Investors,

In 2020, the United States spent over $10 billion USD of taxpayer money on Public Private Partnerships (P3’s) - a trend that’s expected to strengthen in the U.S. and countless other parts of the world in the coming years, according to industry experts. Despite the P3 sector accounting for hundreds of millions of dollars in transactions annually, this monolithic asset class has been hidden from the general public – meanwhile, a small handful of policymakers, private companies, and ultra-high net worth individuals have benefited from these lucrative, government-backed, and tax-advantaged P3 deals.

That’s why I’m excited to announce a new, exclusive promotion for my readers, brought to you by DeltaP3, a decentralized investment platform, bringing the previously hidden world of P3 investing to retail investors everywhere. They are backed by and built on Avalanche – the fastest growing blockchain protocol on the market. DeltaP3 is offering an exclusive discount for my readers and it only takes two easy steps to qualify:

1. Visit https://deltap3.org/caleb/

2. Sign up for the DeltaP3 email list to ensure you’re notified as soon as they are fully live.

The best part? When you sign up using my promo link, you’ll receive a welcome email & discount code for 20% off a (month/year) subscription to my premium content. You’ll also be notified and invited to exclusive virtual/in-person events with me, the DeltaP3 team, and some of the biggest players in the P3 space, ranging from high-ranking government officials to infrastructure investing heavyweights.

DeltaP3 is the only blockchain-native platform offering widespread access to the hottest deals in the P3 market. Check them out at https://deltap3.org/caleb/ to cement your seat at the P3 Investment table AND get 20% off a (month/year) to my premium content.

Aside from signing up for the DeltaP3 email list, I’d encourage you to watch this short segment from a full video about how traditional P3’s are highly exclusive and lack transparency, leading to certain inefficiencies:

DeltaP3 is turning this investment class on its head through blockchain technology, and I’m beyond excited to announce my first ever partnership with them!

Economy:

The “transitory” inflation narrative just received the final nail in the coffin. It’s been dead for months, but it’s now irresponsible to question whether or not inflation has become persistent. It has. What started out as a temporary but modest increase in inflation has now turned into an outright dilemma for monetary policymakers. The year-over-year inflation rate has risen every month since the increase from August 2021 to September 2021.

The February 2022 CPI data was released on Thursday morning, reflecting a 12-month inflation rate of +7.9% for consumer prices. For context, the January 2022 data showed a +7.5% increase. In the last six months alone, the 12-month inflation rate has consistently gained momentum: +5.4%, +6.2%, +6.8%, +7.0%, +7.5%, +7.9%.

The core CPI, which excludes food & energy prices, increased annually at +6.4% in February 2022 vs. +6.0% in January 2022. When we look at the chart above, we can see how the core CPI has generally remained stable even during periods when the headline CPI data swings up & down. What’s unique about the current circumstances is that we’re experiencing a simultaneous and rapid acceleration in both the headline and core CPI data. Quite simply, inflation is unavoidable and unrelenting.

Unsurprisingly, government officials continue to deflect any and all responsibility for the inflation dilemma. On November 11, 2021, I published Edition #118 to specifically focus on inflation dynamics. I highlighted the irresponsible remarks of Treasury Secretary, Janet Yellen, who has consistently been incorrect about inflation.

Once again, policymakers, Fed officials, and bureaucrats continue to lose their credibility and deflect any blame for inflation. On Friday, President Biden said: “make no mistake, inflation is largely the fault of Putin”. This has to be one of the most ludicrous statements I’ve heard in 2022! Let me explain why…

While markets are forward-looking indicators, and commodity markets could have been pricing-in the impact of Russia’s invasion prior to the actual event, here are some important timelines:

February 21, 2022: Putin recognizes the independence of the Donetsk and Luhansk, two separatist regions that comprise the Donbas.

February 24, 2022: Russia officially invades Ukraine & initiates war.

February 24, 2022: The U.S. announces the first sanctions on Russia.

February 26, 2022: The U.S., EU, Canada, and UK ban certain Russian banks from the SWIFT payment system.

Let’s track crude oil prices through these events.

2/1/2022: Crude oil settled at $88.36, up +17% since the start of the year.

2/24/2022: Crude oil settled at $93.00, up +5.25% since the start of February.

2/28/2022 (the final trading day of the month): Crude oil settled at $95.82, up +8.7% for the month of February.

Biden is stating that the +7.9% rise in consumer prices is being caused by Putin, even though the major economic events happened in the final days of the month? While the geopolitical conflict has given commodity prices a boost, it’s irresponsible and/or misguided to blame the U.S. CPI data on global events that happened at the end of the month. Politicians and policymakers are always the first to deflect blame on external factors in order to save face and minimize responsibility. This is exactly what I said was happening in Edition #118 in November, while citing the following chart:

“Oddly enough, central bankers and government officials are quick to blame the sustained acceleration in inflation on everything other than the fact of central bank activity, monetary policy & fiscal spending.”

Where’s the credibility?

First they said there wouldn’t be inflation. Then they said it would be transitory. Then they blamed it on base effects from deflation in mid-2020. Then they blamed it on supply bottlenecks. Then they blamed it on greed and profiteering. Then they blamed it on oil prices. Now they blame it on Russia.

There’s a complete lack of self-awareness to acknowledge that the fiscal & monetary policy decisions of the past 24 months have at least contributed to the inflation predicament.

Since January 2021, in the midst of historic inflation, the Federal Reserve’s balance sheet has increased from $7,363,351 million ($7.363Tn) to $8.910Tn as of 3/9/22, or +21%. The amount of money in circulation, M2 money supply, has increased by +14% during the same time period. Additionally, M2 has increased by +41.7% since January 2020. The monetary system has been primed for record levels of inflation.

Can it be stopped? Certainly, but the problem is becoming increasingly more complex. The longer inflation remains above the historical trend, roughly 2% to 3%, the more rooted it will become in consumers’ expectations, therefore making it more persistent. The opportunity to get in front of inflation and actively suppress rising prices has already sailed past the Federal Reserve. They are unprecedentedly behind the curve, as evidenced by the wide margin between the 2-year yield and the effective federal funds rate. These variables have a tight correlation, generally moving in a consistent direction; however, the recent rise in 2-year yields has been unaccompanied by the federal funds rate.

As we’ve discussed in the past, inflation and yields are positively correlated. Because inflation reduces the purchasing power of the currency, future fixed income payments from the bond become worth less. As such, bond investors won’t accept a low yield during an inflationary period. In order to attract bond investors, debt issuers must offer a higher yield on the debt in order to make an agreement between both parties. Therefore, as inflation rises, bond yields rise.

Additionally, if a potential bond investor believes that inflation will get worse in the future (aka inflation expectations rise), they will believe that the bond carries more risk. In order to compensate for that additional risk, the investor commands a higher yield in order to make a deal. Again, this confirms that inflation and inflation expectations cause yields to rise.

Watching short-term bond yields, like the 2-year Treasury yield, is ideal for how investors and consumers are viewing these inflation dynamics. Yields plummeted in Q1 2020 as a result of the monetary policy response to COVID, but have been able to erase all of those losses in a bizarre U-shape.

2-year Treasury yields have experienced a monumental rise from 0.106% to the current level of 1.75%, reflecting optimism for U.S. growth and concerns around inflation. Because inflationary pressures have continued to rise despite the Federal Reserve’s rhetoric that they’re going to fight inflation, the bond market has been telling us three things:

Inflationary pressures will rise.

Inflation will be difficult to defeat.

The Fed’s policies aren’t going to be as effective as they think.

Stock Market:

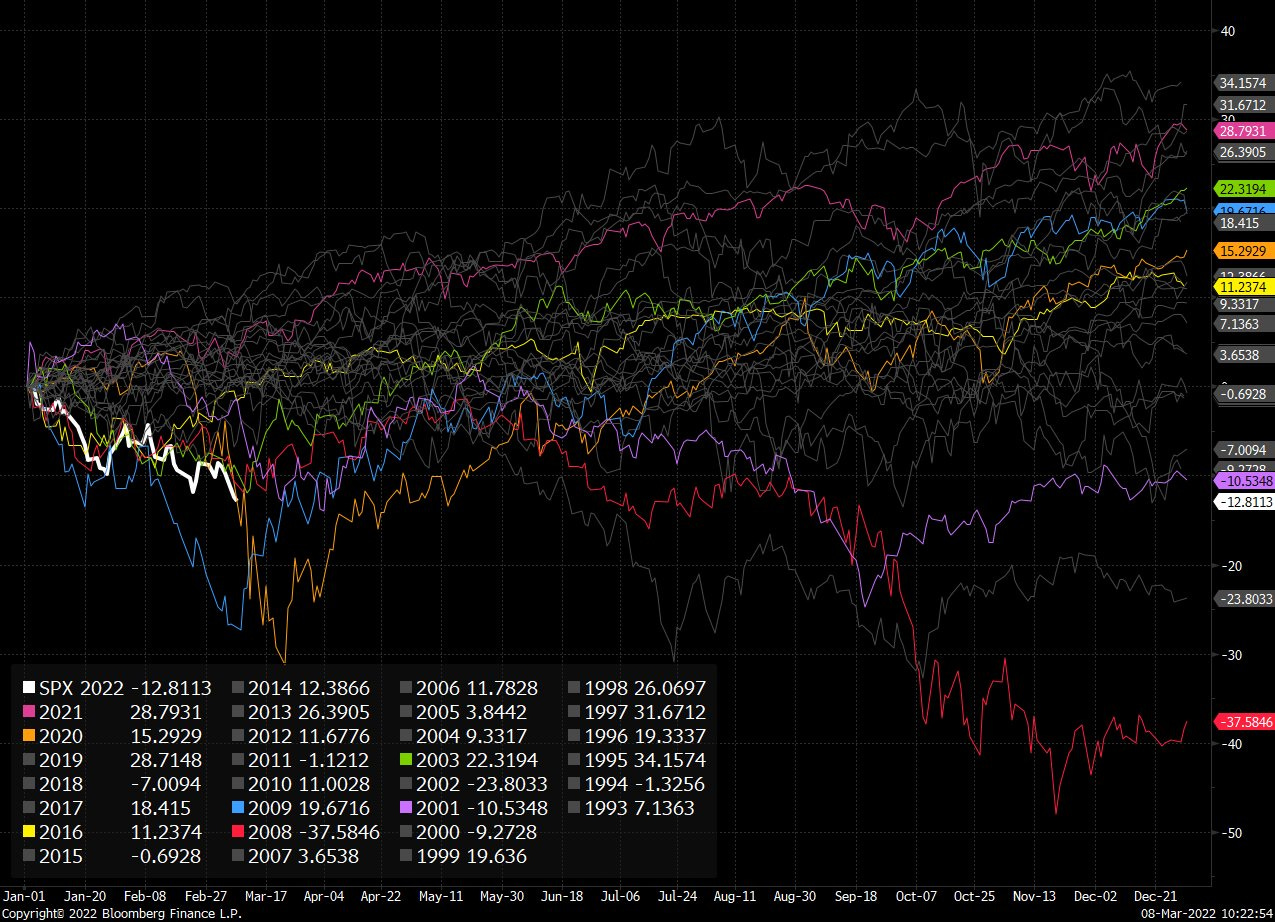

U.S. stocks continue to exhibit non-optimistic behavior. In January, I shared the following chart about the S&P 500, which got featured as “Chart of the Day” by the Chart Report:

My analysis at the time was,

“A key way to define a bull market is the creation of higher highs and higher lows. A bull market looks like the silhouette of a staircase.

Since the COVID lows, we've unquestionably been in a bull market & have yet to make a lower low.

This trend is currently being threatened.”

What has the S&P 500 done since? It has whipsawed around dramatically and continues to display signs of weakness around the yellow level that I originally highlighted.

In this updated chart I’ve been sharing for the past few weeks, we can see that the market has repeatedly tried to rebound on this yellow level. However, it seems to have gotten weaker the more we retest it, producing lower highs and lower lows so far in 2022. This short-term trend is outlined by the red channel.

The weekly close was a worst-case scenario for bulls, as we officially closed below the yellow range for the first time since June 2021. This upcoming week, it’s vital for the S&P 500 to remain above the white trendline I have outlined on this chart. This has been short-term support since 2/24/22; therefore a breakdown below this range could imply that bulls have forfeited the tug-of-war.

It’s also worth noting that returns in 2022 have been historically bad so far, as evidenced by this chart from Michael McDonough:

Only 2009 and 2020 have had worse starts in the past 30 years. In order to be successful in this market, I think investors need to maintain a long-term mindset and stay patient. We’re clearly not in the goldilocks times of 2020-2021, as we’re undergoing a sizable shift in monetary policy, decelerating economic growth, global conflict, accelerating commodity prices, rising inflation, and no apparent catalysts for economic growth or rising corporate profits.

This isn’t doom and gloom, but should be a welcomed opportunity to reset expectations, understand what’s driving markets, return to fundamentals, and build long-term convictions. I remain optimistic on U.S. stocks, but think that short-term dynamics will create additional turbulence. The way I see it, short-term pain equals long-term gain.

Bitcoin:

My approach to Bitcoin remains consistent and I’m still extraordinarily bullish on the investment opportunity in this asset. It feels like enthusiasm within the entire crypto ecosystem has capitulated, yet the price of Bitcoin continues to chop around $40k. While non-Bitcoin investors may scoff at the -42% drawdown from ATH’s, it’s important to recognize a few things:

18 months ago, the price of Bitcoin was $10,000.

24 months ago, the price of BTC was $7,800.

36 months ago, the price was $3,800.

5 years ago, the price was $1,200.

If we could teleport back to each time period and tell people that Bitcoin would be trading at $40k, they’d be shocked. The last thing on their mind would be to question how much of a drawdown BTC experienced to get to $40k, they’d simply be focused on the fact that we got to $40k! Instead, we’re currently at $40k and retail investors have non-existent levels of enthusiasm. Investor psychology is a funny thing.

Here’s my personal chart of Bitcoin and the key levels I’ve been monitoring, going back to January 2019:

Based on this chart, we’re clearly in an extensive consolidation zone. We have well-defined levels of support & resistance, with multiple confirmations at the upper and lower-bound. I still believe we’ll see price above $60k in 2022.

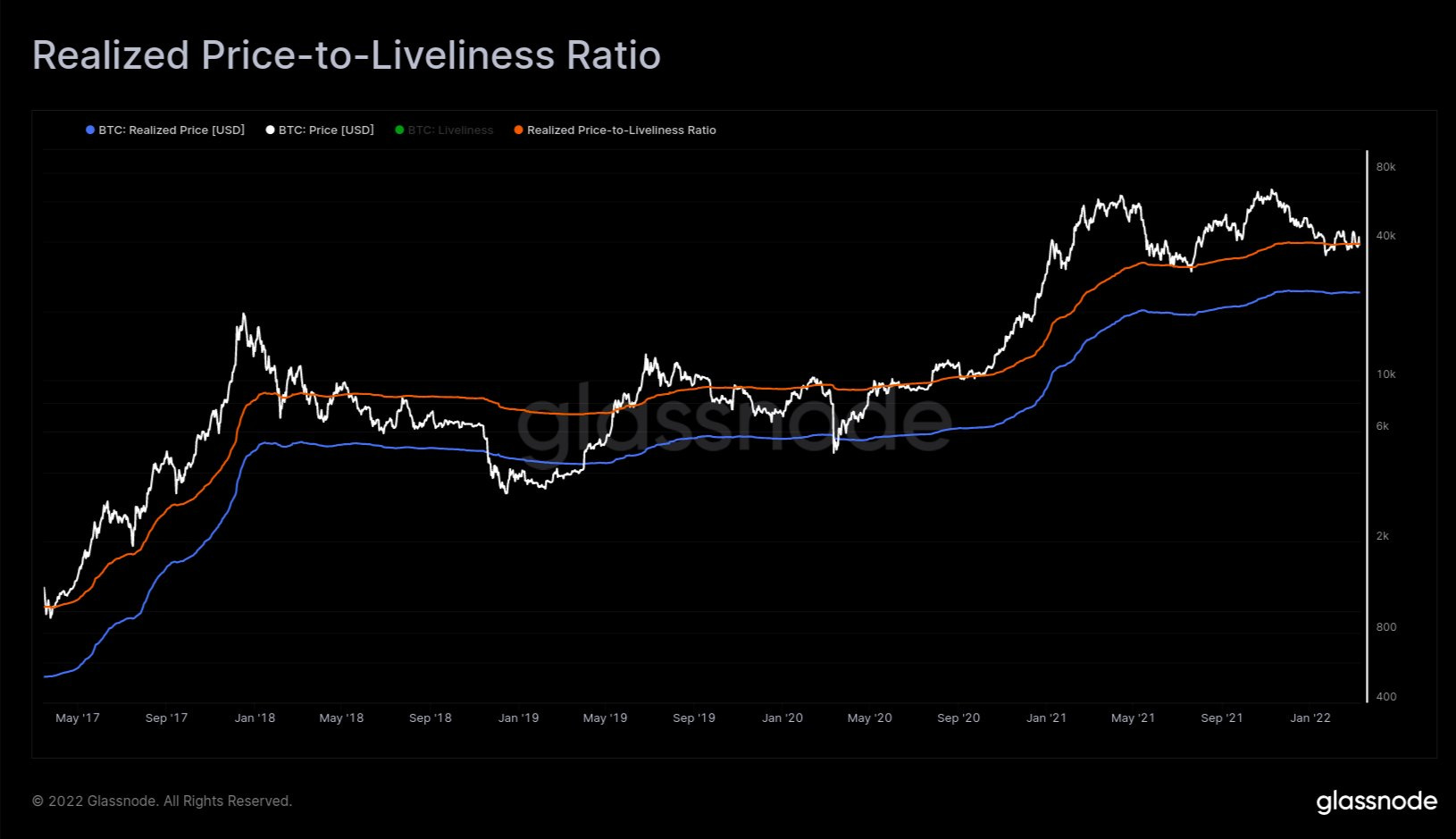

I saw this excellent chart from the lead on-chain analyst at Glassnode, Checkmate, that highlighted some interesting dynamics for Bitcoin.

This chart monitors two important variables:

Realized Price: This is calculated by measuring “realized market cap”, the aggregate price at which point all Bitcoin were last transacted on-chain, then dividing by the current supply. Realized price is a valuable metric because it provides a sticker version of market price. A Bitcoin purchased at $500 has a realized price of $500 until then next time it is transacted, even though the market price of that Bitcoin will fluctuate minute by minute.

Realized Price/Liveliness: Liveliness is a slightly confusing metric, so I’ll simply refer you to Glassnode directly where they provide an excellent summary and breakdown of this data point. They explain it far better than I can in a few sentences.

Nonetheless, these data points show us something interesting when overlaid on top of Bitcoin’s market price. Since mid-2017, a dip below the Realized Price/Liveliness band has provided long-term investors a decently attractive entry point. When market price has fallen below Realized Price, as it did in December 2018 and March 2020, this has provided long-term investors an outstanding entry point.

Currently, the market price of Bitcoin has been bouncing around the Realized Price/Liveliness band. Could price fall further? Absolutely. Do I think the risk/reward of Bitcoin is personally attractive when trading between these two bands? Absolutely.

I know this was a lengthy newsletter, so you’re an absolute rockstar if you made it all the way through!

Talk soon,

Caleb Franzen

DISCLAIMER:

My investment thesis, risk appetite, and time frames are strictly my own and are significantly different than that of my readership. As such, the investments & stocks covered in this publication are not to be considered investment advice and should be regarded as information only. I encourage everyone to conduct their own due diligence, understand the risks associated with any information that is reviewed, and to recognize that my investment approach is not necessarily suitable for your specific portfolio & investing needs. Please consult a registered & licensed financial advisor for any topics related to your portfolio, exercise strong risk controls, and understand that I have no responsibility for any gains or losses incurred in your portfolio.