Investors,

You’re probably surprised to see this newsletter arrive in your inbox this morning, rather than the typical Saturday morning delivery. I’ll be on vacation this weekend in New York, so I won’t be publishing additional research this weekend. Premium members can expect to receive “Portfolio Strategy Pt. #4 — What I’m Buying & Why” this upcoming Wednesday.

September 2022 CPI Data:

Considering that I’ll be away from my desk & laptop this weekend, I thought it was necessary to provide my immediate reaction to the CPI data, the market reaction, and ongoing market dynamics. On Wednesday, I published a preview of my expectations for the September CPI data and had also expressed my 95% confidence interval that the YoY change in headline CPI would be +8.2% to +8.5%. While this was my general assessment, I also provided the following context:

With the long-awaited September results, the data showed that the headline CPI increased at a pace of +8.2% YoY (vs. +8.3% in August 2022 and estimates of +8.1%). On a month-over-month basis, the CPI increased by +0.4% (vs. +0.1% in August 2022 and estimates of +0.3%).

While headline decelerated, the month-over-month rate of change actually accelerated in September! In a vacuum, there’s nothing to celebrate about inflation of +8.2% YoY; however, we operate in a market that’s able to contextualize the current results vs. former data.

I’ve continued to express my belief that headline inflation will decelerate, based primarily on declining energy & oil prices. In mid-August, after receiving the July CPI data (which fell from +9.1% YoY to +8.5% YoY), I shared the following:

“Therefore, while we can be encouraged about the deceleration in headline inflation, it’s vital to contextualize it against the acceleration in these various other measures. What this tells me is that most, if not all, of the decline in consumer prices was driven by lower energy & oil prices. While this is an encouraging first step, we’re not out of the woods yet. From my perspective, it’s possible that we’ve seen a peak in headline inflation while these alternative measures (core, median, trimmed mean, and sticky-price) continue to increase.”

Over the past two CPI readings for August & September, this is exactly what has manifested: headline CPI is declining while underlying metrics of inflation continue to accelerate.

We must remember the impact of base effects when calculating the YoY rate of change and trying to extrapolate a trend based on the monthly evolution of the data! For example, the YoY change in the CPI has decreased for the past three months since the June “peak” of +9.1%:

July 2022 YoY: +8.5%

August 2022 YoY: +8.3%

September 2022 YoY: +8.2%

However, look at the month-over-month trends for each of these months:

July 2022 MoM: ±0%

August 2022 MoM: +0.1%

September 2022 MoM: +0.4%

Therefore, while the headline CPI is decelerating on a YoY basis over the past few months, it’s actually accelerating on a MoM basis over that same period. It’s also important to contextualize the headline CPI vs. these other alternative methods of measuring underlying consumer price inflation. Specifically, I want to highlight the dynamics that are occurring for core CPI, median CPI, and trimmed-mean CPI:

Core CPI increased from +6.3% YoY in August to +6.6% in September. This further strengthens my argument that the deceleration of inflation is being entirely driven by declining energy & crude oil prices. By excluding food & energy prices in this calculation, the purpose of core CPI is to reduce volatility in monthly inflation results. It certainly isn’t most important thing to monitor, but it helps to frame inflation dynamics in a more consistent light.

Median CPI increased from +6.7% YoY in August to +7.0% in September, confirming that the median inflation components are accelerating.

Trimmed-mean CPI increased from +7.2% YoY in August to +7.3% in September.

Each of these three measures of inflation accelerated from July → August and from August → September. On net, this data offers a unique & consistent message that inflation has not peaked and that all of the disinflationary dynamics we’ve seen over the past several months have been caused by lower energy & commodity prices. This is the same message I’ve been sharing since the July data was released in August. Consider the following development that’s taken place since the June CPI data: In June, the Gasoline component of the CPI was up +11.2% MoM. For the past three months, Gasoline has fallen rapidly:

July: -7.7% MoM

August: -10.6% MoM

September: -4.9% MoM

Therefore, since the peak in June, the Gasoline component has fallen -23.2%!

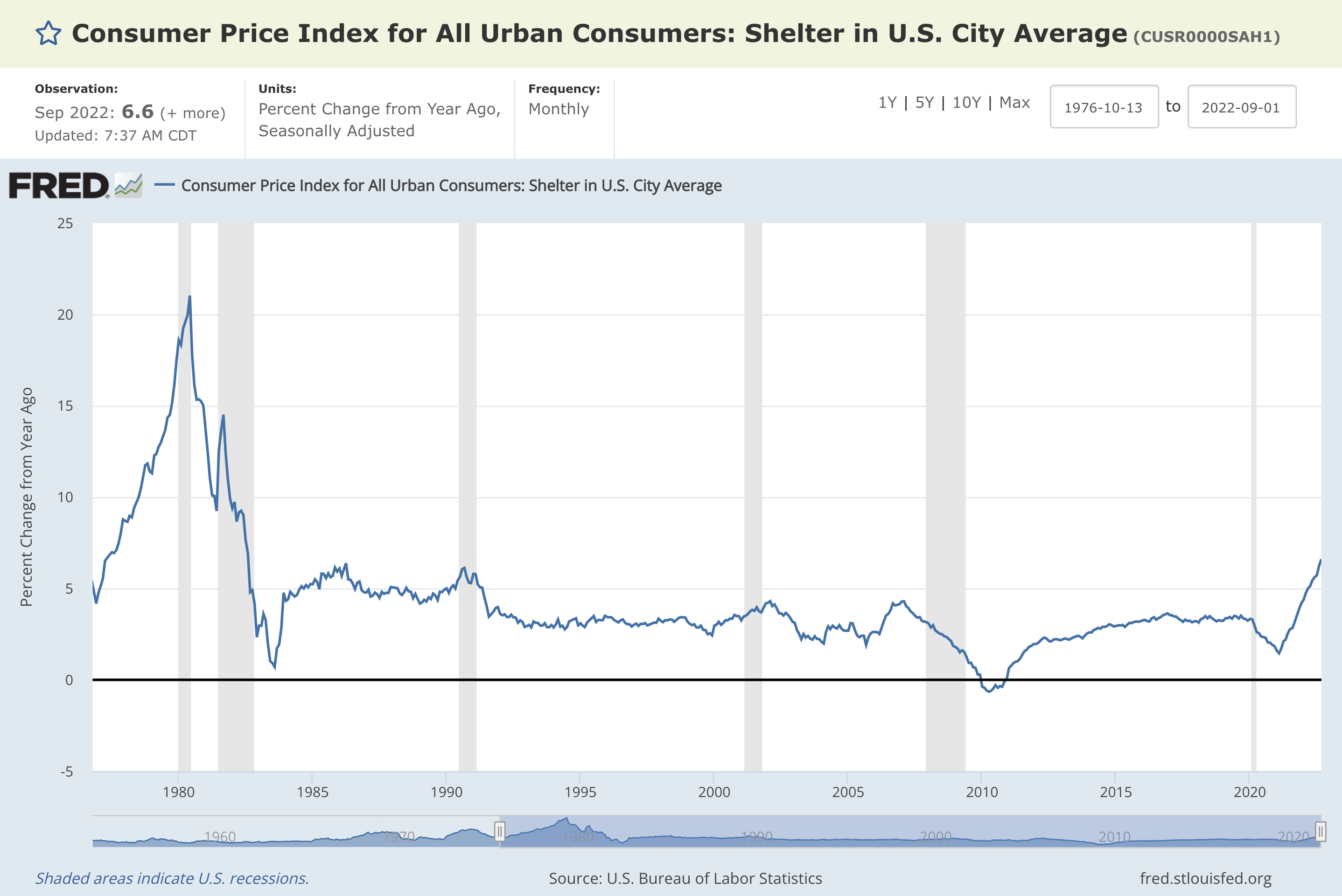

Meanwhile food-related costs & shelter continue to reach historic levels. For example, the overall Food component (which includes “food at home” & “food away from home”) accelerated at a pace of +11.24% YoY in September, down slightly from +11.36% in August. These two results have been the highest readings since April 1979. Turning our attention to the Shelter component, it increased from +6.25% YoY in August to +6.6% in September. This is the highest reading since August 1982.

I expect the Shelter component to remain historically elevated and likely trend higher for the next 6 months or more. Considering that Shelter, measured via an abstract figment referred to as owner’s equivalent rent (OER), lags the broader housing & rental market by roughly 12 months, I think that Shelter-based inflation will likely remain elevated through Q1 2023 and into Q2. It’s important to note that Shelter comprises roughly 1/3rd of the total CPI calculation, so this component will be critical for the overall evolution of inflation & core inflation in particular.

Monetary Policy Implications:

On the aggregate, the September CPI data was a disappointment despite the fact that headline CPI decelerated. This entire inflation/Federal Reserve situation is analogous to the following:

We’re in a car going 120mph on the freeway, but we’re sitting in the backseat. The driver (the Fed) tells us that “there’s a cop ahead, so we need to slow down to 65mph”. As they begin to slow down, they slam on the brakes and immediately reduce our speed to 90mph, with another 200 yards until we reach the police officer. Despite massively decreasing our speed, our velocity is still positive. The driver has to pump the brakes even harder in order to reach 65mph.

Based on this metaphor, it’s no surprise why market expectations immediately reached a consensus that the Federal Reserve will once again raise the federal funds rate by +0.75% on November 2nd. As such, this is likely going to be the fourth consecutive +75bp rate hike and yet the market is also placing a 64% chance that they raise by another +75bps in the December meeting!

CME futures immediately repriced following the September CPI data, decisively in favor of a +0.75% rate hike in November:

Market Reaction & Portfolio Outlook:

In immediate response to the CPI data and the implications for monetary policy, risk assets plummeted in the futures market. However, this was relatively short-lived once the traditional financial markets opened. S&P 500 futures had a violent decline & recovery when analyzed with 1-minute candles. From the market lows at 9:33am ET to the market close at 4pm ET, the S&P 500 gained +5.17%:

This was a remarkable momentum thrust, with consistent buying pressure throughout the session. It’s difficult for me to tell the market that it’s wrong, but I’m trying to get a clear understanding for the massive increase in demand. Ironically, I don’t think that investors are “celebrating” the inflation data; although I do believe that the inflation-induced selloff provided the opportunity for large investment firms to step in on discount. In fact, I think the entire rally largely being caused by extremely negative market sentiment & positioning. With such a significant consensus that the market would react poorly to the inflation data (it did), early buying pressure catalyzed more buying pressure & FOMO sentiment in the late morning.

Interestingly, I wrote this analysis on Thursday evening, but I’m scrolling Twitter on Friday morning & I see the following post from Liz Ann Sonders, the Chief Investment Strategist at Charles Schwab:

This seems to add more credence to my theory that positioning & extreme negative sentiment prompted a stampede of buying pressure, potentially catalyzed by institutional algorithms.

Objectively, I can’t say with any degree of certainty whether or not this single-day rally will persist, or for how long it will persist. Do I have my doubts? Absolutely. Do I have hope. Absolutely. While I still see further downside in stocks, bonds, crypto, and real estate, I think there are unequivocal opportunities to increase long-term market risk by adding to core investment positions. I want to be very clear about this:

It’s okay to believe that asset prices are going to fall in the short-term, while simultaneously increasing exposure to those same assets.

The majority of my investment purchases over the past few months have been with 0.5% to 1.0% of available capital, meaning that I have the ability to purchase assets 100-200 times before running out of my current levels of dry powder. I have been (and will continue to be) patient in terms of elongating my DCA runway. While I don’t know for certain where the market will go in the next week, month, quarter, or year, I do know that I want to increase my long-term exposure to core portfolio holdings.

This market selloff has provided an amazing opportunity for investors who are willing to stomach short-term risk and patiently increase their long-term risk! While these investments may take 24+ months to yield positive returns, this is the risk that comes with the territory. We’ve been spoiled for the past decade with strong market returns, which have therefore distorted expectations of investors. My advice to all investors:

Stay patient, zoom out, and act in accordance with your own risk tolerance, time preferences, financial obligations, income, and goals. If you feel that you are able to stomach short-term volatility, buy assets that you have a deep understanding of and can feel confident in your long-term conviction. There’s no shame in waiting to allocate more capital into the market — we also need to preserve our mental/emotional capital. We’ll be alright.

I can assure you that I’m putting my money where my mouth is, patiently increasing my exposure to these 15-core equity positions and continuing to buy Bitcoin in the $18,000-$22,000 range.

Best,

Caleb Franzen

DISCLAIMER:

My investment thesis, risk appetite, and time frames are strictly my own and are significantly different than that of my readership. As such, the investments & stocks covered in this publication are not to be considered investment advice and should be regarded as information only. I encourage everyone to conduct their own due diligence, understand the risks associated with any information that is reviewed, and to recognize that my investment approach is not necessarily suitable for your specific portfolio & investing needs. Please consult a registered & licensed financial advisor for any topics related to your portfolio, exercise strong risk controls, and understand that I have no responsibility for any gains or losses incurred in your portfolio.

Remember when analysts expected the feds to hike 0.25bps at most 3 time this year. Later the narrative changed to "the feds can't hike past 3%, they are going to wreck the government"

But here we, ready for the 4th consecutive 0.75bps, and FFR towards 4% — and nothing has broken yet.

Moral of the story; never say never.

Back in January, if you told anyone how this hiking cycle would play out, they'd expect the S&P to be below $3,000. But here we are hanging around $3,500. Equities showing relative strength. This is impressive.