Edition #177

Reasons Why Inflation Hasn't Peaked (yet), Relief Rally or New Bull Market, Altcoins Decimated

Investors,

If you have limited time, here are the core takeaways from this newsletter:

Inflation data continues to remain hot, although it appears to be stabilizing. Or is it? We’re seeing mixed signals in the headline numbers that make it impossible to tell. Certain data that I’m looking at suggests that there’s still plenty of fuel being added to the fire.

The S&P 500’s 7-week streak of losses has come to an end, achieving a monumental rally of +6.6% this week. Investors are forced to question if this rally will also roll over or if it will be able to produce a sustained uptrend. Historically, this data is wildly bullish; but I think it’s reasonable to have concern because of the current monetary policy environment.

Crypto is undoubtedly in a bear market, which I believe is confirmed by the continued downward pressure despite stocks moving higher. This decoupling is concerning (if it sustains). In this environment, I expect to see Bitcoin acquire liquidity from altcoins and therefore outperform the broader crypto market. I’m specifically looking at Bitcoin Dominance, a view of how big Bitcoin is relative to the total crypto market cap. I think Bitcoin Dominance should exceed 60% in the coming months.

Macroeconomics:

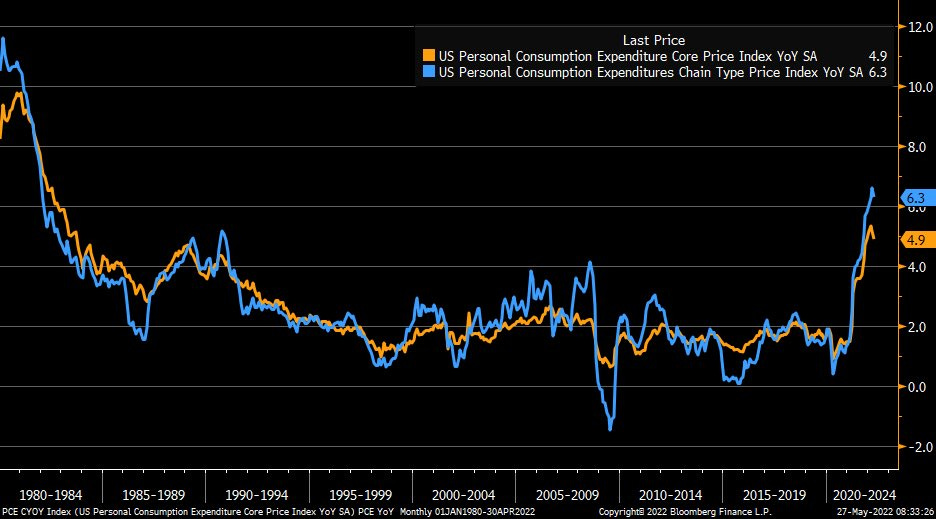

The Federal Reserve’s preferred measure of inflation, the personal consumption expenditures (PCE), was released for April 2022. The headline figure reflected a +6.3% increase relative to April 2021, above analyst expectations for a +6.2% increase. This new data represented a slight decrease vs. the March 2022 report, which showed a +6.6% year-over-year increase; however, the month-over-month increase was still positive at +0.3% from March - April 2022.

The downtick in the PCE is a start, but does not confirm that inflation has peaked. Too many pundits and analysts seem over-eager to pronounce that inflation will only keep going lower from here. These are some of the arguments that I’ve seen:

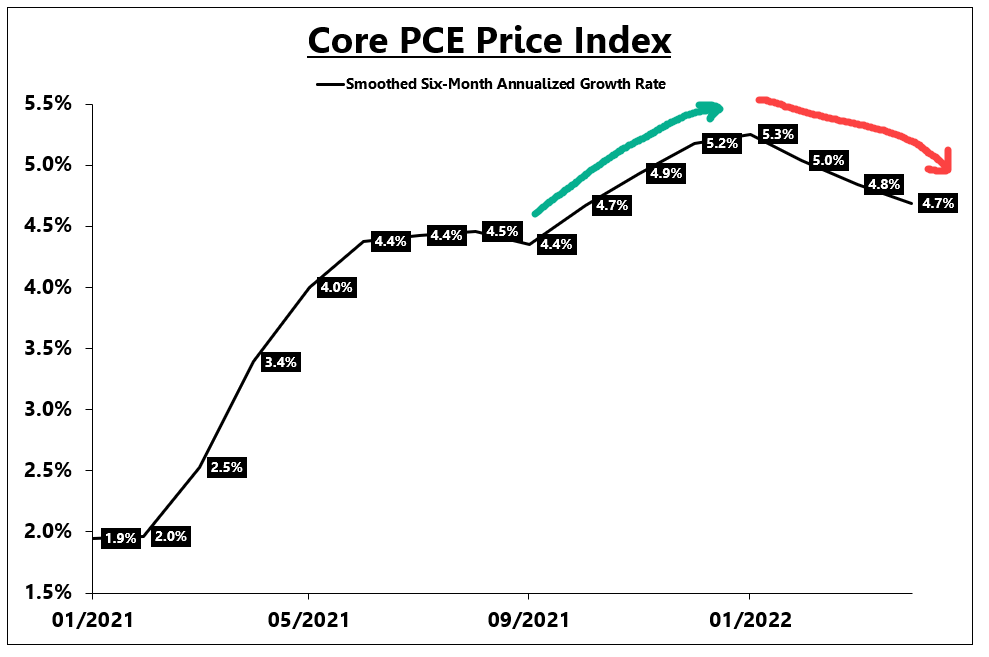

The month-over-month increase in PCE has been +0.3% for each of the past three months, an annualized rate of +4%. In December 2021, the 3-month annualized rate was +6%. Comparing these two periods and the annualized inflation rate derived from each of them, it appears clear that the brakes are being pushed.

The 6-month annualized PCE inflation rate is also turning lower significantly. According to the following chart from Eric Basmajian, core PCE pressures are slowing down:

In response to this data, I’d argue the following: when discussing nominal growth in absolute terms, deceleration ≠ decrease; however, when discussing a derivative of something (rate of change) deceleration = decrease. When we discuss inflation data, such as headline CPI, PPI, or PCE, we measure them in absolute terms by comparing the current month vs. the prior month or the same month in the prior year. Just because they are slowing down, doesn’t mean that they are necessarily decreasing.

When a car is going 80mph on the freeway and the driver slows down to 65mph when they see a police officer ahead, the car is still going 65mph forward. Clearly, they had to decelerate (a term that intrinsically measures rate of change) from 80 → 65mph, but the car is still progressing in a forward manner during the deceleration period.

When we measure the decrease in the annualized rate of change, inflation is still rising! As mentioned, the PCE data has increased by +0.3% on a month-over-month basis for each of the past three months! I’ll be willing to concede that inflationary pressures are decreasing when one or both of the following conditions are met:

The 12-month CPI rate decreases by -0.9% nominally from one month to the next. For example, the April 2022 CPI was +8.3%. If the May 2022 CPI comes in lower than +7.4%, that would be an encouraging sign (in my opinion) that inflation has peaked.

Two consecutive reports in which the month-over-month CPI or PCE falls by at least -0.2% for each month.

If both of these criteria are met, I would feel confident to say that inflation has peaked. However, I have a four primary concerns right now with respect to inflation:

1. Supply Bottlenecks: Supply chains have improved marginally, but are still experiencing bottlenecks. Lockdowns & closures in China are worrisome and will only make these problems worse. According to recent data from the Federal Reserve, the Global Supply Chain Pressure Index remains well-above average & got worse in April.

2. Wage-Price Spiral: With nominal wages continuing to make solid gains, in light of a near-record high quits rate, employees have control over labor market dynamics. With businesses reporting trouble finding skilled labor, these issues seem persistent. The Federal Reserve Bank of Chicago has studied the impact of a high quits rate in research published by Jason Faberman and Alejandro Justinano in 2015, “Job Switching and Wage Growth”. Their research showed that “job switchers drive up wages as they move up the job ladder... Furthermore, theory suggests that since the quit rate helps predict current and future costs of production (through wages), then it should also be important for predicting inflation. We find that these predictions hold true in the data.” They continue that “the pace of job switching is a useful indicator for forecasting the behavior of wages and inflation.” Labor market dynamics are telling us to see continued inflationary pressure.

3. Commodity Pressures: Commodity prices ripple through the economy in multiple facets. Consumers pay higher prices at the pump, with recent estimates showing that Americans are paying $4,700/year at the gas station (a +70% increase relative to last year). Higher prices for fertilizer & agriculture feed equate to higher prices at the grocery store & restaurants. Higher steel, copper, and lumber prices increase the cost of industrial output. The Bloomberg Commodity Index as well as the S&P GSCI Commodity Index both closed at their highest levels since 2014, indicating that a broad-basket of commodities keeps trending higher.

4. Commercial Banking Data: With nearly two years under my belt as a portfolio analyst at a major commercial bank, I’m extremely familiar with how bank data works. In last week’s edition of Cubic Analytics, I covered how commercial & industrial loans as well as total loans & leases are rising substantially. In combination with a decrease in cash held by banks and total reserves held by depository institutions, it appears that newly minted money from the Fed’s QE program is continuously entering the real economy and leaving the financial system. Assuming that the U.S. consumer remains resilient, higher loan issuance will create more inflationary pressures.

For these four reasons, I think inflation has tailwinds to keep rising.

Stock Market:

Last week, I discussed how the S&P 500 had fallen for seven consecutive weeks, an achievement that has only happened three other times since 1950. This fourth occurrence was clearly significant considering how rare these streaks are. Finally, the streak has come to an end with the S&P 500 gaining +6.6% this past week. In last week’s edition, I stated the following:

“I genuinely wouldn’t be surprised for stocks to experience a relief rally in the near future (similar to the price action we experienced from 3/15 - 3/29/22), but I do expect to see continued pressure shortly thereafter.”

Admittedly, I didn’t think the rally would happen immediately or be this significant in terms of magnitude (the last weekly performance of +6.5% or greater happened in November 2020). This was the 19th time that the S&P 500 had a weekly performance of +6.5% or greater since September 1974!

In those scenario’s, the forward looking returns are quite encouraging:

3-month average return: +7%

6-month average return: +14.6%

12-month average return: +23%

Here’s the full table of data, which is nothing short of incredible:

Will this most recent occurrence mirror the returns of the past, or is the current downtrend too strong to break? Keep in mind, this is the 5th rally of +5% so far this year, in which every single rally has been followed by new year-to-date lows. Hence the term “relief rally”, which is merely a short (but powerful) uptrend within a larger downtrend.

Clearly, it’s far too early to tell which way the short-term price action will evolve; however, I continue to think this will be a brutal environment for short-term traders. Meanwhile, long-term investors should be cautiously optimistic, regardless of how short-term dynamics evolve. My number one rule for investing is don’t fight the Federal Reserve. In a monetary tightening regime designed to combat historic inflation, I think asset prices will face headwinds until there is a material shift in monetary policy and/or a material downturn in the inflation data. The data discussed above is merely one study, which should be assessed amongst a broad array of market data in order to determine the weight of the evidence. Still, I think investors should be happy to see some optimistic data.

Bitcoin:

While bonds and stocks were generally able to rally higher this past week, crypto decided to not participate in the upside. At the time of writing, the price of Bitcoin has fallen -1.7% since the prior Friday evening, 5/20/22. Meanwhile, Ethereum has fallen -10.5% over the same window.

I want to focus on one primary topic in this section: the relative outperformance of Bitcoin vs. other crypto assets (and the broader crypto market) during bear markets. First & foremost, here is a great rule of thumb:

So, how has $ETHBTC, the relative performance of Ethereum vs. Bitcoin performed recently? Here’s a chart that I’ve been sharing recently:

I was highlighting the importance of this channel on May 9th, saying that a retest of the lower-bound was my base case scenario. Since then, $ETHBTC has fallen -18%. The failed rebound on the lower-bound & the subsequent breakdown indicate that Ethereum is deteriorating relative to Bitcoin. It’s vital to understand where this ratio peaked: May 2021 & December 2021. These were just after the peaks in the broader crypto market. With a sustained downturn now seemingly underway, I expect to see $ETHBTC retrace lower towards the bottom of this chart and break below 0.04 in the coming months.

As I mentioned at the start of this section, in an environment where $ETHBTC is falling, I expect to see the broader crypto market selloff and trend lower. This means Bitcoin will also fall, but less than the rest. This leads me to analyze Bitcoin Dominance, a metric of Bitcoin’s market cap relative to the total crypto market cap.

During bull market cycles, investor exuberance causes mania across the crypto asset class. This mania produces massive gains in a variety of altcoins, which skyrocket by unfathomable amounts. New crypto projects are created, in which new value is created practically overnight. During these periods, the size of Bitcoin relative to the broader crypto market decreases.

Eventually, the mania ends and investors start to run for the exit. The value that was created overnight disappears just as fast; however, Bitcoin continues to operate. Considering that every other crypto protocol is built, managed, and owned by a company (Ethereum, Luna, Solana, Avalanche, Polygon, etc.), the weakest and most useless always go belly-up. When they do, liquidity floods back into the apex digital asset: Bitcoin. During these periods, bear markets, Bitcoin Dominance rises.

Based on the long-term structure of Bitcoin Dominance, and the general acceptance that we are now in a bear market, I think it’s very reasonable to see Bitcoin dominance exceed 60% in the coming months vs. the current reading of 46.5%. Considering that it was less than 40% at the start of 2022, I think this is feasible. The analysis I provide above indicates that we could return as high as 70%, but I don’t know if that’s within the probable set of outcomes right now. Nonetheless, I expect to see altcoins lose a significant amount of value relative to Bitcoin in the current market environment. I have drastically reduced my altcoin exposure in the month of May, conceding to the pressure of the market and being willing to objectively analyze and adjust to the data in front of me.

Talk soon,

Caleb Franzen

DISCLAIMER:

My investment thesis, risk appetite, and time frames are strictly my own and are significantly different than that of my readership. As such, the investments & stocks covered in this publication are not to be considered investment advice and should be regarded as information only. I encourage everyone to conduct their own due diligence, understand the risks associated with any information that is reviewed, and to recognize that my investment approach is not necessarily suitable for your specific portfolio & investing needs. Please consult a registered & licensed financial advisor for any topics related to your portfolio, exercise strong risk controls, and understand that I have no responsibility for any gains or losses incurred in your portfolio.