Edition #21 - 6.11.2021

Inflation, Inflation, Oh & More Inflation!

Economy:

In my newsletter dated May 24, 2021, one of the topics of discussion was the used car market, notably the rapid ascension of prices in that market, and then gave some general comments on inflation. In that section I wrote the following:

I believe the Fed has done a sufficient job of downplaying how high inflation can rise over the next 24 months through their rhetoric & consistent reassurances that they’ll be able to reel in consumer prices if/when they need to. From my perspective, I wouldn’t be surprised if we see the 12-month CPI inflation numbers between +6% and +10% at some point in 2021. Even in this forecast, I think it’s far more reasonable that the CPI inflation remains below +7%, but I’m certainly open to the idea that we move higher than that.

Today, the long-awaited CPI data for May 2021 was released, which can be viewed in its entirety from the BLS. The result was a +0.6% month-over-month increase in the CPI, inclusive of all items, and a +5.0% increase year-over-year. Meanwhile, the consensus estimate was at +0.5% and +4.7%, respectively. Once again, this report was an upside surprise relative to estimates, but it’s unclear whether it’s a sign of good or bad news. Depending on which type of economist you ask, you’ll get a different answer. For right or for wrong, it is what it is.

From my perspective, we continue to track towards my window of +6% to +10% in 2021; however, I’m starting to recognize that this is developing faster than I initially anticipated. As such, the +7% or less figure I gave as a “more reasonable” account of my expectations might be underestimating the rising momentum in consumer prices.

Many economists, including members of the Federal Reserve, also look at the core CPI data, which simply excludes food & energy prices (which are explained to be more volatile in nature, thus giving a less consistent comparison for inflation). For the month of may, the core CPI inflation was +3.8% on a YoY basis. Here is a graph tracking the YoY core CPI inflation figures dating back to 1991. As we can see below, this is the highest the core CPI inflation has been since 1993.

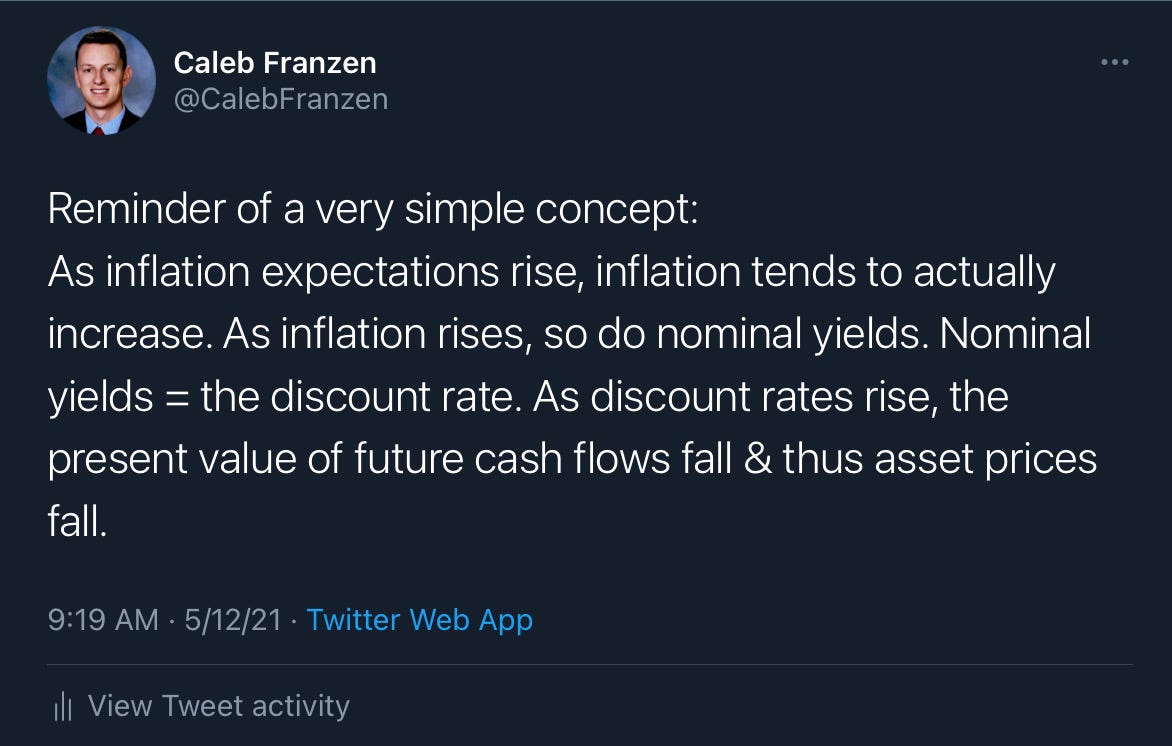

While the data release in and of itself is important, a case can be made that the market responds is just as, if not more, important. At the beginning of the year, as inflationary pressures started to gain early signs of momentum, nominal yields on government Treasuries rose in accordance. If inflation is a symptom of an expanding economy, as modern economists believe, nominal yields were rising in order to price in the expectation of higher economic growth! Additionally, to offset the impact that inflation has on fixed-income securities, bond investors weren’t willing to accept the previously lower rates, began to sell their Treasury securities, and bond yields rose in accordance to these market dynamics. As nominal yields rose from January through March, growth & technology stocks were hit the hardest, as asset prices typically have an inverse relationship with yields. To highlight this point, here are two tweets that I posted discussing how inflation & nominal rates can impact asset prices, particularly for companies with high growth expectations:

The interesting thing to note however, is that despite the strong rise in yesterday’s CPI inflation release, nominal yields actually declined dramatically throughout the trading session on Thursday. As bond yields fell, stocks climbed higher and were led by the Nasdaq-100 at +0.78% for the day. Meanwhile, the Dow Jones was +0.06%, S&P 500 +0.47%, and the Russell 2000 was actually negative at -0.68%. In any event, the divergence between inflation & yields created a lot of confusion amongst economists and financial media commentators, but can actually be explained by one simple factor: the Federal Reserve.

Throughout this newsletter, I have highlighted the rhetoric of the Fed & the various officials within the institution who have continued to pound the table on a few key things. The first is that they want inflation to to remain moderately above 2% for some time. In order to achieve a longer-run average of 2%, in which the U.S. has remained well-below 2% for the majority of the time after the Great Recession, the Fed is willing to let inflation run hotter than normal. The second factor is that the Fed’s rhetoric has provided substantial reassurance to the market that any spike in inflation is transitory, and the Fed has the ability to curb inflationary pressures. With the market convinced that the higher inflation is coming and that Fed will be able to rein in inflation, it appears that the market was actually pricing in more than a +5.0% YoY CPI!

I think that there are a lot of concerns around inflation, with fears that hyperinflation or stagflation are just around the corner. Now that we’ve started to see hints of that inflation since the beginning of 2021, those fears have been rising. However, there is still no evidence of either of those two outcomes being the probabilistic outcomes. My mantra/prediction has continued to be that rates will be lower for longer than the market is currently pricing in. Everyone believes rates must rise. That’s the consensus trade. That was also the case in 2011 and 2012, but several rounds of QE passed as well as operation twist and new FOMC strategies kept rates lower for longer than anyone anticipated at the onset of the recovery.

With that said, I do believe the Federal Reserve will raise rates at some point over the next 18-24 months, but I’m not confident that they’ll be able to raise them as high as they did during the last hiking cycle ending in 2018. I also think they’ll take a more slow, steady, and gradual approach to their taper & rate hike process. At the same time, just as the Fed is flexible to incoming data & acts in accordance to new data, as will I. If I’m wrong about inflation, and we actually see double-digit CPI growth for a sustained period, the Fed will need to raise rates dramatically to combat it. We’ll just have to see how the data continues to develop.

One last thought: inflation is typically bad for bonds, as the inflation rate eats away at the coupon payments of the bond and dissolves the value of future dollars. Over the course of the last few weeks, we’ve seen a significant decline in Treasury bond yields for 5, 10, and 30-year Treasuries, indicating that buyers are finally stepping in with force. Is it possible that the bond market has started to price in a peak in the inflation rate? As I said, it appears that the market was seemingly expecting higher CPI inflation data for May 2021 and was thus able to shrug off the +5.0% result. I’ll continue to watch the bond market with more acute detail, so don’t be surprised if I start posting more technical analysis and commentary on Treasuries going forward (hint hint, I’ve already been doing it on Twitter).

I know that rising consumer prices is a dense & dry topic to talk about, so I’m happy to dedicate this newsletter solely to this topic.

Talk soon,

Caleb Franzen