Edition #3 - 5.19.2021

Real Yields, S&P 500 Chemicals Index, MicroStrategy Buys More BTC

Economy:

Courtesy of Lisa Abramowicz on Twitter (@LisaAbramowicz1), here is the YTD chart of the real 10-year Treasury yield. The real yield is given by the nominal yield of an asset & adjusted by the rate of inflation. Simply: real yield = nominal yield - inflation.

One of the most important things to note is that the real yield has been negative, indicating that 10-year Treasury holders would be losing purchasing power since the interest payments earned by the asset are decayed by the inflation rate. So why would an investor accept a negative real return? Either the investor believes that rates are going to fall lower (which would cause the value any asset to rise, all else being equal), or they expect that the value of the currency is going to fall by more than the negative real rate. In each scenario, the investor would benefit from a further decline in yields compared to maintaining their cash position. I’ll likely cover the topic of negative yielding assets in future newsletter.

Either way, the cash flows generated by the Treasury are negated by the inflation rate. While the 10-year Treasury has had negative real returns before, the real yield flipped negative in January 2020 & consistently remained negative for the rest of the year, reaching a low of -1.08% in August. On the 2021 YTD chart above, we can see a rapid spike mid-February which was prompted by a spike in nominal yields that accelerated from 1.15% on 2/10 to 1.54% on 2/25. While nominal yields have continued to rise since 2/25, reaching a high of 1.74% in March & are currently 1.64%, real yields have consistently declined since mid-March. Because we understand the dynamics of how to calculate real yields, this is easily explained by a more substantial increase in the inflation rate!

The 12-month change in the Consumer Price Index (CPI) has been the following for each month YTD:

January 2021: +1.4%

February 2021: +1.7%

March 2021: +2.6%

April 2021: +4.2%

Essentially, the 12-month inflation rate has increased by 3x YTD. It’s also worth noting that April’s YoY inflation of 4.2% was the highest since 2008 & was the first time the YoY change was greater than 4% since September 2008.

Because real yields are a good way to evaluate financial conditions, low yields (and particularly negative yields) are often synonymous with “easy” or “loose” financial conditions. Low interest rates imply an abundance of liquidity, in which potential borrowers have easy access to capital & the funds that they borrow have minimal debt service costs! Often times, members of the Federal Reserve & economists will mention that they don’t want to see the economy “overheat”, a term used to indicate overwhelming growth & high inflation. With GDP expected to continue to rebound & retail sales hitting ATH’s, nominal yields will likely need to rise further in order to counter-act “overheating”, according to traditional finance/economic theory. While I think yields will certainly push higher (I’m not sure how much higher), I don’t think the Fed will let them rise too far as they continue to maintain record-high levels of asset purchases. They will have to taper eventually, but recent comments from Richard Clarida (Vice Chairman of the Fed), Raphael Bostic (President of the Federal Reserve Bank of Atlanta), and James Bullard (President of the Federal Reserve Bank of St. Louis) indicated that they think it’s too early to think about reducing the FOMC’s pace of asset purchases. It will be interesting to see how this plays out as more economic data is released.

Stock Market:

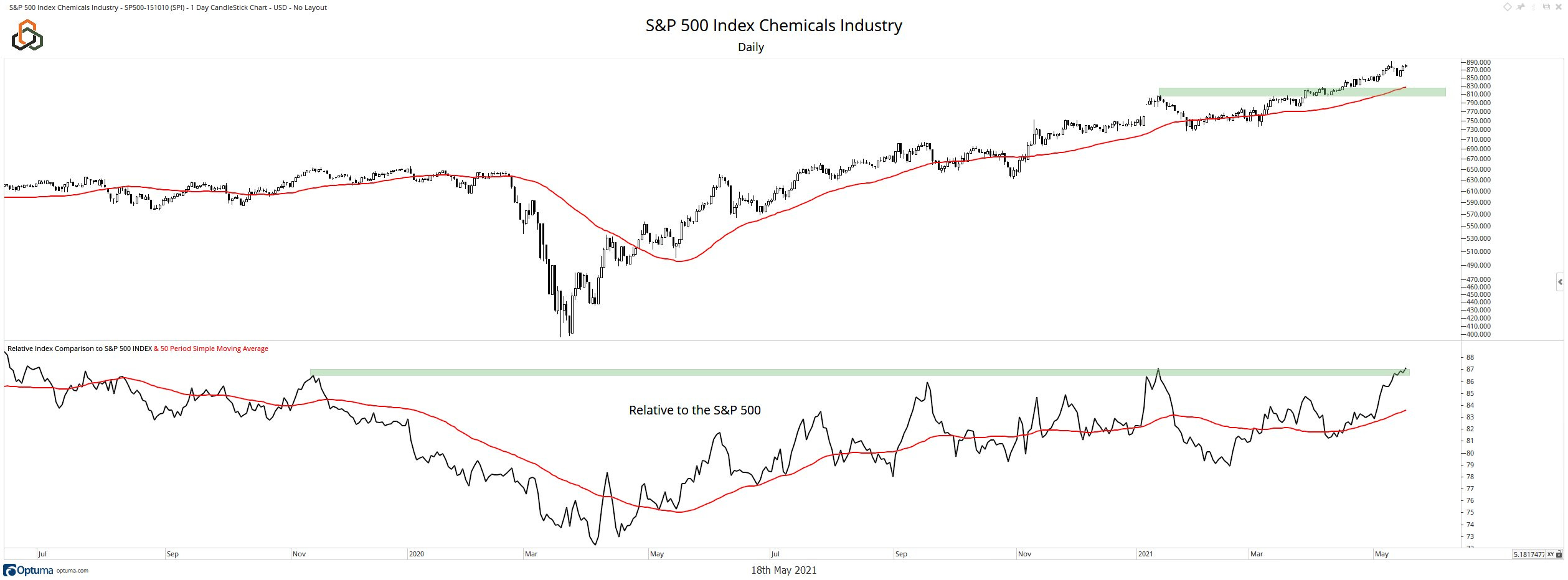

Quick technical analysis & commentary on the S&P 500 Index Chemicals Industry, which is currently at/near ATH’s. Chart was provided by Dan Russo on Twitter (@DanRusso_CMT) at the market open on 5/18.

The red band is the 50 day moving average & the chart on the bottom is the price of the Chemicals index relative to the overall S&P 500. The 50 MA is often viewed as a way to measure momentum as well as a dynamic support/resistance level for price to bounce on (notice how price tends to rebound when it retests the 50 MA since 2020). One thing that I want to highlight is how the Chemicals index has performed extremely well, with a YTD return of +18.6%. This is significant outperformance relative to the Dow (+12%), S&P 500 (+10.8%), and Nasdaq (+3.8%).

Structurally, the index is at a key resistance level relative to the S&P 500, which has been rejected nearly three times (Nov. 2019, September 2020, and January 2021). My best estimate is that the Chemicals index is going to have a massive breakout relative to the S&P 500 and maintain strong outperformance. Particularly in light of chemical shortages, such as chlorine, and supply chain disruptions for raw materials used in plastic production. Chemical manufacturers are set to benefit from these factors, especially as commodity inflation has been a strong market theme in 2021.

Ideas: $DOW $DD $LYB $LIN

Cryptocurrency:

MicroStrategy ($MSTR), an enterprise software company, made headlines last year when they were the first publicly traded company in the U.S. to convert their cash position & store Bitcoin on their balance sheet. CEO & founder, Michael Saylor, has become one of the most public proponents of Bitcoin since his announcement, meanwhile facing sharp criticism of the decision. Since MicroStrategy made the announcement in August 2020, in which it purchased 21,454 Bitcoins, the company has continued to purchase more Bitcoin & even issued several rounds of convertible debt offerings (raising more than $1.5Bn) to buy more.

This morning, Michael Saylor posted an announcement that “MicroStrategy purchased an additional 229 bitcoins for $10.0 million in cash at an average price of ~$43,663 per Bitcoin”. The $10M purchase was done on May 18, 2021. Per the SEC filing, clarified that the company’s balance sheet now had 92,079 Bitcoin, purchased for an aggregate price of $2.251Bn at “an average price of ~$24,450” per BTC. I think this will go down as one of the highest conviction decisions in the history of corporate America. It’s worth noting that the value of $MSTR’s Bitcoin position is $3.97Bn at a current price of $43,133/BTC. With a holding size of 92,079 BTC, they currently hold less than 0.5% of the total circulating supply of 18,713,313 (and only 21M will ever exist). With approximately 9.746M outstanding shares of MicroStrategy, an owner of 1 share of $MSTR, currently worth $489/share, will indirectly own 0.0094 BTC = $407 at a market price of $43,133.

Considering that MicroStrategy was trading at $123.62/share before announcing their first Bitcoin purchase on 8/11/2020, which equates to a market cap of roughly $1.2Bn, we could conclude that their enterprise software business alone is worth $123/share. Based on the analysis above, it seems that the market is either:

Pricing in a significantly lower price of Bitcoin of roughly $38,900/BTC ($489 - $123 = $366. $366/0.0094 = $38,900), while maintaining the same $123/share valuation of the enterprise software business.

Undervaluing the value of the enterprise software business by at least $41/share ($489 - $407 = $82. $123 - $82 = $41), while maintaining the current $43,133 price of Bitcoin.

Until tomorrow,

Caleb Franzen