Investors,

I want to take a moment to celebrate the 1-year anniversary of launching this newsletter! My first publication had roughly 20 subscribers (mostly some former colleagues, family, and friends) on the first distribution list. Today, Cubic Analytics has 900+ subscribers!

The momentum over the past year has blown me away, but we’re still in the early stages of what I’m trying to create. If you’ve gained value from this newsletter over the course of your membership, I encourage you to share Cubic Analytics with your network and help this endeavor continue to grow. Also, take advantage of the free 7-day trial that I’m offering in order to gain access to the premium research I publish for paid members.

If the research doesn’t live up to your expectations, you can cancel with zero risk within the 7-day trial! This is the first time I’ve run this kind of promotion, and I’ve been happy to see so many investors upgrade their subscription.

Macroeconomics:

In light of the Federal Reserve embarking on a path of monetary tightening, I wanted to review important commercial banking data and to discuss the impact on broader economic & financial conditions. Let’s briefly review the current monetary policy environment & projected path of policy decisions:

The Federal Reserve has lifted the target for the federal funds rate from 0.00%-0.25% to 0.75%-1.00% as of early May 2022.

Recent comments by key Federal Reserve members have indicated that they are prepared to raise interest rates by +0.5% in the upcoming two meetings, while reiterating that a +0.75% hike is on the table.

Their policy decision announcement on May 4th indicated that the Fed will formally begin selling the assets on their balance sheet at a rate of $47.5Bn/month in June 2022. They expect to maintain this rate of selling activity through August 2022, at which point they will increase their balance sheet runoff to $95Bn/month thereafter.

Of course, all of these projections are subject to change based on the incoming economic data; however, this is what the Fed has currently communicated to the market. While the Fed’s actions have been deliberate, their rhetoric has been significantly more aggressive than their actions. This has allowed the bond market to do the heavy-lifting for the Fed, forcing interest rates on Treasuries and corporate debt to rise in advance of Fed policy.

As a result, financial conditions are tightening based on recent data Bloomberg from Robin Brooks:

This data reflects an important dynamic: while still historically loose, financial conditions are tightening rapidly even though the Fed’s actions haven’t been congruent with such tightening. The Fed is teaching us that words can be as important as actions with respect to the impact of monetary policy on financial markets.

I wanted to get confirmation of this trend, so I found fantastic data from the Federal Reserve Bank of Chicago measuring the National Financial Conditions Index:

This data validates the data in the first chart, proving that risk, credit, and leverage are all getting tighter. However, the most recent data for the period ending May 13th was -0.23, confirming that financial conditions are below the “loose” threshold for now. With financial conditions getting tighter, but still considered to be loose, how is the banking data being impacted?

First & foremost, banks are substantially increasing their lending activity and/or businesses are increasing their demand for loans. In the chart below, we’re analyzing the total balance of commercial & industrial loans (top) and total loans & leases of U.S. commercial banks. It’s worth noting that C&I loans, typically considered a loan to expand the productive capacity of a business, are a subset of total loans & leases, which also includes loans secured by real estate, loans to financial institutions, consumer loans, and loans to the agriculture sector.

Both are rising considerably since November 2021, when the Fed announced that it would begin reducing the pace of their asset purchases. Why? With the substantial rise in interest rates, we’re seeing two dynamics take place:

Banks, who generate revenue by issuing loans and collecting interest payments, have been able to make loans at higher interest rates since November. With the opportunity to generate higher revenue on a single dollar of loans, they have an incentive to issue more loans.

Businesses, who rely on financial planning to allocate capital and acquire new debt, have been forecasting that interest rates will continue to rise substantially. As such, they’ve had a fire under their asses to lock-in new debt at interest rates today in order to avoid higher interest rates tomorrow.

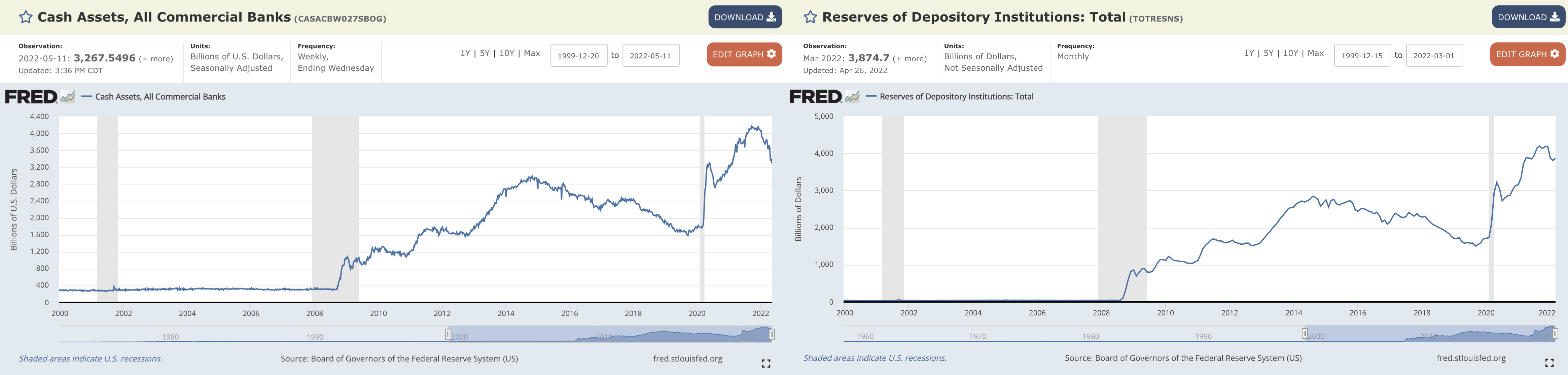

The combination of these two factors is what’s driving the increase in C&I and total loans & leases, purely caused by rising rates and the expectation of rates to rise even more. We can confirm this trend with two other data points: cash assets of commercial banks and reserves held by depository institutions:

Based on this data, we can see that both cash & reserves are falling from their recent all-time highs. This confirms that banks are reducing their cash balances in order to issue more loans and generate interest payments (revenue) from their clients. As a result of increased lending activity, we’re seeing newly minted money from the Fed’s historic stimulus leave the financial system and enter the real economy. With reserve notes & cash now becoming productive loans in the real economy, my interpretation is that this will add pressure to the inflationary environment. In light of ongoing supply chain bottlenecks, lockdowns in China, wage pressures, and higher producer costs, I expect to see inflation data remain above 8% in the upcoming months and potentially exceed 9.3% on a trailing 12-month basis.

This prediction fits within my prior forecast in May 2021 that consumer price inflation will reach the 6% to 10% range. If this prediction manifests into reality, I expect to see an even more aggressive stance from the Federal Reserve, who will be stuck between a rock and a hard place trying to fight inflation while not forcing the U.S. economy into a recession.

Stock Market:

Stocks and bonds are having historically poor starts in 2022, something that none of you need a reminder of. We’re all witnessing our portfolios, 401k’s, and brokerage accounts decline regardless of our risk allocations. On a YTD basis, here’s the performance of the major U.S. indexes:

Dow Jones Industrial Average $DJX: -14%

S&P 500 $SPX: -18.1%

Nasdaq-100 $NDX: -27.5%

Russell 2000 $RUT: -21%

Meanwhile, the 20-year Treasury Bond Fund $TLT is down -20% YTD.

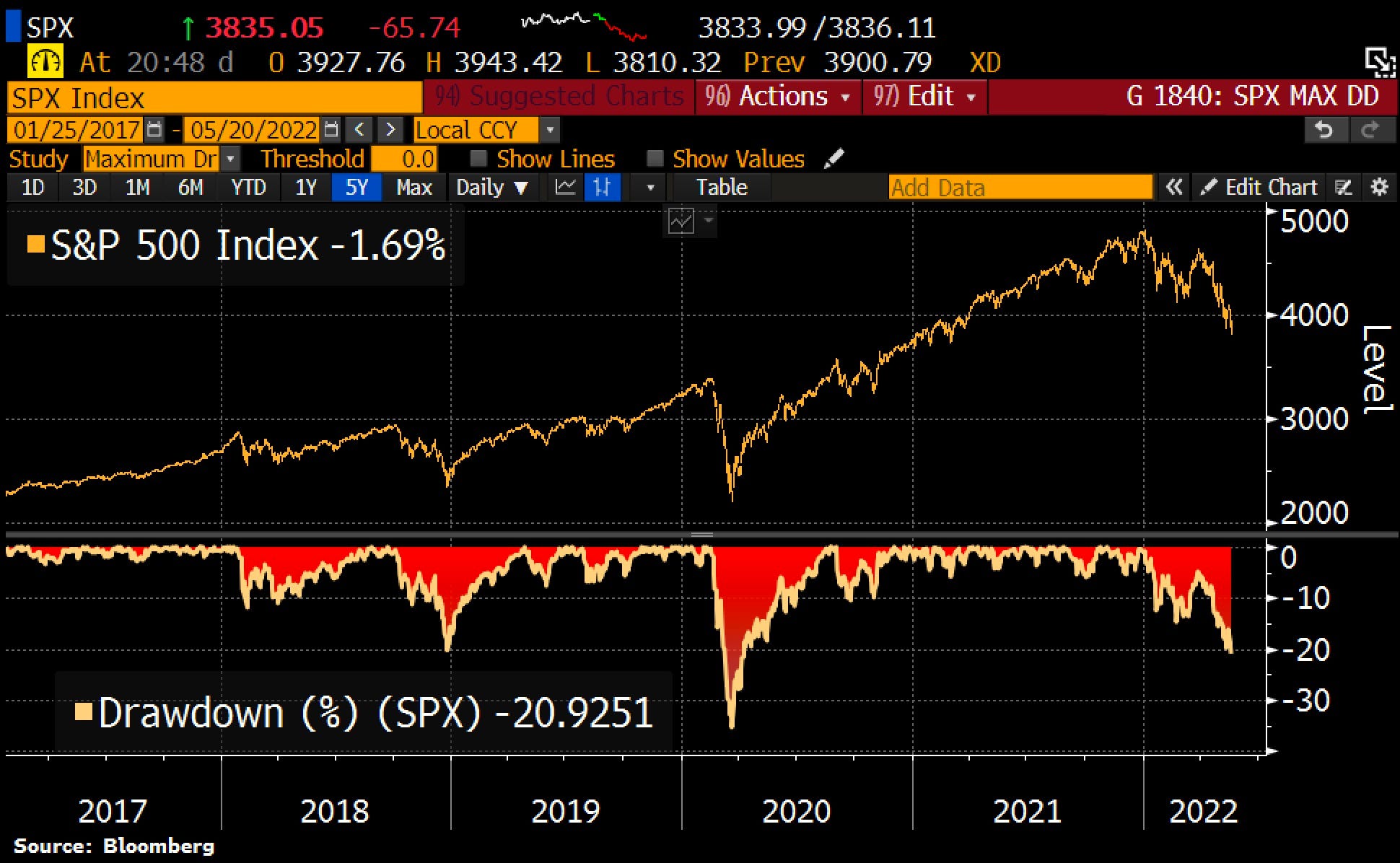

On Friday’s session, the S&P 500 entered bear market territory (down at least -20% from 52-week highs), but stocks rallied in the second half of the session & closed in a much better position. Still, each of the indexes are reflecting clear signs of deterioration, something we’ll continue to cover in the weekly Premium Market Analysis reports.

At one point during Friday’s session, the S&P 500 officially reached a drawdown of -20.9% and entered bear market territory:

Aside from the 2018 hiking tantrum and the COVID crash, the current drawdown in the S&P 500 is the worst in the past five years. Additionally, the S&P 500 has just completed the seventh consecutive week of negative weekly returns, the first such streak since Q1 2001 in the midst of the dot-com burst. During that period, the S&P 500 went on to achieve eight consecutive weeks of negative returns, then proceeded to rally +15%, and then decline an additional -41% to the 2002 lows. Here’s what the price action looked like, from 1999-2003:

Interestingly, the S&P 500’s current 7-week losing streak is only the third such streak since 1980 and only the fourth since 1950. Clearly, these streaks don’t happen often and it’s therefore hard to extract any meaningful takeaways from their occurrence. Consider the 1980 case, which fell for a total of seven consecutive weeks:

Unlike the 2001 case, the seventh week of the 1980 case was quite literally the bottom of the market and it proceeded to rip +40% over the next 36 weeks. On a forward-looking basis, here were the key returns for the market after the seventh week:

1-year: +33%

2-years: +10%

3 years: +49%

This is a stark difference compared to the 2001 scenario, in which the forward-looking returns were:

1-year: +2%

2-years: -27%

3 years: +2%

If I had to lean one way or the other, I think the current dynamics are more similar to 2001 than 1980. I genuinely wouldn’t be surprised for stocks to experience a relief rally in the near future (similar to the price action we experienced from 3/15 - 3/29/22), but I do expect to see continued pressure shortly thereafter. In a scenario where the market rallies, I will stick to the same plan I’ve been laying out to premium members: reduce exposure to lower-conviction names and non-core holdings while continuing to dollar-cost average (DCA) into high-conviction, long-term holdings.

Bitcoin:

If you’re aware of the carnage in U.S. stocks, you’re certainly aware of the larger carnage taking place in crypto. Even still, Bitcoin is holding up quite well in light of the macro factors that are impacting market conditions. To contextualize the circumstances, we’re dealing with: a major geopolitical conflict, 40+ year high inflation rates, a contracting U.S. economy, historically negative investor sentiment, a rapid acceleration in yields, the threat of a recession, and a Federal Reserve poised to combat inflation with an aggressive tightening regime. Under these circumstances, Bitcoin is down -36% YTD. Without question, Bitcoin’s performance is significantly worse than any of the U.S. stock market indexes, the bond market, or emerging market stocks. However, considering that Bitcoin is only a 13-year old asset, I think it’s shown resilience during this period.

Regarding the price structure, we continue to consolidate within a critical support zone:

In my opinion, it’s vital for price to remain above this $28.9k-$30.2k range, although I wouldn’t be surprised to see a quick flush below this range and then a rebound back above it. Either way, a breakdown below this range substantially increases bearish outcomes in the short-term.

Similar to the S&P 500’s streak of weekly losses, Bitcoin is currently in the midst of an eight week of consecutive losses. This is the longest such streak in Bitcoin’s history. In addition to this historic streak, Bitcoin is also experiencing another historic signal.

Below is the weekly chart of Bitcoin since 2011, in logarithmic scale. The indicator at the lower-bound is the 26-week Z Score, measuring where the current price stands within a normal distribution of the 26-week price history at any given moment.

The current reading is -2.02, meaning that the current price is more than 2 standard deviations below the mean price over the past 26 weeks. Why 26 weeks? It’s essentially half a year of data. As we can see, this has only happened four other times in Bitcoin’s history, an important signal to show just how oversold the digital asset is. Could it stay oversold, or become more oversold? Yes. However, this data shows that the current price is trading at an attractive discount relative to historical standards.

While the short-term price action is almost certain to be volatile, my long-term conviction in Bitcoin is still remarkably strong, and I think this is providing a solid opportunity to dollar-cost average into Bitcoin over the next 6-12 months.

Talk soon,

Caleb Franzen

DISCLAIMER:

My investment thesis, risk appetite, and time frames are strictly my own and are significantly different than that of my readership. As such, the investments & stocks covered in this publication are not to be considered investment advice and should be regarded as information only. I encourage everyone to conduct their own due diligence, understand the risks associated with any information that is reviewed, and to recognize that my investment approach is not necessarily suitable for your specific portfolio & investing needs. Please consult a registered & licensed financial advisor for any topics related to your portfolio, exercise strong risk controls, and understand that I have no responsibility for any gains or losses incurred in your portfolio.