Investors,

The Dow Jones Industrial Average, S&P 500, and Nasdaq-100 closed the Friday session at new daily, weekly, and monthly YTD lows. Plagued by continued pressure from global central bank tightening, strong rhetoric from various Federal Reserve officials, persistent inflation dynamics, and a historically strong U.S. Dollar, each of the major financial asset classes can’t catch their breath.

The intensity of this pressure is forcing many investors to simply walk away from the table, analogous to a blackjack player forced to cut their losses, leave the casino, and lick their wounds. In a way, this market cleansing dynamic is necessary for the long-term health of financial markets; however, there appears to be no end in sight. As of Friday’s close, these are the YTD returns for each of the major indexes:

Dow Jones $DJX: -20.96%

S&P 500 $SPX: -24.8%

Nasdaq-100 $NDX: -32.75%

Russell 2000 $RUT: -25.8%

With the S&P 500 peaking on the second trading day of 2022, the ATH’s are officially 269 days behind us. According to the following data from Charlie Bilello, this is the longest bear market since the Great Recession:

According to these implications, the average non-recessionary bear market going back to 1929 lasts for 12 months, while the average bear market that occurs with a recession lasts for a total of 16 months. While averages merely allow us to contextualize historic market dynamics, this data indicates that we should expect more tumultuous market conditions going forward.

In the remainder of this analysis, I’ll share the most interesting data points, charts, and market dynamics that I saw this week. I’m hopeful that these reports don’t merely share where we are and how we got here, but where we might be headed. For the past several months, the macro portion of these reports have been significantly longer than the stock market & Bitcoin sections, for the simple reason that macro is dominating the market narrative. As such, I continue to believe that macro developments will continue to drive broader market dynamics, largely influenced by inflation, monetary policy, and yields.

While these free reports will continue to highlight key developments I’m seeing in the stock & crypto markets, my Premium Market Analysis is intended to provide data-driven insights for how I’m viewing financial markets and to explain how new data fits within my investment thesis.

If you’re interested in reading these weekly deep-dives, in addition to other exclusive research, I’d encourage you to consider becoming a premium member!

Macroeconomics:

Interestingly enough, I felt like the most important economic dynamics came from Europe this past week. Notably, UK bond market dynamics, the subsequent reaction by the Bank of England (BoE), and EU inflation were at the top of the list. In addition to these topics, I want to follow up on prior analysis that I’ve shared about mortgage & the U.S. housing market.

As it pertains to dynamics across the Atlantic, the Bank of England was seemingly forced to intervene with monetary stimulus in order to stopgap the bloodbath in the UK bond market. Allegedly, UK pension funds were on the verge of insolvency due to their allocation in UK government bonds, which were collapsing at a historic pace. In addition, the British Pound was also collapsing at a historic pace, indicating that there was a severe shortage of demand for British Pounds today (GBP) and future British Pounds (UK bonds).

Quite simply, the UK bond market was failing. While I think the term “failing” gets thrown around too often in the world of finance, it’s actually appropriate in this circumstance. A failing market occurs when buyers and sellers simply cannot agree on an equilibrium price, or when there aren’t any buyers at any given price. According to data from Robin Brooks, liquidity (the measure of how easily an asset can be converted into cash) was abysmal for UK bonds. In the chart below, a rising trend is indicative of falling liquidity:

This highlights the difficultly that sellers were faced with, unable to successfully find a buyer for their UK bonds and essentially becoming trapped in holding the asset. Shortly before 9pm ET on September 25th, the GBP was collapsing relative to the dollar & reached an all-time low in terms of the GBP/USD exchange rate:

While the Pound has attempted to recover from those lows on 9/25, the direction of the trend is crystal clear: GBP is bleeding relative to USD.

Said differently, capital is flooding into the dollar. Global capital allocators are constantly forced to make a critical decision: where to allocate money today. With an immense amount of confusion about the direction of monetary policy in the UK, deep recession fears throughout Europe, and political risks in South America & Asia, global capital allocators are increasing their demand for U.S. dollars. In turn, this has created the strongest period for the dollar relative to a basket of global currencies in 20+ years.

While the BoE has been tightening monetary policy quite aggressively over recent months, the collapse of UK government bonds essentially forced them to step in as the buyer of last resort. The BoE announced that they’d be purchasing up to £65Bn worth of UK bond with a maturity longer than 20 years. In other words, they approved £65Bn worth of monetary stimulus. However, they’re also raising interest rates at the same time, which is equivalent to monetary tightening.

This is monetary confusion at its finest, equivalent to pressing the gas & brake pedals simultaneously in a car. Again, this highlights why the dollar continues to see inflows and is trading at 20+ year highs.

Admittedly, I’m not familiar with UK economics, monetary policy, or politics. I can’t say how this story will unfold over the coming months/years, but it’s clear to see that the BoE is becoming the first domino of the developed nations to swivel. It might fall or it might manage to stay upright, but it’s far too early for me to call it. All we know right now is that there are cracks in the system and that bureaucrats will try to fix it.

While the BoE’s actions appear to be a temporary solution, global investors are reading between the lines and viewing this development as a foreshadowing of a Federal Reserve pivot. I believe that this is a misguided interpretation, despite the historically poor performance of U.S. Treasuries in 2022. Quite simply, the U.S. bond market isn’t failing and the Fed has continued to express their resolve in combatting inflation despite the economic costs. The Federal Reserve is blatantly trying to create economic costs by producing an inverse wealth effect, making the cost of capital more expensive, disincentivizing debt-based consumption, and deteriorating the labor market in order to reduce aggregate demand. They have clearly expressed this goal and I think that a pivot will come from two scenarios only:

Inflation returns to their target, or to a level that is decisively trending towards their 2% target.

Financial collapse/crisis.

We better hope it’s the former.

Returning to Europe, I want to briefly highlight inflation dynamics across the Eurozone. The German CPI data was released for September 2022, reflecting a +10.0% increase YoY (vs. +7.9% YoY in August 2022). This is the highest level of inflation in Germany since WWII, which history buffs will remember was one of the key components that Hitler used to rile up the German spirit. On the aggregate, EU flash CPI for September came in at +10.0% YoY, the highest levels of inflation since the union was formed:

It’s clear to see that global inflation dynamics in developed economies continues to increase. While Europe is dealing with their own set of problems and the ECB has a different mandate than the Federal Reserve, we must acknowledge that historic inflation is a global phenomenon.

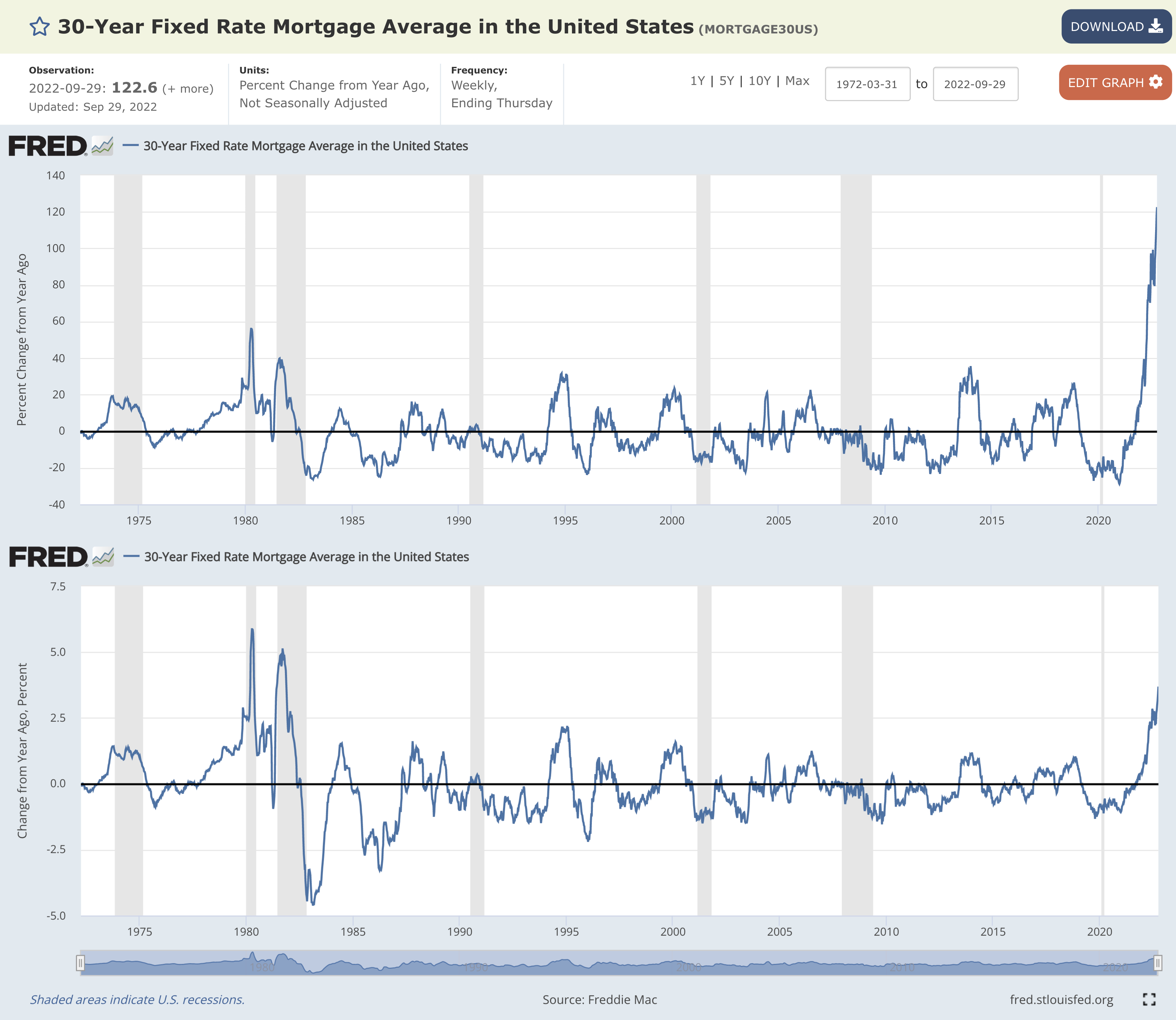

Returning back to the U.S., I’m seeing more analysts focused on the YoY % change in 30-year mortgage rates, which I’ve been trying to spread awareness about since mid-August. I’m glad to see this getting more attention, so I wanted to provide the updated view as of the most recent data.

There are two important ways to contextualize the rapid rise in mortgage rates:

Top: YoY percent change = +122.6%

Bottom: YoY nominal change = +369 basis points

For as long as we have data in the U.S., we’ve never seen the average 30-year fixed mortgage rate double over a 12-month period. The current pace is significantly faster than “just double”, measured at +122.6% YoY. Considering that the starting point is from historically low rates, it’s important to contextualize the increase by looking at the YoY nominal point increase. This measure, currently reflected as +3.69%, is the highest since the great inflation of the early-1980’s. In both contextualizations, mortgage rates are accelerating at an unsustainable pace.

Actually, let me rephrase that…

Mortgages can continue to increase going forward, though perhaps at a slower rate of change. The “unsustainable” aspect is home prices, which have remained elevated & resilient to significant downward pressure so far. The S&P Case-Shiller National Home Price Index was updated for the month of July 2022, reflecting a month-over-month decline of -0.33%. That’s a fairly negligible decline, particularly when we consider that the National Index is up +15.8% on a YoY basis!

Remember, housing affordability & mortgage debt-servicing is a function of:

The interest payment, derived from the mortgage rate.

The principal payment, derived from the price of the home & down payment.

With interest rates accelerating at such a historic pace and home prices generally remaining at/near all-time highs, it’s clear to see how housing affordability is extremely low. Considering that interest rates aren’t expected to fall going forward, the only way for affordability to improve is for home prices to fall.

My position on this topic remains the same: I expect both supply & demand in the housing market to remain extremely muted over the coming months, and likely through the first half of 2023, during which time I expect to see home prices decelerate dramatically and flip negative on a YoY basis.

Stock Market:

As mentioned at the intro of this report, equity markets are in a bad place right now. Considering that you probably don’t need me to tell you that, I wanted to share an interesting perspective about the severity of this current drawdown and what it might mean going forward.

Specifically, I want to focus on the S&P 500 and the 48-month moving averages. While 48 months might feel like an arbitrary number, it allows us to analyze the 4-year trend of the market and diagnose where price is relative to the 4-year average. If we analyze the S&P 500 since the mid-1940’s, we can identify an interesting trend!

The S&P 500 experiences classic bull markets (periods of exuberance where price is significantly higher than the 4-year average for an extended time), followed by a mean reversion back to the 4-year trend. Historically, price has rebounded in a near-perfect fashion on the 4-year average; however, we have experience multiple periods where the Index remains below the 4-year trend for multiple months at a time.

Here’s the S&P 500, shown using logarithmic scale in order to analyze the price trends of the past & present:

I’ve added the 48-month exponential moving average (EMA) in green & the simple moving average (SMA) in red in order to create a dynamic range of the average. While it’s difficult to see on this chart above, the S&P 500 officially closed the month of September below the 48-month EMA, but has yet to cross below the SMA. It’s possible that the S&P 500 has completed its mean reversion process and will soon begin to form a rounding bottom, as it has throughout history. Conversely, deep bear markets have been identified as periods where the Index sustainably remains below the 48-month MA cloud for 6+ months. During this downtrends, identified in orange circles, we enter the most painful phase of the bear market.

Quite literally, we’re at an extreme inflection point that could have severe repercussions for market dynamics going forward.

However, I don’t want this potential warning to be received as doom & gloom. In fact, let’s consider the periods where the Index fell below the 48-month MA cloud and recognize that the best time to be a long-term buyer was during these periods. Should we actually stay below this range over the coming months, I’ll view it as a generational buying opportunity while conceding that more short-term pain is to be expected. Historically, these have been extremely difficult times to increase exposure to equities, but the long-term rewards are very attractive. Maintaining composure during these periods is difficult, but necessary & I’d encourage investors to have a list of high-conviction assets that they are interested in buying for their long-term portfolio. Here’s what I’m buying:

Bitcoin:

While equity markets have closed at new YTD lows, both Bitcoin & Ethereum have held up quite well on a relative basis. At the time of writing, they are respectively trading at $19,410 and $1,330 and have yet to fall below the June 2022 lows.

Considering the significance of the 48-month moving averages that we highlighted above for the S&P 500, I thought it would be worthwhile to share the same analysis for Bitcoin:

While Bitcoin has a much shorter history than the S&P 500, we can see that the 48-month MA cloud is also an extremely important mean reversion level. Interestingly, this dynamic support range is acting as resistance after falling below it in June, which I’ve been warning about as a negative development. Based on this analysis alone, I’ve forecasted that the price of Bitcoin could experience further downside to the teal range, formed via the 2018 high (December close) and the 2019 high (June close). This gives a reasonable target of roughly $10,500-$13,900/BTC. Should more downside continue, this could act as a viable support range, even for a short-term period.

Many analysts on Twitter are highlighting the relative strength of Bitcoin vs. the S&P 500 that occurred this past week, alluding to the idea that this trend will continue to persist. Unfortunately, I don’t share their confidence, though I acknowledge the possibility that they are correct.

Why am I more cautious to celebrate? While Bitcoin is perceived to be more risky than stocks, and riskier assets typically bottom first at the trenches of a bear market, we’ve seen an interesting dynamic across financial markets over the several weeks.

Consider the following:

20+ Year U.S. Treasuries created new YTD lows on September 6th.

The Dow Jones, “riskier” than Treasuries, created new YTD lows on Sept. 23rd.

The S&P 500, “riskier” than the Dow, created new YTD lows on Sept. 27th.

The Nasdaq-100, “riskier” than the S&P, created new YTD lows on Sept. 30th.

The Russell 2000, “riskier” than the Nasdaq, has yet to create new YTD lows.

Strangely, market dynamics are showing us that the “less risky” assets are structurally weaker than the “riskier” assets and leading the way lower. With Bitcoin & crypto widely accepted as the riskiest asset class, I think it’s reasonable to expect that broader financial market pressure will produce new YTD lows for Bitcoin in the coming weeks/months.

I don’t have a crystal ball, but I’ll continue to observe the data & market dynamics in an objective fashion and provide key insights that I think you should be aware of. With that, I look forward to sharing more stock & crypto analysis tomorrow with the Premium Team!

Best,

Caleb Franzen

DISCLAIMER:

My investment thesis, risk appetite, and time frames are strictly my own and are significantly different than that of my readership. As such, the investments & stocks covered in this publication are not to be considered investment advice and should be regarded as information only. I encourage everyone to conduct their own due diligence, understand the risks associated with any information that is reviewed, and to recognize that my investment approach is not necessarily suitable for your specific portfolio & investing needs. Please consult a registered & licensed financial advisor for any topics related to your portfolio, exercise strong risk controls, and understand that I have no responsibility for any gains or losses incurred in your portfolio.