Investors,

Market conditions continued to deteriorate this week, prompted by heightened inflationary pressures. In last week’s report, Edition #157, I discussed how “market participants are starting to fold their hands with the intention of revisiting the markets once things have calmed down.” I’m starting to refer to this dynamic as “enthusiasm capitulation”. When market psychology is currently dominated by fear, any negative news becomes a catalyst for additional selling pressure. That’s where we are right now.

After 20+ months of a raging bull market, the market is simply digesting the exuberance and gains that we’ve been experiencing. There are three return metrics that I want to focus on: Returns since ATH’s, 2022 YTD returns, last week’s returns.

Returns since ATH’s:

Dow Jones: -10.8%

S&P 500: -12.7%

Nasdaq-100: -20.6%

2022 YTD returns:

Dow Jones: -9.3%

S&P 500: -11.8%

Nasdaq-100: -18.5%

Last week’s returns:

Dow Jones: -2%

S&P 500: -2.9%

Nasdaq-100: -3.9%

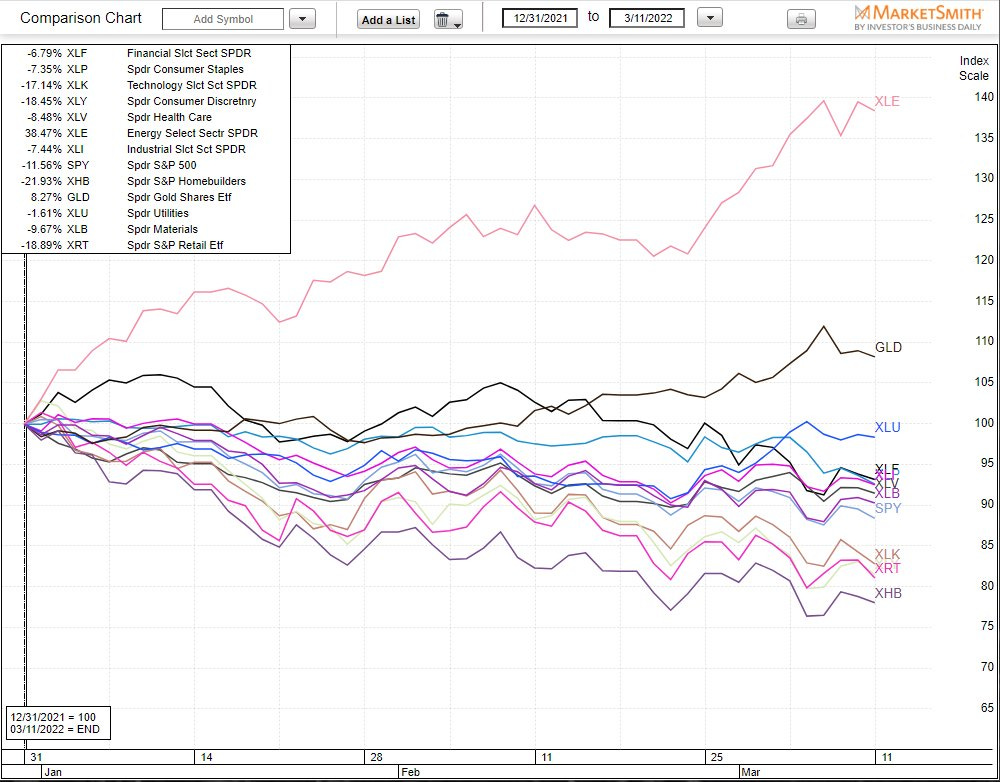

The financial services company State Street Global Advisors offers a variety of sector ETF’s, and we can see the YTD returns for each of these funds below:

Energy ($XLE) and gold ($GLD) are the only two that have a positive YTD return. This is happening for two reasons:

Inflation is creating tailwinds for commodity prices, therefore oil & precious metals are rising in this environment.

Market fear is creating a rush to safety, causing investors to sell high risk assets and rotate into risk-less assets. This is directly benefitting the U.S. dollar and gold.

Normally, U.S. Treasuries would be included in the second group as a beneficiary of investors rushing to safety; however, 40-year record levels of inflation and a shift in the Fed’s monetary policy are causing rates to rise at a historic rate. This consistent rise in rates puts pressure on the present value of Treasury securities, resulting in bond funds falling in 2022. $TLT, the 20+ year Treasury ETF, is currently down -9% in 2022, while the fund was “only” down -6% in 2021.

The reason why I’m bringing this up is to highlight how difficult it’s been to navigate the market over the past several months.

As of March 11th, the advance/decline (A/D) line of the Nasdaq hit its lowest level since 2016. The daily A/D line measures the difference between the number of stocks rising vs. falling.

Again, this confirms how extremely difficult market conditions have been — it wasn’t even this bad in February/March 2020!

If we look at the S&P 500, I wanted to update some analysis I had previously shared in mid-February on Twitter. Here’s the S&P 500 since 2012, using weekly candles in logarithmic scale:

In the original analysis I shared in February, I pointed out how the 55-week moving average (teal) has generally acted as a strong level of support. When it fails to act as support, price has continued to fall towards to the 200-week moving average (blue). We can see that the 55-week EMA failed to act as support in 2015/2016, and again in 2018. Both of these occurrences are outlined in red rectangles. Additionally, the COVID crash also sliced through the 55-week EMA and the 200-week EMA, though it’s worth noting that provided investors an amazing buying opportunity.

With this knowledge at our disposal, what can we extrapolate about the current circumstances? We officially had a weekly close below the 55-week EMA for the first time since COVID. Based on this 10-year analysis, the S&P 500 has fallen to the 200-week EMA after falling below the 55-week EMA.

In the 2015/2016 case, it took 22 weeks for the S&P 500 to retest the 200 EMA after closing below the 55 EMA. The ride was choppy, but fell an additional -8% until it officially rebounded on the 200-week EMA.

In the 2018 case, it took 9 weeks for the S&P 500 to retest the 200 EMA after closing below the 55 EMA. The index fell an additional -11.7% after breaking below the 55-week EMA, rebounding almost perfectly on the 200 EMA.

In the current situation, the S&P 500 would need to fall -15% in order to retest the 200-week EMA. Of course, this will adjust over the coming weeks as the EMA continues to evolve based on the future price action of the index. Therefore, I reasonably think the S&P 500 could fall an additional -10% to -13% over the next 4-20 weeks.

Throughout this newsletter, I’ve been consistently bullish on U.S. equities. In November 2021, I shifted bearish on non-profitable tech & growth stocks; however, this is the first time where I’m officially short-term bearish on the broader market. Genuinely, I hope I’m wrong. Over the long-run, I think this will provide an excellent buying opportunity, and I don’t think investors should be running to the exit doors right now. For over a month, I’ve been highlighting two key investment opportunities in the short-run:

Oil & gas services ($OIH)

Shipping & container stocks ($ZIM, $SBLK, $SB, $NMM, $GSL, $MATX, $DSX)

Let’s address some of my prior research, starting with oil & gas services. On February 13th, I published Edition #151 and shared the following chart:

“I’d like to own oil & gas stocks if they can hold above the upper-bound grey zone.”

Since publishing that research on 2/13/22, here’s how the oil services ETF has performed:

To perfection, price used the grey range as intermediary support before achieving the final breakout extension. Since 2/13, shares have gained +17%.

Switching to my prior research on shipping & container stocks, here’s how each of the stocks have performed since I first highlighted them on February 7th:

$ZIM +14.2%

$SBLK +26.4%

$SB +28.3%

$NMM +19.8%

$GSL +8.6%

$MATX +20.3%

$DSX +31.5%

Recall, I reiterated my bullishness on this sector on February 27th. All except $SBLK and $MATX have risen since 2/27. I’m still bullish.

Talk soon,

Caleb Franzen

DISCLAIMER:

My investment thesis, risk appetite, and time frames are strictly my own and are significantly different than that of my readership. As such, the investments & stocks covered in this publication are not to be considered investment advice and should be regarded as information only. I encourage everyone to conduct their own due diligence, understand the risks associated with any information that is reviewed, and to recognize that my investment approach is not necessarily suitable for your specific portfolio & investing needs. Please consult a registered & licensed financial advisor for any topics related to your portfolio, exercise strong risk controls, and understand that I have no responsibility for any gains or losses incurred in your portfolio.