Investors,

To celebrate the 200th edition of Cubic Analytics, I’m making this premium research report available to all subscribers! If you’re currently a free subscriber, these weekly reports are typically exclusive for paid members and are designed to provide original insights about the stock & crypto markets that I don’t share on other platforms. For $10/month, premium members get full access to my views, ideas, and expectations about market conditions via these deep-dive reports.

I hope that this latest report highlights the additional value of my research and illustrates why premium memberships are growing at a rapid pace. The premium team has hundreds of investors who have subscribed and we’d love to have you join:

In a late-June publication, I expressed my belief that financial markets were trading at an inflection point, potentially signaling where inflation might go next. Since then, I’ve been laser-focused on how risk appetite has been evolving across the market. I’ve contextualized risk appetite by analyzing key relationships on an intra & inter-market basis to illustrate how investors are increasing their demand for risk assets, regardless of the asset class.

In today’s report, I’ll share new findings to confirm this trend and analyze under-the-hood metrics for the S&P 500. First, I want to share a pivotal new discovery that I made about Apple Inc. AAPL 0.00%↑ and what it implies for the broader market. In my opinion, this is the most important study that I’ve produced since my late-July analysis about the Nasdaq-100:

Let’s dive right in…

Apple Inc. ($AAPL) Study:

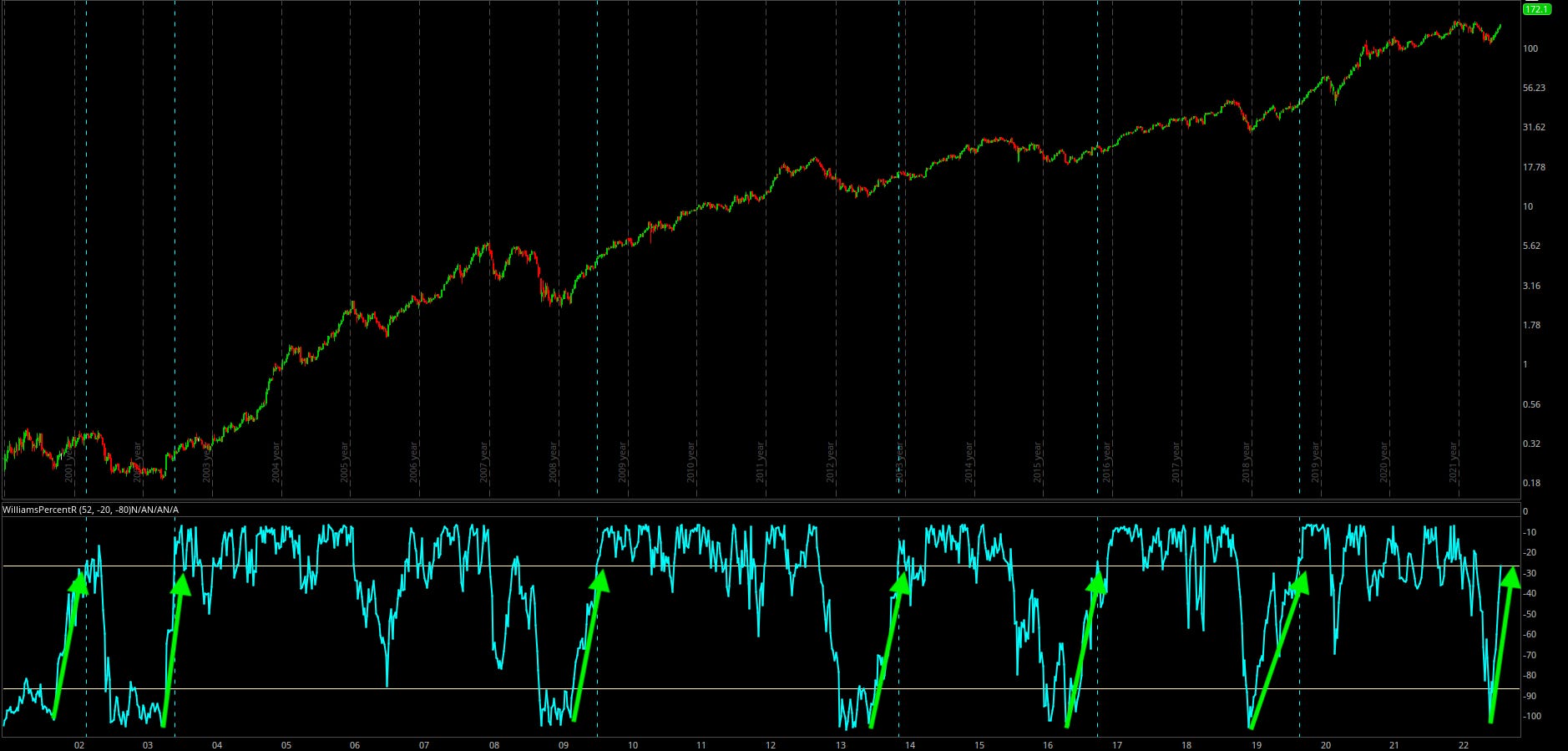

Apple has been on a massive run over the past several weeks, currently up +33% from the YTD lows. This made me question: “Have we seen AAPL make similar momentum thrusts of this magnitude in the past, from a statistical perspective?”

Using the 52-week Williams%R Oscillator (1-year trend analysis), I noticed that Apple was making a momentum thrust from below the lower-bound (oversold) and peaking above the upper-bound (overbought). This full oscillation has only happened 6 other times since the year 2000!

At first glance, this doesn’t appear to be an excellent market timing strategy; however, it certainly appears to increase the likelihood of riding a wave of momentum higher. Simply by glancing at the chart above, we can see the significance of this momentum thrust signal for AAPL, but let’s dive deeper into the six prior signals:

Aside from the signal in March 2002, each signal flashed after the lows were in. Even still, an investor who bought AAPL in March 2002 had a phenomenal 5-year return of +592% (6.9x their investment) despite the choppy market environment they had to endure over the short & medium-term. With an average annual return of +36.6%, this data is extremely hard to ignore.

In order to produce extremely strong long-term return profiles, investors had to sit through some turbulence and endure brief periods of pain.

Could this time be different? Absolutely. As I always say, we cannot analyze statistics in a vacuum and must always contextualize this data against the macroeconomic environment. However, an investor in 2002, 2009, and 2019 had very legitimate reasons about the macroeconomic environment to avoid buying stocks. They had every reason to stay on the sidelines and believe that market conditions were going to get worse, very similar to the macro environment that we’re in right now. Nonetheless, markets continued to produce new highs over the medium to long-run.

I expect that will continue to be the case for this current signal. Could there be short-term pain ahead? Yes. However, that short-term pain will continue to create opportunities for long-term investors who are able to maintain their composure and stick to their convictions.

Risk Appetite & Relative Performance:

1. S&P 500 SPY 0.00%↑ vs. Consumer Staples XLP 0.00%↑ (SPY/XLP):

Comparing the broader stock market vs. the defensive consumer staples sector is a beautiful way to visualize risk appetite in the equity market. Here’s how I approach this ratio:

Fearful market environments are illustrated by SPY/XLP ↓

Happy market environments are illustrated by SPY/XLP ↑

By analyzing this long-term chart, we can see that markets are generally in a state of happiness, but 2022 has been dominated by fear. These pockets of fear eventually come to an end, resulting in higher highs for SPY/XLP. I’ve tried to highlight these periods with the red levels, displaying how these breakouts often lead to substantial extensions higher. With SPY/XLP breaking out of a new resistance range, it’s very possible that this momentum thrust could foreshadow a larger extension.

2. SPY/XLP vs. Bitcoin:

When I was analyzing the chart above, my mind immediately saw similarities to the price chart of Bitcoin. Out of curiosity, I decided to overlay the long-term price chart of Bitcoin on top of SPY/XLP. The results blew me away:

This is such a significant finding because it helps to visualize how Bitcoin’s price movements are a function of risk appetite (in addition to the fundamental value-drivers of the digital monetary network). As risk appetite increases, illustrated by rising SPY/XLP, Bitcoin also rises in tandem. The inverse is equally true, showing how a substantial decline in risk appetite is visualized by a decline in SPY/XLP & BTC.

With SPY/XLP & Bitcoin showing signs of life since the YTD lows, it’s very possible that risk appetite is prepared for a sustained increase.

3. Semiconductors SMH 0.00%↑ vs. Nasdaq-100 QQQ 0.00%↑ (SMH/QQQ):

Focusing on technology equities, I think this ratio is arguably one of the most important variables to monitor. Considering that technology stocks provide high beta returns relative to the broader market, and semiconductor stocks are high beta tech stocks, this helps us to visualize how investors are viewing tech-related risk exposure.

In a post-Great Recession environment, semiconductor stocks have been fairly unparalleled in terms of producing outsized returns in the technology sector. However, semi’s have produced little upside relative to the broader tech market since the beginning of 2021. This sideways choppiness is perhaps indicative of a market where return expectations and risk appetite are being reset & investors are simply taking time to digest the current market environment.

From my perspective, the semiconductor industry is one of my favorite long-term investment ideas as the world becomes increasingly dependent on data, compute power, and artificial intelligence. This “pick & shovel” play on technology is a no-brainer in my opinion, based on my own risk appetite.

Eventually, this sideways range will produce an important breakout or breakdown below the key structure in this chart. When it does, I think we’ll have a better sense of direction, but I’ll continue to DCA into my favorite semiconductor stocks.

S&P 500 Under-The-Hood Metrics:

Every week, I report on the key developments that I’m seeing for the S&P 500. For the past 6 weeks, I’ve been discussing how we’re generally seeing constructive developments in these metrics. This week, we’re getting more confirmation of this trend, indicating that the fundamentals within the S&P 500 are continuing to improve.

Could they get worse from here? Absolutely. But they are unquestionably improving right now. Here’s what I’m seeing:

164 stocks in the index have a positive YTD return vs. 133 last week.

224 stocks are trading above their 200-day moving average vs. 178 last week.

224 stocks are down at least -20% from their 52-week highs vs. 273 last week.

95 stocks are down at least -30% from their 52-week highs vs. 126 last week.

202 stocks are making new 20-day highs vs. 70 last week.

2 stocks are making new 20-day lows vs. 26 last week.

133 stocks are making new 50-day highs vs. 39 last week.

2 stocks are making new 50-day lows vs. 10 last week.

14 stock is making new 52-week highs vs. 4 last week.

0 stocks are making new 52-week lows vs. 4 last week.

This has to be the best weekly close that I’ve seen in months. Seriously… months! Just look at the rate of improvement in new 20-day highs vs. new lows. We’re witnessing a massive momentum thrust in a broad-based fashion, where nearly every stock is catching bids. Almost half of the index is trading above the 200 day simple moving average, an extremely positive development. Less than half the index is still in official bear market territory (down at least -20% from 52-week highs).

This is strong data all around, but it’s important to note that this doesn’t give us any indication about where the market will go from here! Nonetheless, it provides quantifiable evidence that market internals have drastically improved.

Conclusion:

The momentum thrust that we’ve seen across the equity & crypto markets has been undeniably strong. Considering that I’ve taken a patient approach to increasing risk this year, I’d be lying if I said that I wasn’t having a sense of FOMO in this rally. I’ve had to constantly remind myself that I’m focused on long-term goals of growing wealth rather than taking short-term risks to swing for the fences.

While I’m still not confident that the bottom is in, we’ve now seen quantifiable evidence to support the argument that the bottom is in. The Nasdaq-100 study that I published in July and the Apple Inc. study published above are proof positive of that. Additionally, time is a major factor that increases the likelihood of a bottom. The longer we go without a bottom, the more likely that the bottom is in.

With that said, bear market rallies can be vicious and it’s still impossible to say with any degree of confidence that the market lows are absolutely in.

However, one thing’s for certain: risk appetite is rising considerably & market fundamentals are improving.

Markets don’t bottom on good news, they bottom on less worse news. Over the past 4-6 weeks, we’ve seen the following developments:

Better than expected corporate earnings.

Q2 2022 GDP was negative, but less negative than Q1 2022.

Headline CPI inflation for July was high, but lower than it was in June.

The labor market continues to exhibit resilience & strength.

The Federal Reserve is tightening monetary policy, but appears less hawkish than the market was expecting.

Crypto issues exist with Celsius, Three Arrow Capital, and others, but we haven’t seen more of these issues arise.

Across the board, we are starting to see fundamental improvements and less bad news & that’s a win for financial markets, which are forward-looking pricing mechanisms.

Best,

Caleb Franzen

DISCLAIMER:

My investment thesis, risk appetite, and time frames are strictly my own and are significantly different than that of my readership. As such, the investments & stocks covered in this publication are not to be considered investment advice and should be regarded as information only. I encourage everyone to conduct their own due diligence, understand the risks associated with any information that is reviewed, and to recognize that my investment approach is not necessarily suitable for your specific portfolio & investing needs. Please consult a registered & licensed financial advisor for any topics related to your portfolio, exercise strong risk controls, and understand that I have no responsibility for any gains or losses incurred in your portfolio.

Good shit