few things that I want to highlight in this section of the newsletter, as I’ve been seeing great data & charts that I want to share. I just got done watching Jeffrey Gundlach’s “Total Return Webcast” from 6/8/2021, but was posted to YouTube on 6/18. Jeffrey is one of the preeminent asset managers in the world, with AUM of $135Bn as of 3/31/2021, and has earned the moniker “The Bond King” due to his early-stage career trades in the U.S. fixed-income markets. He’s one of my all-time favorite investors and someone who I always listen to when he gives infrequent interviews. Due to intellectual property constraints, I can’t post the chart here on this newsletter (I have reached out to the DoubleLine team to receive permission for the future), so I highly recommend that you click the following link and skip to the 33:19 mark of the video.

The chart that DoubleLine is providing shows the relationship & correlation between commodity prices and the inverse U.S. dollar index, and you’ll quickly notice that the correlation is extremely high. The reason why I wanted to bring this up is that commodity prices have risen dramatically due to supply chain bottlenecks & overall inflationary concerns. Meanwhile, the same inflationary concerns & dramatic increase in monetary supply have pushed the dollar substantially lower over the last 18 months. Recall, more than 35% of all U.S. dollars to have ever existed were printed out of thin air in 2020, so it’s logical to expect that the value of each dollar in circulation would be worth less (or should I say worthless?) Jokes aside, this is a perfectly-expected correlation.

Based on my views of continued levels of elevated inflation, likely ranging from 3% to 8% on a rolling 12-month basis, for the remainder of 2021 and into the first half of 2021, I believe that the most likely scenario is for the dollar to continue to decline & for commodities to continue to rise. We’ve seen a sharp downfall in commodity prices over the last month, notably with lumber prices, industrial metals, agricultural feed, etc., but my impression is that we’ll start to get a clearer idea of the winning & losing commodities now. I’m particularly more bullish on industrial metals & crude oil to continue to rally, or show relative strength compared to the broader commodity index, for the remainder of the year. Here’s a chart showing how significantly the prices of soybeans, corn, and wheat have fallen from their recent ATH’s:

I don’t necessarily believe these will fall too much further; however, the immediate trend is negative so I don’t want to bet against that. In terms of the U.S. dollar, I don’t expect much of a change, although I do have a negative bias. Foreign exchange and currency evaluations are so difficult to predict, and I won’t pretend to be an expert in that realm. With monetary policy driving the majority of my investment thesis, the value of the dollar is variable to U.S. monetary policy, as well as the comparative monetary policy of other major OECD countries. Aside from maintaining knowledge on the monetary policy of the Bank of Japan, Bank of England, and the European Central Bank, all of which are substantively accommodative, I’m practically unaware of the monetary policy of other economies.

In any event, my views are broadly: commodities up, dollar down until data begins to prove otherwise or shift economic expectations/dynamics.

Lastly, because inflation expectations have been a consistent topic over the last few weeks, I wanted to provide a chart that I saw on Twitter from @DavidBeckworth.

This chart helps to contextualize the recent rollover in inflation expectations, particularly since the May 2021 inflation data was released in mid-June.

Stock Market:

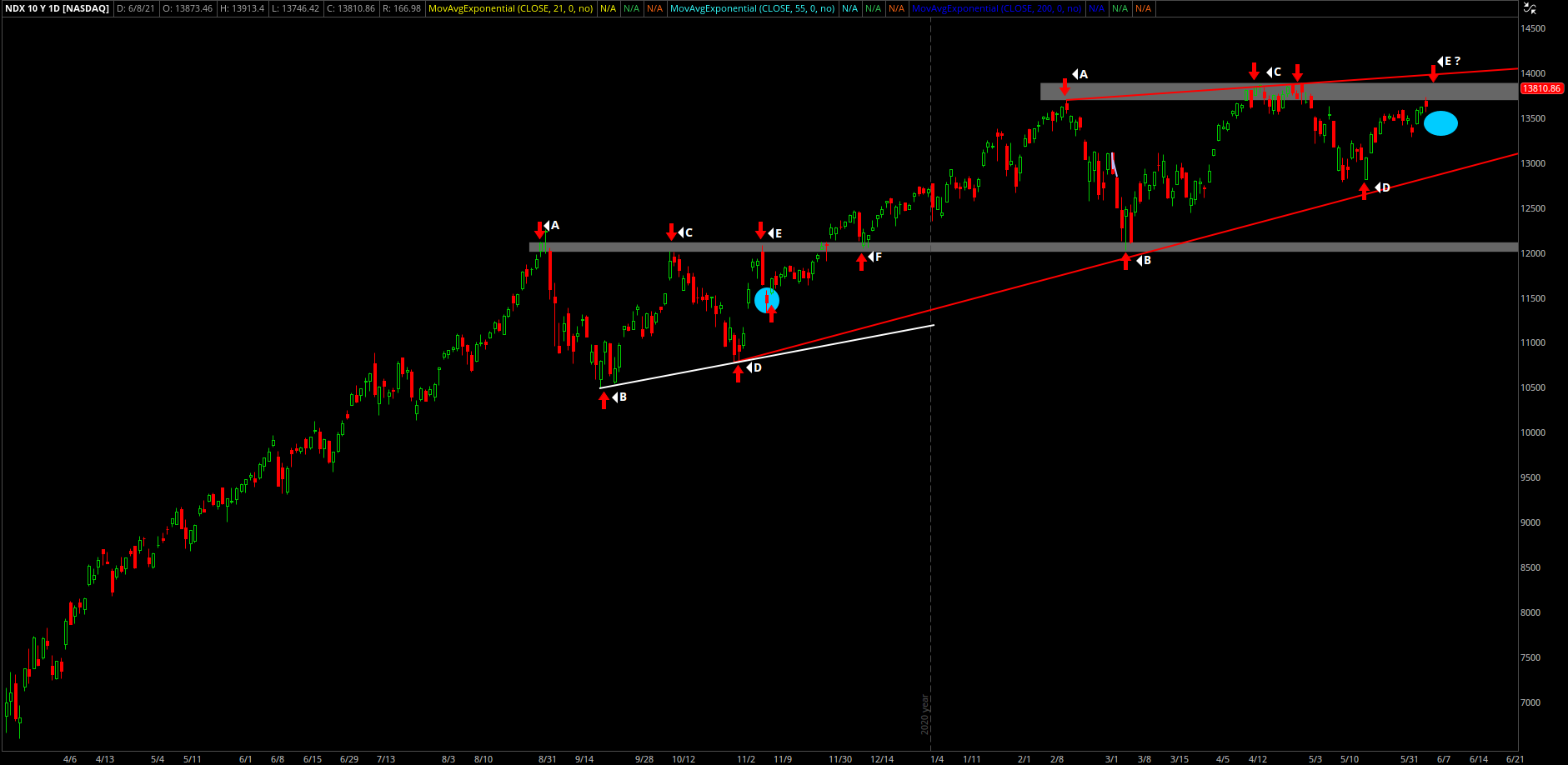

On 6/9/2021, I shared the following chart of the Nasdaq-100 index as a way to share my thoughts & views on the broader tech market.

In that newsletter, Edition #19, I explained that the current price structure that formed in 2021 was eerily similar to price structure in September - December 2020. To close my thoughts at the time, I provided the following analysis:

I think it’s entirely possible that price is able to continue to rally & breakout of the grey zone for new ATH’s. However, I am also prepared that we are currently retesting a prior resistance level that has been confirmed from two previous retests. As such, it’s very possible price gets rejected from here again, at which point I’ll be looking for signs of a potential upside reversal, particularly at the rising red trend line at the lower-bound. Similar to the consolidation pattern in 2020, a breakout will potentially be subsequently followed by a retest of the previous resistance level, in which that same grey level will attempt to act as support. It may fail, or it may hold as it did on 12/10/2020 (point F).

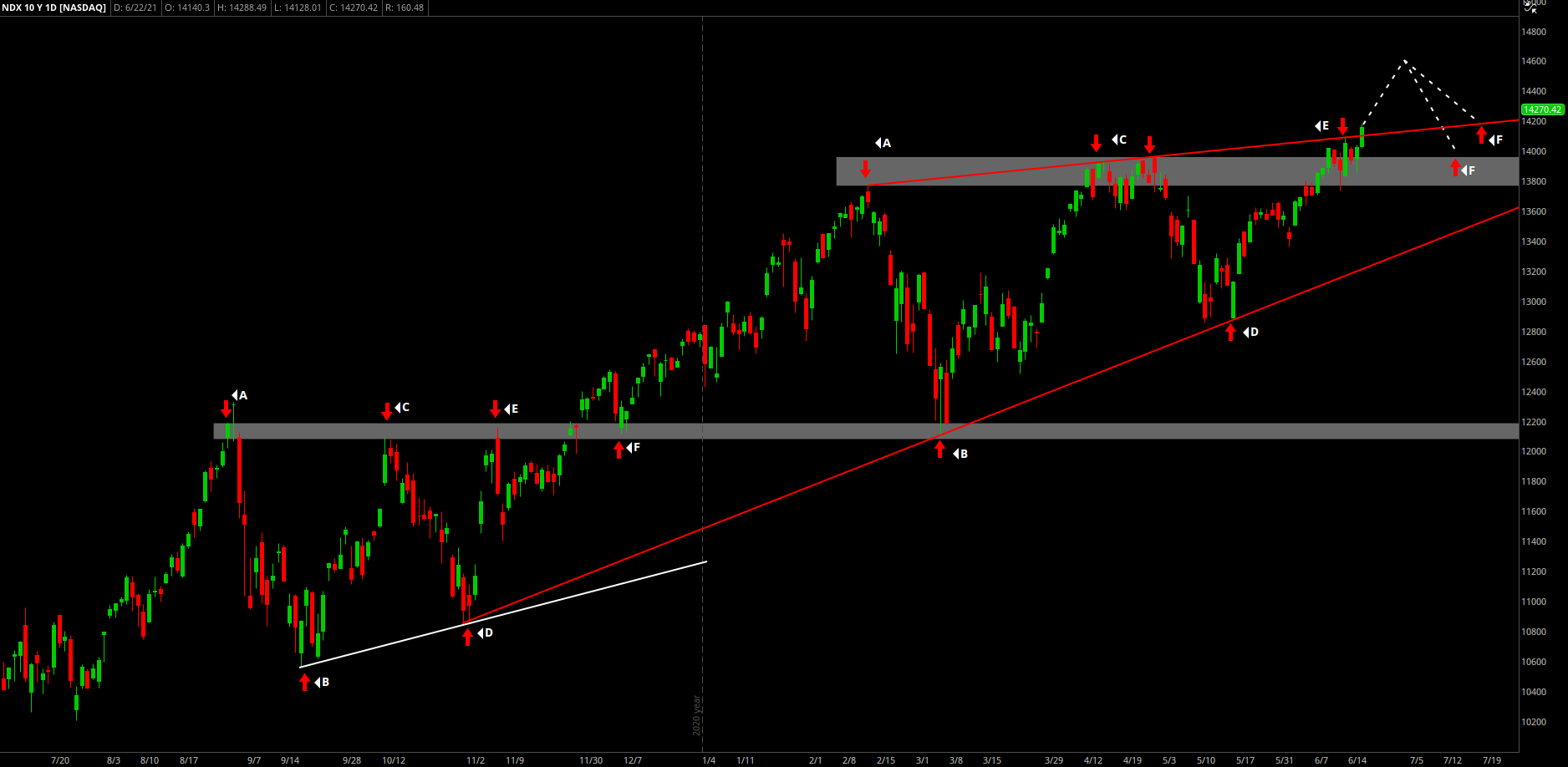

Here is the update based on the closing price as of 6/22/2021, zoomed in:

As we can see, the price of the index did face some overhead resistance at the top end of the range (Point E), in which price consolidated back into the grey range before continuing higher. In yesterday’s trading session, the $NDX gained 0.94% and outperformed each of the other major indices. As we can see from the price structure that I have drawn, price is successfully breaking out of the red resistance trend line, in which price was rejected on at Point A (1x), Point C (2x), and briefly at Point E, closing at new ATH’s.

First of all, this is an excellent sign to prove the tech/growth > value rotation that I’ve begun to highlight more frequently. As I’ve mentioned, I’ve started to reflect that rotation in my own portfolio since the beginning of last week. Premium subscribers will see which companies I’m investing in at the present moment to reflect these changing dynamics.

Second of all, the current price structure continues to rhyme with the price structure of September - December 2020. As such, I believe that the most likely scenarios are what I have drawn in dotted white lines. This is a common trading strategy based on breakout price structure, in which a trader will wait for shares to retest the prior resistance trend line in order to initiate a new long position or add to an existing long position (Point F). I have even outlined this price structure before in a recent newsletter, Edition #28, where I highlighted how I trade breakout, retest & continuation trends.

I believe that the height of the dotted white line is going to be a reasonable level for prices to reverse, based on a fibonacci retracement from the swing-high to swing-low extension from the correction on 4/29 - 5/12. At the same time, I don’t have a crystal ball, and my technical analysis only provides me with a potential path forward & a methodology for setting expectations & possible outcomes.This pattern, applied to what I’m seeing in $NDX, implies that price could rise +3.4% over the coming 7 days before experiencing a minor consolidation towards the grey range. As I’ve said before, what was once prior resistance, can act as future support. My expectation of that consolidation ranges from -2.5% to -5.5%.

I continue to expect the Nasdaq to outperform both the Dow ($DJX) and the S&P 500 ($SPX) in the short & medium-term, and my trading activity is reflective of that belief. As I said last the last time I provided Nasdaq-100 analysis, “I’m excited to see how this pattern continues to develop!”

Cryptocurrency:

Very brief thoughts on the general macro view of cryptocurrency, particularly in light of the nasty correction that we experienced yesterday morning that pushed the price of BTC below $29k for the first time since 1/21/2021. At their core, digital currencies are merely a technology. Some have niche use cases, some are application systems, some are financial operating systems, pure blockchain ledgers, memes, decentralized vs. central governance, digital collectibles, etc. Whatever your view is on cryptocurrency, the concepts of smart contracts, decentralization, digital transferability, and the accurateness of the ledger are all undeniable innovations, particularly in the realm of finance & monetary networks. Aside from the speculation that does occur in the space, just as it occurs in the equity market, there is real value & innovation being recognized in this asset class.

In many ways, the growth & potential impact of crypto echos the same dynamics of the internet. To quote my favorite economist, Paul Krugman (sarcasm):

I’ve gotten into some spats with Krugman before on Twitter, which I’ll perhaps share in a future newsletter, based on some fundamental disagreements about the economy, but this is arguably one of the worst predictions of all-time in terms of the impact of a specific innovation. The reason why I’m bringing this up is because I saw a fantastic chart from Raoul Pal (@RaoulGMI on Twitter), where he compares the adoption curve of cryptocurrency & the internet in logarithmic scale.

As I continue to say, we are extremely early in the game. Perhaps as early as the 2nd or 3rd inning. Keep in mind, Bitcoin was created in January 2009 and reached a total market cap of $1Tn (at a price of approximately $55k/BTC) within 12 years and 2 months. Conversely, the first company to ever be valued at a market cap of $1Tn was Apple on August 2, 2018. Apple was founded in April 1976, so it took 42 years and 4 months to achieve the same accomplishment, or nearly 3.5x as long as Bitcoin.

Even at the current value based on a price of roughly $34k, the Bitcoin network is valued at $632Bn and is larger than every company in the United States other than Apple, Microsoft, Amazon, Alphabet (Google), Facebook, and Berkshire Hathaway. Outside of those 6 companies, Bitcoin is valued more than literally every other company in the U.S.

I plan to touch on this further in future newsletters, but I highly recommend researching & understanding Metcalfe’s law, network effects, and exponential adoption curves. This video, also by Raoul Pal, is a great start.

Until tomorrow,

Caleb Franzen