Edition #189

Critical Signals For Monetary Policy, Yields, Stocks, and Bitcoin

Investors,

I want to keep this newsletter short and sweet. I published new video analysis on Friday afternoon, reviewing some key market dynamics that I’m seeing in the bond and equity markets. If you don’t have time to read the remainder of this newsletter, which reviews additional data, I’d encourage you to simply watch the video below:

This week was extremely dynamic, with a mix of strong and weak economic data. In particular, labor market data was very encouraging; however, we continued to see general softness in ISM manufacturing data and weakness in the Atlanta Fed’s GDPNow forecast for Q2 2022. The jobs data was the biggest bright spot of the week, giving me confidence that the Federal Reserve is being emboldened to maintain aggressive monetary policy. With the labor market being perceived as too tight and inflation being unequivocally high, the Fed is willing to rebalance the scales by attempting to engineer a softer labor market in order to reduce inflationary pressures. Specifically, here are the key data points showing the strength in the labor market:

1. JOLTS (May 2022):

Series low layoff rate (0.9% & stable) for the second consecutive month.

Historically high quits rate (2.8% vs. prior month of 2.9%).

Total job openings decreased from 11.7M in April 2022 (originally reported at 11.4M) to 11.3M.

2. NFP (June 2022):

372k jobs vs. estimates of 265k.

Unemployment rate = 3.6% vs. prior month 3.6%.

Labor force participation rate = 62.2% vs. prior month 62.3%.

Prime age labor force participation rate = 82.3% vs. prior month 82.6%.

Average nominal wages = +5.1% vs. prior month +5.2% YoY (beat estimates of 5.0%).

All in all, this reflects strong labor market dynamics where employees are in control and employers are desperate to retain high-skilled/qualified workers. The historically elevated quits rate is helping to produce a wage-price spiral, which will likely keep inflation pressures elevated. As mentioned above, this strong data is likely to vindicate the Federal Reserve’s path of monetary policy & rate hike schedule. The stronger the labor market is, the more persistent inflation will be. This gives the Fed a “green light” to remain aggressive in their policy to fight inflation & attempt to diminish demand.

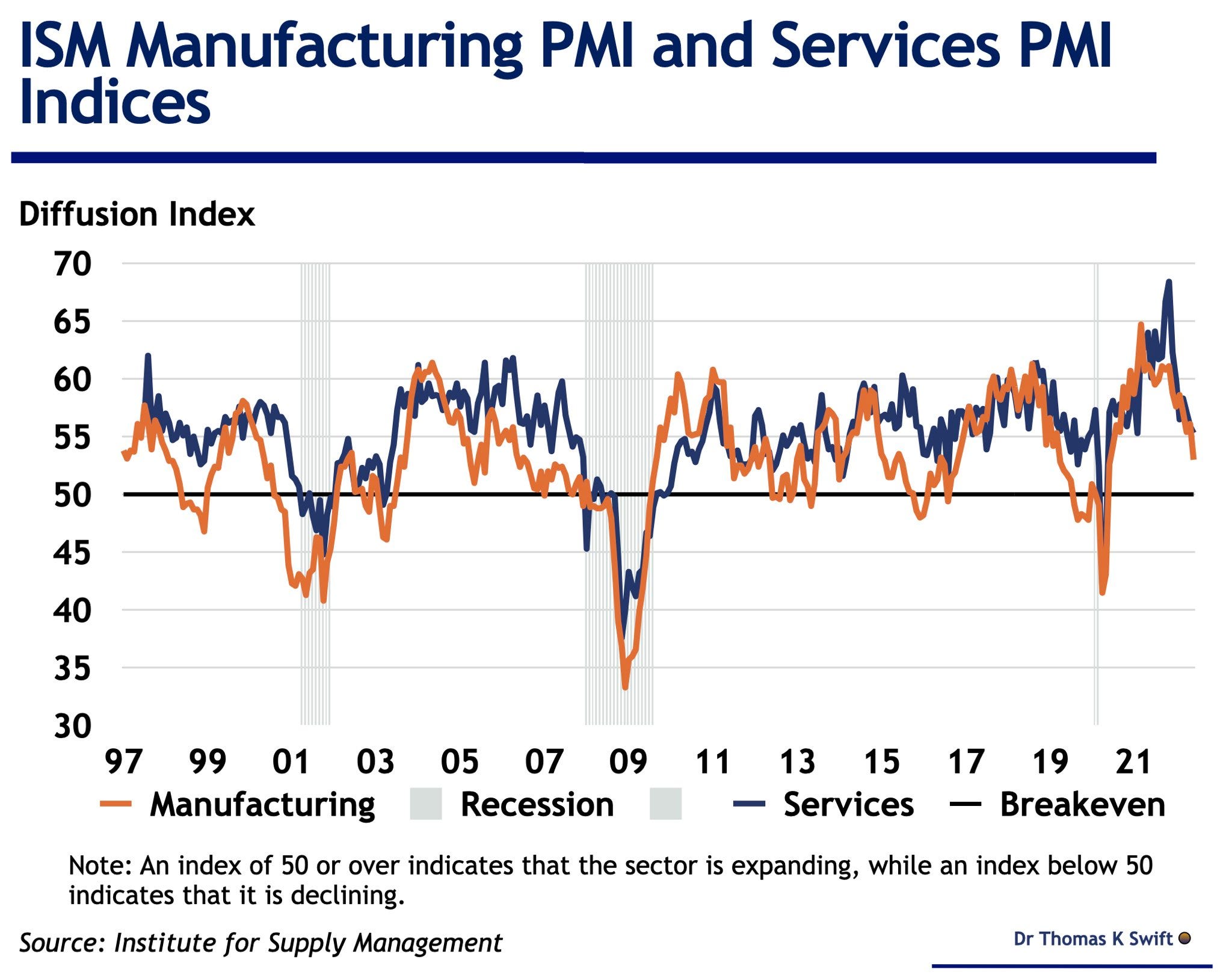

Manufacturing and service sector data continued to soften, as reflected by the ISM & PMI data released earlier in the week; however, they both continue to remain in expansionary territory. The key detail is that we’re seeing a massive deceleration in both of these metrics, trending towards contraction:

The newest inversion of the 2/10 Treasury yield curve is a substantial concern for the medium term, dramatically increasing the odds of a recession on the horizon. How soon that recession manifests is unknown, but investors & market participants should consider this to be an alarm bell.

If we look at the actual yield curve, tracking the yield on each length of maturity, we can see that yields are getting pulled up and to the left, which is referred to as a “flattening of the curve”. Generally, this isn’t a sign of optimism.

Despite the massive increase in yields across the maturity spectrum this week, particularly since Wednesday’s session, I was impressed at the resilience of risk assets. Both equities and Bitcoin generally rallied higher this past week and showed signs of optimism. My immediate takeaway is that the current market rally will soon fade, similar to the market rallies that we experienced in late-January, mid-March, and late-May/early-June of this year. In each of these market rallies, the Nasdaq Composite Index gained between +11% and +16%, but then proceeded to rollover and make new YTD lows.

Bitcoin has also shown resilience to get back above $21,000 in the past few days, which has been an unexpected surprise from my perspective. Similar to the action I’m seeing in the equity markets, I don’t have much confidence that Bitcoin has bottomed; though I am certainly open to the idea that they have. As it pertains to crypto, I’m laser focused on the ratio of ETHBTC as a signal for risk-on or risk-off sentiment.

After failing to remain with the blue channel, I became outspoken in my view that Ethereum (and altcoins) would decline in value relative to Bitcoin. So far that’s exactly what we’ve seen. I raised additional concerns after ETHBTC fell below the teal support range in early June. As it turns out, this prior support range is now acting as clear resistance. Should ETHBTC fall below the diagonal yellow trendline, I’ll expect to see BTC outperform the rest of crypto on the aggregate.

Please keep an eye out for tomorrow’s premium report, which will be exclusive for paid monthly/annual members, where I’ll be reviewing more in-depth analysis on the stock market and the various signals that I’m seeing there.

If you haven’t already signed up for those exclusive research reports, I’d love to have you part of the readership:

Best,

Caleb Franzen

DISCLAIMER:

My investment thesis, risk appetite, and time frames are strictly my own and are significantly different than that of my readership. As such, the investments & stocks covered in this publication are not to be considered investment advice and should be regarded as information only. I encourage everyone to conduct their own due diligence, understand the risks associated with any information that is reviewed, and to recognize that my investment approach is not necessarily suitable for your specific portfolio & investing needs. Please consult a registered & licensed financial advisor for any topics related to your portfolio, exercise strong risk controls, and understand that I have no responsibility for any gains or losses incurred in your portfolio.

Thanks Caleb !

Brief and to the point !