Investors,

In light of continued market pressure, and seemingly unprecedented dynamics, I wanted to share new thoughts as a follow up to my March 5, 2022 piece “Navigating Uncertainty”. In that newsletter, Edition #157, I addressed the critical risks that we were facing at the time. Since then, those risks are increasingly impacting asset prices, financial markets, and the economy.

Today’s newsletter serves as an update on the dynamics discussed in Edition #157, analyzing new data & charts to provide fresh perspectives on market conditions. The asset markets are having a historically challenged year, one where investors have no reprieve from market pressure, particularly since the end of March 2022. In this environment, negative performance has created historically negative sentiment, therefore creating a feedback loop and recursive nature to the selloff.

I’m hopeful that the perspectives in this newsletter will provide clarity on these market dynamics, and provide insightful ideas about where markets might be going. As always, I’d love to hear your thoughts and I encourage you to share this with other investors who are interested in these topics!

Introduction & Review:

To briefly summarize Edition #157, I highlighted one factor as the primary culprit of downside market pressure: rising interest rates.

The upward pressure on yields was being caused by two factors:

The monetary policy environment: The Federal Reserve shifting from monetary easing (QE), to tapering their asset purchases (reduced QE), to monetary tightening (QT). The transition between these phases has happened faster than anyone anticipated at the beginning of the year, causing the bond market to effectively adjust to the actions & rhetoric of the Federal Reserve.

The inflation environment: With inflationary pressures continuing to grow, the bond market is actively adjusting & signaling that higher/more sustained inflation is coming. Higher inflation means that demand for bonds will fall, forcing bond issuers to increase the yield on their debt to attract investors. Alternatively, the bond market may be signaling that the projected path of monetary tightening will be ineffective to combat inflation, therefore forcing the Fed to be even more aggressive.

In response to rising yields, impacted by the two dynamics listed above, asset prices have faced significant pressure in 2022. All else being equal, interest rates and yields have an inverse causation on asset prices. In a vacuum, it’s mathematically proven that:

Yields ↓ = Asset Prices ↑

Yields ↑ = Asset Prices ↓

Shortly before I published “Navigating Uncertainty”, Russia had officially invaded Ukraine. The geopolitical conflict dramatically reduced the risk appetite of investors, resulting in a “rush-to-safety”. In turn, this increased the demand for bonds, putting short-term downward pressure on yields from February 16th (one week before the invasion) through March 1st (one week after the invasion). In “Navigating Uncertainty”, I explained the following:

“This brings us to an interesting inflection point: yields are rising because of rising inflation and because the Federal Reserve is tightening monetary policy; however, yields are falling because of geopolitical conflict and uncertainty. This tug-of-war is causing heightened volatility in the market”.

In closing, I made it clear that the Federal Reserve’s monetary policy would produce tailwinds for rates to rise even further, therefore putting more pressure on asset prices:

“I think bond yields will resume their upward momentum, despite the recent dip as a result of the Ukraine/Russia conflict. My belief is that inflation will continue to accelerate and remain elevated for the remainder of 2022 (likely above 5% on a trailing twelve-month basis). Additionally, my number one rule is don’t fight the Federal Reserve. At the present moment, the Federal Reserve is committed to ending their asset purchases and raising interest rates. Rising/persistent inflation, a strong labor market, and monetary tightening are likely to push yields higher.”

Since then, the 10-year Treasury yield has risen from 1.72% to 2.87% as of 5/11/22. While this symbolizes a 1.15 percentage point increase, yields have risen by +67% over the course of the last two months! In fact, this recent period has been the fastest 8-week positive rate of change in more than 25 years!

While the 8-week rate of change has cooled off over the past two weeks, the recent acceleration was very unique. In closing, I suggested that long-duration assets, like technology stocks, would face downward pressure in this rising rate environment. In particular, I listed $ARKK, $IPO, and $XBI as the key areas to avoid: SaaS, internet, high growth, and biotech.

I also suggested that energy & commodity-related stocks were likely poised to outperform the broader market during this period, benefitting from inflationary pressures and the Russia/Ukraine conflict. Broadly speaking, these downside & upside ideas have produced strong results. Since my initial research on 3/5/22, we’ve seen the following:

S&P 500 $SPX -7%

Nasdaq-100 $NDX -10.6%

Ark Innovation ETF $ARKK -27.6%

Renaissance IPO ETF $IPO -22.9%

Biotechnology ETF $XBI -18.1%

Energy ETF $XLE +7.3%

Oil & Gas Exploration ETF $IEO +8.6%

Oil & Gas Services ETF $OIH +0.5%

Clearly, the three groups I suggested to avoid have dramatically underperformed the market while the energy-related areas have dramatically outperformed the market.

Financial Markets & Asset Prices

Here are the returns for core assets & financial markets since November 3, 2021, when the Federal Reserve officially announced their tapering process:

Stock Market:

Dow Jones Industrial Average $DJX: -10.9%

S&P 500 $SPX: -13.6%

Nasdaq-100 $NDX: -23.3%

Russell 2000 $RUT: -25.5%

Bond Market:

iShares Trust 20-year Bond ETF $TLT: -20.3%

iShares Trust Core U.S. Aggregate Bond ETF $AGG: -10.4%

iShares Trust High Yield Corporate Bond ETF $HYG: -11.6%

PIMCO 25+ Year Zero Coupon US Treasury Index ETF $ZROZ: -26.3%

Crypto:

Bitcoin $BTC: -51.9%

Ethereum $ETH: -54.8%

Total Crypto Index $TOTAL: -52.9%

Commodities:

Crude Oil Futures: +37.4%

Natural Gas Futures: +30.3%

Gold Futures: +2.2%

In my concluding remarks from Part 1 of “Navigating Uncertainty”, I highlighted the uncanny correlation between $ARKK and the 10-year Treasury yield in order to highlight how further increases in yields would punish assets like $ARKK and the stocks within it. Since then, the relationship between these two variables continues to be perfectly inversely correlated, confirming that risky, long-duration assets are most impacted by rising yields.

In the chart below, we’re comparing $ARKK (candles) vs. the inverted 10-year Treasury yield (teal). Therefore, a decline in the teal line is representative of yields rising (hence why the left y-axis is negative).

The rising yield environment is pushing asset markets into disarray. With the carnage in the stock & crypto markets, you’d generally think that bonds would be providing a safe haven. However, this simply hasn’t been the case. With bonds providing zero protection, and even worse returns than the stock market, investors are gasping for air.

Commodities have been the only beneficiary of recent market dynamics, aided primarily by the inflationary environment facing the global economy. Even still, precious metals like gold & silver have been extremely underwhelming in this environment, providing little solace (if any) to their owners. The Bloomberg Commodity Index, $BCOM, is up +1% since Part 1 of “Navigating Uncertainty”; however, the Index is up a total of +29% so far year-to-date.

Crypto is experiencing severe market declines, still viewed as a high-beta asset in traditional finance. While it’s seemingly correct to say that Bitcoin has been correlated to the stock market over the past several months, it’s important to highlight that correlation ≠ causation. Additionally, pointing out this correlation misses a critical point: it isn’t that Bitcoin and stocks are correlated, it’s that Bitcoin and stocks are both directionally correlated with yields!

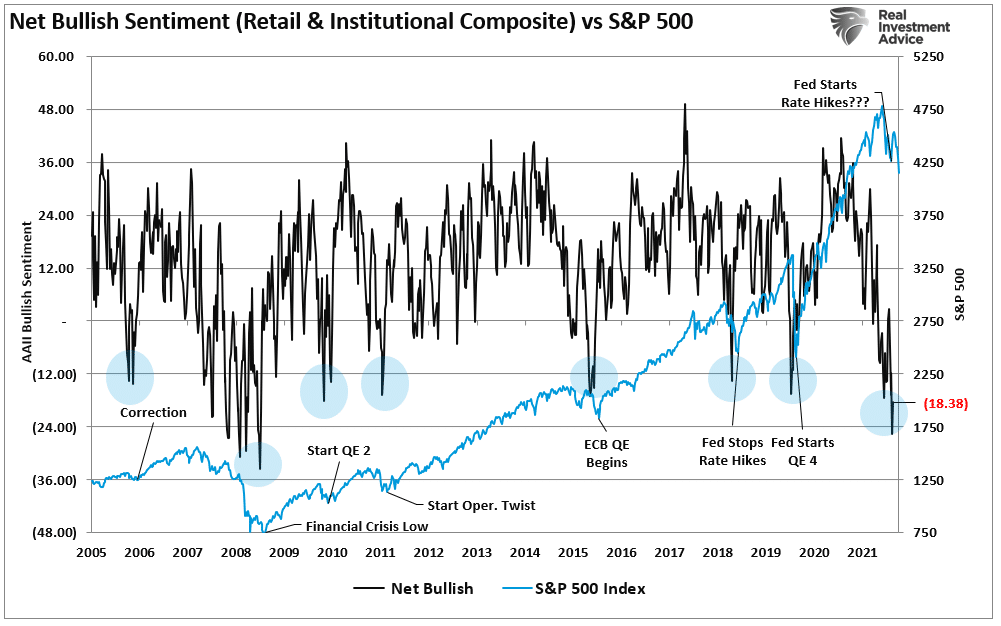

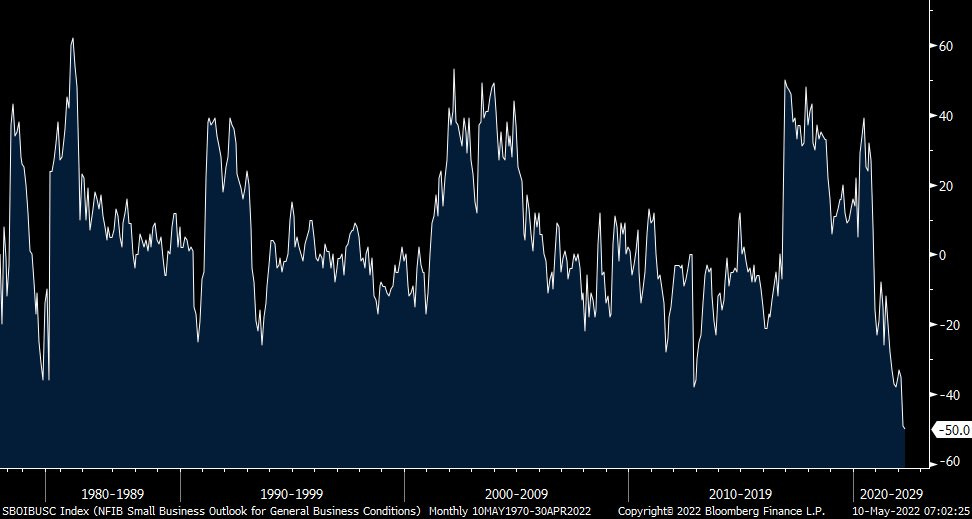

On top of the natural pressure created by rising rates, increasingly negative investor sentiment is adding fuel to the fire.

{kind=link}

Based on this chart from RIA, net bullish sentiment is historically negative — the lowest it’s been since the Great Recession. Such negative sentiment isn’t exclusive to the stock market, as the NFIB’s recent small business survey indicates a record low of businesses expecting better business conditions over the next six months:

Essentially, financial markets and the economy are resetting expectations amidst record inflation, monetary tightening, a decelerating/contracting economy, and a system that has been oversaturated with monetary & fiscal stimulus.

Regarding the individual indexes, the three major markets are displaying major signs of weakness & breaking below critical support levels.

1. The Dow Jones Industrial Average $DJX: The Dow has held up better than the other indexes and is also reflecting the most strength in terms of the price structure. Still, it’s unquestionably weak. The index is trading below the top grey range, producing lower lows and lower highs (red channel). The lower-bound of the red channel has been vital for the market, doing an excellent job of rebounding on each retest. If shares break below this support zone, I think a return to the pre-COVID highs is likely. That would imply additional downside of roughly -8.5% from current prices.

2. The S&P 500 $SPX: The S&P is materially weaker than the Dow Jones, particularly since the market pressure we’ve experienced over the past 6 weeks. The index briefly broke below the red channel this week, implying that the important support level is losing strength. I think it’s possible we see continued downside pressure next week, as the lower-bound of the channel may turn into resistance after previously acting as support. In this scenario, I think a further decline of the S&P 500 to $3,500 (white levels) is reasonable.

3. Nasdaq-100 $NDX: The technology index is the weakest of the three, continuing to cut below major support levels from the past 18+ months. This past week, the Nasdaq fell below the important resistance range from Q4 2020, that eventually flipped into support in December 2020 & March 2021. We know that this is a critical level because of the distinct behavior of buyers and sellers when price was previously in this range. Could this be a fake breakdown? Yes. Could it be the start of another leg down? Yes. I tend to lean towards the latter, implying that this grey range can act as resistance at the start of this upcoming week. Thankfully, we’ll have an answer soon.

On the aggregate, each of the major indexes are showing further signs of deterioration after incurring steady losses all year. I believe that the markets will have rallies and brief extensions higher, but that these will largely be short-lived, so long as there isn’t a material shift in the monetary policy environment.

We’ll talk more about my expectations at the end…

Economic Conditions:

First & foremost, I want to highlight the evolving dynamics between the effective federal funds rate (FFR) and the 2-year Treasury yield. Considering that the Federal Reserve is directly involved in both of these markets, it’s understandable to see why the FFR and the 2-year yield tend to move in the same direction.

I’ve been sharing this chart for months as a way to prove that the Federal Reserve is “behind the curve”, implying that their monetary policy framework is disjointed from where it should be. While the Fed has raised the FFR by a total of 0.75% over the past few months, it’s clear that the gap between these two variables is still historically elevated.

Interestingly, we’re starting to see a dip in the 2-year Treasury yield, which may prompt some analysts to speculate that yields will fall lower from here. To that perspective, I would encourage people to look at the 2004-2007 era, in which the 2-year yield had multiple head-fakes to the downside while the Fed continued to raise interest rates. In my opinion, as I’ve stated multiple times, the current monetary policy environment will produce tailwinds for yields to rise further. This is the path of least resistance, aligned with the policy actions by the Federal Reserve. Barring a material shift in the actions and/or rhetoric of the Fed, I believe yields across the financial system are poised to rise, a stance I’ve held since Q4 2021.

As additional proof that the Fed is behind the curve, here’s an excellent graphic from Holger Zschaepitz highlighting the ongoing divergence between the Federal Reserve’s policy rate and the 12-month inflation rate in consumer prices:

Considering that the inflation rate is the highest it’s been since the early 80’s, it’s clear that the Fed’s policy rate has a lot of room to catch up. On Thursday, May 12th, Jerome Powell said that “it would be appropriate for there to be additional 50 bps rate hikes at next two Fed meetings.” Without question, the Fed is prepared and willing to execute on this plan, committed to fighting inflationary pressures amidst an extremely tight labor market.

Because the Federal Reserve operates under a dual-mandate to promote price stability and maximum employment, the Fed has approximately met half of their goal with the success of the labor market. Here are some key datapoints that represent the conditions of the labor market:

As of April 2022, the unemployment rate is 3.6% (near all-time lows).

As of March 2022, the quits rate is 3.0% (near all-time highs).

As of March 2022, the 12-month net employment gains totaled 6.3M.

On March 30, 2022, there were 11.5M job openings. For the entire month of March, there were 6.7M hires, 4.5M quits, and 1.4M layoffs.

As of April 2022, nominal average hourly earnings increased by +0.31% relative to March 2022, and increased +5.46% on a 12-month basis.

This data tells us a few things. First, the labor market is very tight, given by the low unemployment rate and high quits rate. A high quits rate is actually a positive thing in my opinion, reflecting the ability of the currently employed to find better opportunities, higher pay, and positions more aligned with their interest and skills. This will drastically increase the optimality of the labor market.

However, there are also some glaring areas of weakness. Most notably, the labor force participation rate is at a historically muted level, currently at 62.2%. In addition, while nominal average hourly earnings are increasing, inflation is actively reducing the purchasing power of the labor force. Adjusting for inflation, the real average hourly earnings decreased by -2.7% over the 12-month period ending March 2022.

The labor market isn’t perfect and will continue to have flaws; however, I would argue that the labor market will be able to withstand a monetary policy regime that will allow the Federal Reserve to steadily combat inflation.

Remember, the Fed isn’t raising interest rates by +3.0% at once! They appear committed to consecutive 0.5% rate hikes, reiterating that they can do more or less depending on how the data evolves. Whether the Fed will properly engineer a soft-landing is still up for question; however, it appears that the labor market is giving them the ability to raise interest rates substantively.

This brings us to inflation…

Quite simply, inflationary pressures aren’t subsiding. The April 2022 CPI data was released this past week, in which the 12-month inflation rate was +8.3%. While this came in slightly lower than the March 2022 data (+8.5%), this isn’t a material decline to suggest that inflation has peaked. Even if inflation has stabilized here, which isn’t certain, the inflation rate remains at historically elevated levels.

Additionally, while the 12-month inflation rate marginally declined, the month-over-month rate of inflation was still positive. The consumer price index increased by +0.3% from March 2022 to April 2022. In my opinion, it’s inaccurate to say that inflation has stabilized or is rolling over. We simply don’t have enough data to confidently suggest that it has.

With Q1 2022 GDP contracting at an annualized rate of -1.4%, the threat of stagflation is staring the U.S. economy in the face. This dynamic may continue to escalate, indicating that inflationary pressures remain elevated during a period of economic contraction. It’s too early to tell based on one quarter of GDP data, so there’s a lot at stake for the Q2 2022 data. Unfortunately, that data is a few months away from being released, so we’ll need time in order to resolve questions about stagflation. This will put more pressure on the monthly inflation readings, for both consumer and producer prices.

Inflation hasn’t been contained to consumer prices, with the Producer Price Index (PPI) also at historically elevated levels:

The April 2022 data reflected an annual increase of +11.0% vs. analyst estimates for a +10.7% increase. With a relatively strong U.S. consumer, businesses are finding confidence in their ability to pass higher producer prices onto the final consumer, particularly in light of nominal wage increases and a tight labor market. Ironically, the strength and ability of the consumer to absorb higher prices is creating a recursive impact on inflationary pressures.

The 10-year Treasury yield will continue to be one of the best metrics to gauge inflationary dynamics in real-time. Bond investors have always been referred to as “the smart money”, implying that dynamics in the bond market are typically an excellent gauge for economic projections and dynamics. If yields continue to rise at an accelerated pace, as they have since November 2021, I will interpret this as bond investors forecasting higher & more sustained inflation.

The 10-year Treasury yield recently retested the multi-year highs I’ve been highlighting on Twitter, getting immediately rejected within this white range from 2018. While the immediate reaction has been a rejection, I think the monetary policy environment will cause 10-year yields to break above these 2018 highs and extend to levels from before the Great Recession.

If we see that yields move lower from here, this will benefit asset prices in the short-term, likely causing technology stocks and crypto to rally substantially. If we see a breakout in the near future, that will put additional pressure on risk assets in the short-term. As always, watching 10-year Treasury yields will be a critical factor in my assessment of financial market conditions and risk appetite.

What’s Next:

Since December 2021, I’ve err’d on the side of caution regarding the stock market, based purely on my understanding of the shift in monetary policy. Even still, the perspectives that I shared in my “Investment Outlook for 2022” were too optimistic, despite calling for a 70% chance of below-average S&P 500 returns this year and a 10% chance of poor market returns.

On Twitter and in various editions of my newsletter over the past 4-6 months, I’ve stated that the current monetary policy environment and economic dynamics are creating tailwinds for yields to rise. Barring a material and sustained shift in the path of monetary policy, additional increases in interest rates will put downward pressure on asset markets. This will predominantly punish software, technology, and internet stocks, as well as retail & consumer discretionary stocks. This is why I’ve been outright bearish on $ARKK, $IPO, and $XBI constituent stocks.

Year-to-date, here are the returns for the top 5 largest positions within $ARKK, which is down -54% on the aggregate:

Tesla Inc. $TSLA: -27%

Roku Inc. $ROKU: -57%

Zoom Video Communications $ZM: -48%

Exact Sciences Corp. $EXAS: -32%

Block Inc. $SQ: -48%

The financial markets have seemingly shrugged off the geopolitical conflict in Ukraine; however, these dynamics are still impacting commodity markets significantly. I’ve been relatively bullish on energy & commodity-related stocks prior to the onset of the Russia/Ukraine conflict, largely due to the inflationary environment. However, with broad market pressure putting cracks in all sectors and industries, I think oil & gas stocks might have increasingly high levels of volatility in the near future. I am not looking to build positions in these sectors, and I think investors who already have exposure in them will benefit from sitting tight.

Defensive sectors that provided a safe-haven for investors in Q1 2022 have been deteriorating in Q2. Utilities ($XLU), industrials ($XLI), consumer staples ($XLP), and basic materials ($XLB) stocks are all negative now on a YTD basis, though are generally outperforming the broader indexes.

From my perspective, current market dynamics are making it difficult to be attracted to any stock over the short-run. However, the ongoing market consolidation and bear market in technology stocks is providing long-term investors with extremely attractive entry points, particularly if they are able & willing to stomach short-term downside.

Most notably, mega-cap technology stocks are trading at substantial discounts. For example, here are the 52-week high drawdowns for key stocks:

$AAPL: -19.5%

$MSFT: -25.1%

$GOOGL: -23.3%

$AMZN: -39.9%

$NVDA: -48.7%

Cumulatively, these stocks have lost hundreds of billions of dollars in market capitalization, without fundamental changes to their businesses, cash flows, or dividends. Markets can act rationally and irrationally, both to the upside and to the downside. At the present moment, I feel that there are pockets of downside irrationality that are providing long-term investors with rational opportunities to buy equity in great companies.

As always, more downside is possible! In fact, I think it’s probable based on analysis I’ve shared with premium members. However, long-term investors who can maintain their conviction and handle short-term downside should be even more opportunistic if prices continue to decline.

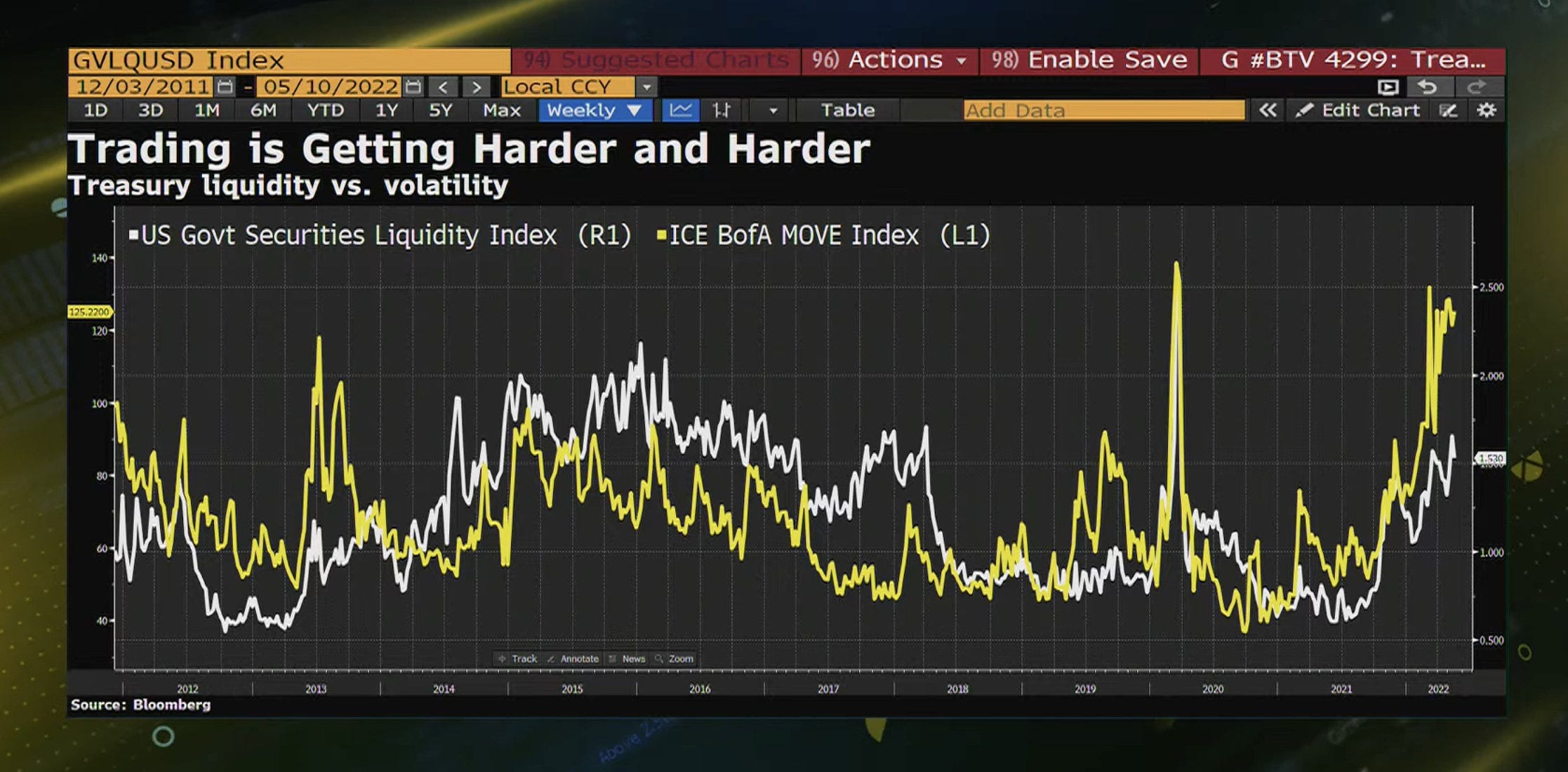

I expect for volatility to remain elevated in the current monetary policy environment, wherein markets will be choppy and reflect the downside risks of negative investor sentiment. The CBOE Volatility Index, the $VIX, looks poised for an explosive move at some point in the near future. This rounding bottom shape, paired with the resistance trendline, is setting up for a a breakout extension if/when it is able to break above the red trendline.

If this breakout occurs, it will be indicative of a further deterioration in risk assets. With an ongoing reduction of global central bank balance sheets, this will continue to drain liquidity out of the financial system, therefore bringing higher volatility into the markets. Quite simply, there’s a clear correlation between liquidity and volatility:

This gives us an excellent framework in order to set expectations:

Monetary Tightening ↑

Yields ↑

Central Bank Balance Sheets ↓

Liquidity ↓

Volatility ↑

Asset Prices (notably high risk assets) ↓

Investor Sentiment ↓

At the present moment, this line of logic is my base-case for financial markets until we see a material change in the inflationary dynamics and monetary policy environment.

I also expect to see inflationary pressures resume to the upside. Commercial banking data that I’ve reviewed suggests that commercial & industrial loans, a subset of total loans & leases, are on the rise. This will bring more money out of the financial system and into the real economy, likely pushing inflation higher as the Fed’s newly printed money continues to enter the economic system. With more money chasing the same amount of goods & services, the price of goods & services will rise in order to accommodate the increase in the instrument of exchange: U.S. dollars.

This is actually a scenario that I outlined in February, predicting that higher interest rates from the Fed could stimulate banks to increase lending activity in an environment of relatively loose lending conditions. The increased lending activity would therefore increase the velocity of money, increasing inflationary pressures in the economic system:

Over the three months since posting this analysis, a lengthy thread on commercial banking data, markets have evolved in accordance to the prediction I laid out. If the data continues to evolve as I suspect it will, we’ll see higher inflation in the U.S. (and likely globally). This will cause the Federal Reserve to become increasingly aggressive in their monetary policy actions & rhetoric, therefore causing interest rates to rise even further and put more downside pressure on the present value of assets.

This is why I believe patience will be a critical feature of success in financial markets for the remainder of 2022. I don’t believe there is a need to aggressively dollar-cost average, or try to go “all-in” on certain investments. Risk management will continue to be a core component of my investment strategy for the remainder of the year, using rallies to shift portfolio allocations into core positions.

Over the coming weeks, I’ll be sharing the core stocks & ETF’s I’m focused on, which will be exclusive for premium members. If you’re not already a member for the exclusive research I share with premium members, please take advantage of the 7 day free trial below.

If you’re not happy with the quality of the research, you’ll have the ability to cancel the subscription, risk free.

In closing, recent market conditions have been extremely difficult. The views that I shared above aren’t very optimistic for short-term dynamics, and I do expect to see these difficult conditions persist. However, these difficult times will produce long-term winners and short-term losers. Investors who can frame the market environment in this bifurcated framework while maintaining a patient dollar-cost averaging strategy into stocks and crypto are likely poised for great long-term success. This isn’t a sexy or exciting approach to investing, but it’s a tried & true method of the best investors to have ever lived. In the game of investing, you don’t win brownie points for excitement, pizazz, or flashy strategies. The only thing that matters is compounding returns.

As such, I think long-term investors should celebrate the opportunity that the markets are giving us right now, understanding that things can get worse but will eventually improve.

Caleb Franzen

DISCLAIMER:

My investment thesis, risk appetite, and time frames are strictly my own and are significantly different than that of my readership. As such, the investments & stocks covered in this publication are not to be considered investment advice and should be regarded as information only. I encourage everyone to conduct their own due diligence, understand the risks associated with any information that is reviewed, and to recognize that my investment approach is not necessarily suitable for your specific portfolio & investing needs. Please consult a registered & licensed financial advisor for any topics related to your portfolio, exercise strong risk controls, and understand that I have no responsibility for any gains or losses incurred in your portfolio.