Edition #157

Navigating Uncertainty

Investors,

Markets are continuing to evolve in surprising ways. It feels like global macro conditions are changing on a daily basis, with substantial impacts on literally every single asset class. Markets are behaving both rationally and irrationally, creating hypocritical conclusions and theories about why certain assets are behaving in a certain way. We’re being inundated with frightening headlines of war and the potential of an economic downturn, creating a general sense of panic and heightened uncertainty. Markets have been facing consistent pressure since November 2021, but have almost exclusively been falling lower in 2022. While the S&P 500 has fallen -10.2% from the all-time highs on 1/4/2022, it feels as if investors are withdrawing from the market. Seemingly, investors need to be experts in monetary policy, geopolitical conflict, global trade, public health & safety, inflation, and commodity dynamics in order to be successful in this market. That’s a tall task, and I’m getting the sense that market participants are starting to fold their hands with the intention of revisiting the markets once things have calmed down.

In this special report, I’ll provide an in-depth breakdown of how we got here, how I’m viewing financial market conditions, and how I expect to see markets evolve in the coming months. I’m seeing market pundits on financial media and analysts on Twitter spouting nonsense and contradicting themselves in multiple ways; therefore, I’m confident this report will act as a sufficient north star.

I’ll predominantly be focused on three core topics:

U.S. monetary policy.

Risk assets.

Commodities.

How We Got Here:

Financial markets have been a mess since November 2021, which should come as no surprise to students of monetary policy. While financial markets are a forward-looking indicator, the Federal Reserve’s November announcement to begin tapering their asset purchases signaled an official shift in the monetary policy environment. The markets knew this announcement was coming and had already began to price in higher rates, but the official announcement has created massive tailwinds for rates to rise further.

The Fed’s announcement took place on November 3rd, 2021 and almost perfectly signaled the top of the market. The S&P 500 closed at $4,660.57 on 11/3/2021 and had an all-time high daily close of $4,796.56 on 1/4/2022, indicating that the S&P 500 only gained +2.95% after the Fed’s tapering announcement. In the chart below, we’re looking at the S&P 500 since January 2020 and highlighting the tapering announcement in teal. I’ve been sharing this chart on Twitter since mid-January:

This wasn’t exclusive to the stock market, as Bitcoin also peaked shortly after the Fed’s announcement. Because the mainstream belief is that Bitcoin is riskier than U.S. stocks, the peak for Bitcoin happened much faster than it did for stocks. Bitcoin peaked at $69,000 on November 9th, less than one week after the Fed’s announcement.

Mechanically, why was the taper announcement so impactful on risk assets? The simplest answer is often the most appropriate, which leads me to providing the following solution: yields and interest rates have risen substantially since 11/3/2021.

On 11/3/2021, the yield on the 2-year Treasury was 0.478%. As of 3/4/2022, the 2-year Treasury yield is 1.49%. While this may seem like a marginal increase, rising “only” 1.012 percentage points, yields have practically tripled over a three-month period. This massive acceleration and rate of change has significant impacts on all assets and financial markets.

Why has this acceleration happened so swiftly? There are two reasons:

• First of all, the Fed’s shift to taper their asset purchases is the primary driver for rising yields. When the Fed reduces its purchases of Treasuries, demand for Treasuries falls! In response to reduced demand, yields rise in order to attract and incentivize investors to buy the debt. Considering that the Fed was buying at least $80Bn/month of U.S. Treasuries for 18+ months, they were providing an extremely significant level of demand in this market. As that demand fell, bond yields rose.

• Secondly, inflation has continued to gain momentum after the Fed’s tapering announcement. At the time of their announcement, the most recent inflation data was for September 2021, in which the 12-month inflation rate was +5.4% for the CPI. In the coming months, the 12-month inflation rate for each month was 6.2%, 6.8%, 7.0%, and 7.5%, ending January 2022. The February 2022 CPI is scheduled for release on March 10th, with median estimates currently at +7.8%. The market believes inflationary pressures will persist and continue to increase.

In response to accelerating inflation, financial markets have expected the Federal Reserve to act even stronger than we initially anticipated in November. Market theory tells us that yields and inflation are positively correlated, meaning an increase in inflation will produce a similar increase in yields. The consistent rise of inflation has created tailwinds for yields to rise faster, in addition to the the Fed’s reduced asset purchases.

These two dynamics are the sole reason for rising yields.

As we know, yields and asset prices typically have an inverse correlation. Therefore, rising yields have prompted asset prices to move lower, putting the most pressure on the riskiest assets like stocks and crypto. In total, here’s the framework:

Inflation ↑ Yields ↑ Asset Prices ↓

Inflation ↓ Yields ↓ Asset Prices ↑

These unquestionable dynamics are why I pay such acute attention to the economic environment and monetary policy. Inflation data and labor market data have a direct impact on monetary policy, which directly impacts yields, which directly impacts asset prices.

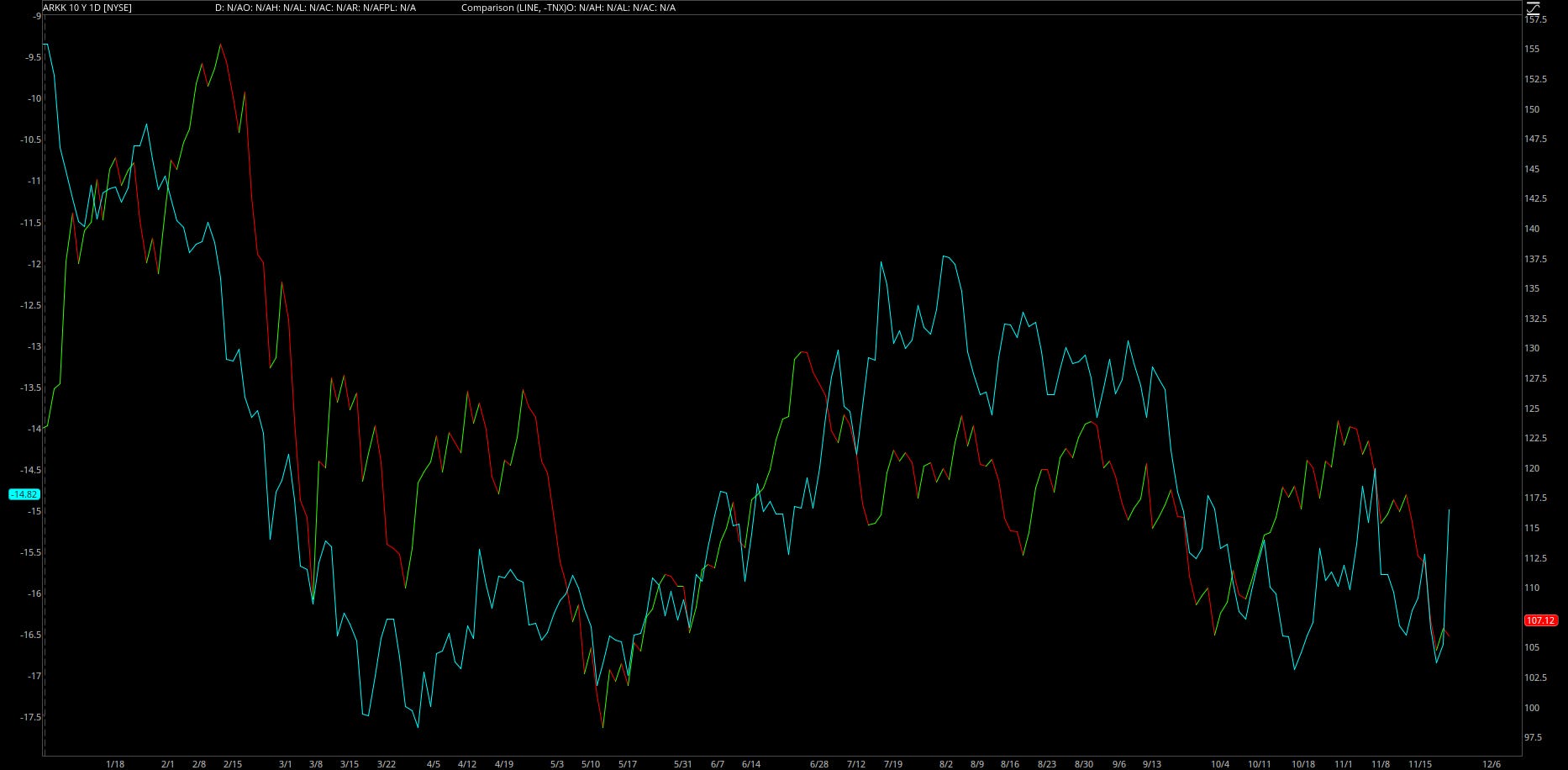

Because I understood these dynamics, I wrote “Edition #127: A Deep-Dive on Equity Prices, Rates, and Asset Returns”, where I formally warned against investing in tech/growth. I particularly warned against non-profitable tech/growth stocks, using $ARKK as a proxy, due to the rising-rate environment. As a way to highlight the inverse relationship between risk assets and yields, I inverted the 10-year Treasury yield and overlayed it on top of $ARKK’s chart.

The perfect correlation we see in this chart shows that the two variables are inversely correlated, a vital relationship to understand in any market. In that publication, I said:

“As an investor with a time horizon of 3-12 months, I’d be extremely wary to get invested in unprofitable tech/growth stocks barring any material outlook in the trajectory of rates going forward. Based on what we know right now, it appears that the path of least resistance for rates is to gradually rise higher.”

What’s happened since I shared this outlook? $ARKK has fallen -43.8%. The correlation between $ARKK and inverted 10-year yields has remained intact, reflecting that yields are rising while $ARKK is plummeting. Rising yields create a risk-off environment, signaling to investors that they should adjust their portfolios.

You’ll notice that the correlation got weaker in the past few weeks… why has this been the case?

Geopolitical risks in Ukraine have exacerbated the risk-off environment. In times of heightened uncertainty, global investors dramatically reduce their exposure to risk assets and increase their exposure to the U.S. dollar and to future U.S. dollars (aka Treasuries). When the demand for Treasuries rises, the yield on Treasuries falls. Russia’s invasion of Ukraine has produced a massive rush to safety, dramatically increasing the demand for the USD and Treasuries and decreasing the demand for risk-assets like $ARKK.

This brings us to an interesting inflection point: yields are rising because of rising inflation and because the Federal Reserve is tightening monetary policy; however, yields are falling because of geopolitical conflict and uncertainty. This tug-of-war is causing heightened volatility in the market, shifting the attention of investors between monetary policy, inflation, and Ukraine/Russia. On any given day, new developments on either topic dominate financial news.

The fact is, both variables (rising interest rates and geopolitical conflict) cause volatility to rise. It’s no wonder that the CBOE Market Volatility Index ($VIX) bottomed on 11/3/2021 and has been moving higher ever since. The VIX has gained +113% since the market-close on 11/3/21!

The market has been and will continue to grapple with these two dynamics, which aren’t likely to subside. While the geopolitical conflict may cause the Federal Reserve to pump the brakes on their rate-hike schedule, they seem fully committed to raising rates in March 2022 in order to combat inflation. So long as they remain committed to fighting inflation, their actions will create tailwinds for rates to rise. On the other hand, investors hate conflict and uncertainty, leading them to sell their risky assets and rotate into safer assets. This will create tailwinds for rates to fall, due to the increased demand for U.S. Treasuries.

In either scenario, this is bad news for risk-assets. The only way risk-assets will perform well is if there is a massive shift in monetary policy, in which the Federal Reserve acknowledges that the Ukraine/Russia situation is substantially increasing the likelihood of a global recession, and therefore prompting them to keep interest rates low. This would require the Fed to formally acknowledge that they will not be fighting inflation, putting the onus on U.S. consumers to weather the storm as the Fed continues to stimulate the economy & financial markets.

At the present moment, I think this likelihood is very small. While several Fed officials have cited heightened uncertainty of global economic conditions as a result of the Ukraine/Russia conflict, the Fed has firmly reassured that they are committed to fighting inflation. Jerome Powell gave his semi-annual monetary policy report earlier this week, in which his opening remarks were extremely informative. Powell cited an “extremely tight” labor market and high levels of persistent inflation. In essence, the conditions to tighten monetary policy are firmly in place and it would take a significant turn of events for the data to deteriorate and force the Fed to provide monetary stimulus. While it’s possible for the Ukraine/Russia conflict to spiral out of control and create a global economic slowdown, I can’t speculate on how extensive that impact will be.

Where I Think We’re Going:

I’m going to keep this direct: I think bond yields will resume their upward momentum, despite the recent dip as a result of the Ukraine/Russia conflict. My belief is that inflation will continue to accelerate and remain elevated for the remainder of 2022 (likely above 5% on a trailing twelve-month basis). Additionally, my number one rule is don’t fight the Federal Reserve. At the present moment, the Federal Reserve is committed to ending their asset purchases and raising interest rates. Rising/persistent inflation, a strong labor market, and monetary tightening are likely to push yields higher.

First of all, let’s address inflation. I’ve been on record since May 2021 that inflation will reach 7% to 10%. At the time I made that prediction, the inflation rate was +4.2%. The most recent two months have achieved my target prediction, reaching 7.0% and 7.5%. I still think there is room to rise further, despite what many economists and analysts are predicting.

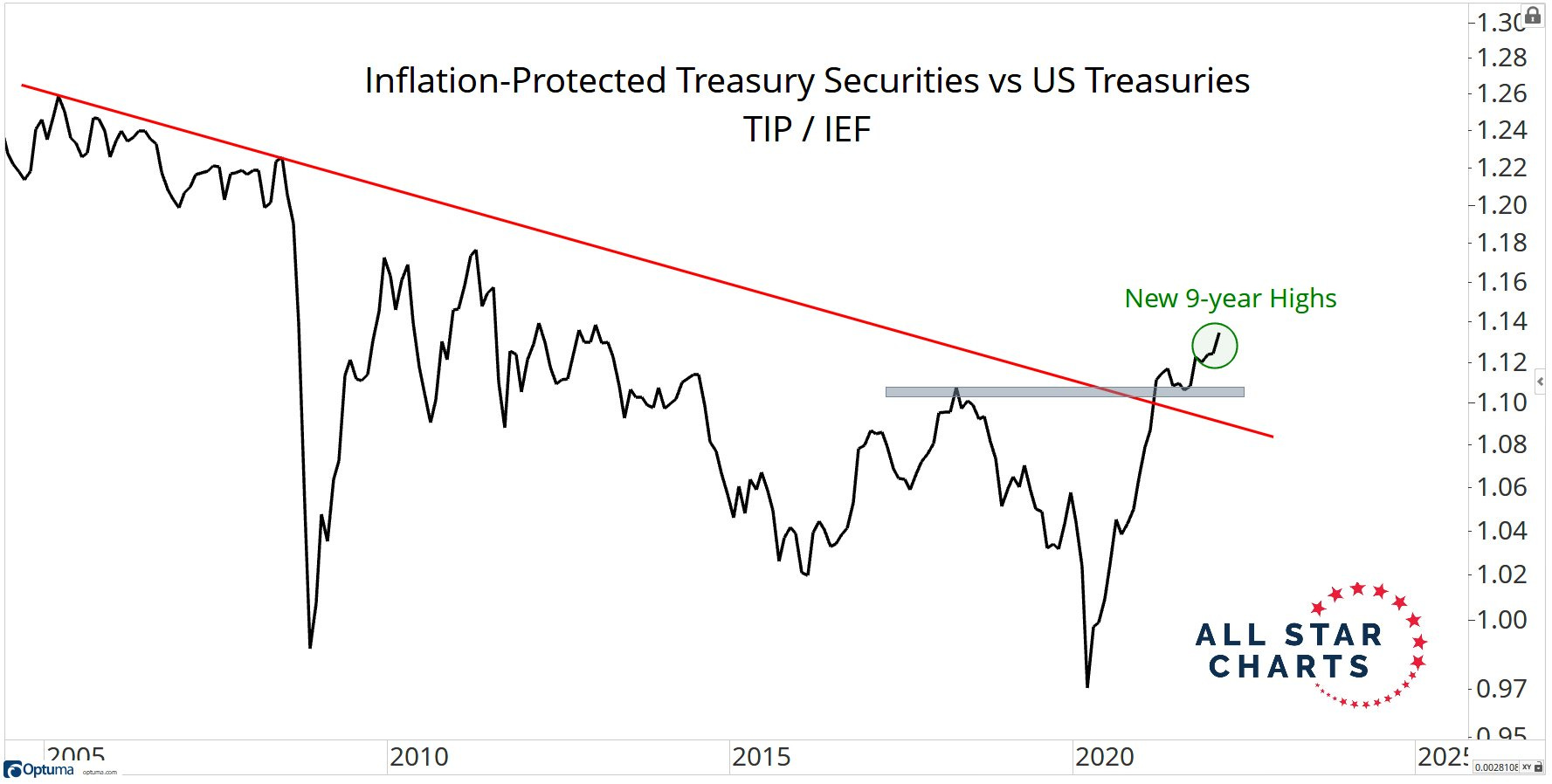

To support my argument, here’s an excellent chart I saw from J.C. Parets that helps to show how bond market participants are positioning themselves in the market:

By comparing the relative performance of inflation-protected Treasuries (TIPs) vs. standard Treasuries, we can see that there has been stronger relative demand for TIPs than pure Treasuries. Essentially, the bond market is indicating that inflation is likely to keep rising and bond market participants are putting their money where their mouth is. The bond market is usually right, and is considered “smart money” for a reason.

The economic factors are in place for inflation to remain persistent, the smart-money traders think it will persist, and my own personal inflation narrative has remained strong, therefore I feel confident that inflation will continue to rise in the short-term.

As it pertains to yields, which are positively correlated to inflation, here’s my technical analysis:

10-year yields are moving in a well-defined fashion. I’ve been sharing these levels since May 2021, highlighting the grey zone & the white channel specifically as key structure. The grey zone acted as resistance for the entirety of 2021, but has been acting as support so far in 2022. We are currently retesting this grey range once again, and I believe the most likely case scenario is that yields rebound on this level.

These “breakout, retest, and rebound” patterns are extremely common, and useful across all asset markets. For example, let’s evaluate this chart of S&P Global Inc. ($SPGI) since the beginning of 2020:

We have a descending channel & a grey resistance level, just like we see in 10-year yields, followed by a breakout to new highs. After the initial breakout move, the stock price falls and retests the grey range. When price retested the grey range, former resistance acts as current support, leading to a new extension higher. What happened next is the stock gained +30% in less than 6 months.

I actually shared this analysis in real-time on Twitter, posting this chart on 5/24/2021:

Surprisingly, $SPGI is retesting this grey range once again… and immediately rebounding higher! It’s not promised that it will continue to rebound, but it proves that buyers are stepping in with a significant level of demand at this level. To me personally, there are structural similarities between $TNX and $SPGI, so it will be interesting to see if $TNX follows suit.

Combining the inflationary factors, monetary policy outlook, bond market dynamics, and my own personal technical analysis, I reiterate my expectation for yields to rise. This will exacerbate the trends we’ve been seeing since November 2021, likely causing increased volatility in financial markets and increasing economic uncertainties.

Navigating Uncertainty:

In an environment of rising interest rates and rising inflation, risky stocks will continue to get punished. Despite $ARKK already falling -62% from the ATH’s in February 2021, I think there’s quite a bit of room to fall further. With that said, I think the broader stock market will perform much better, although the short-term momentum is clearly to the downside. In this environment, I expect value to outperform growth. This doesn’t mean I think the S&P 500 or the Nasdaq are going to crash — I don’t. However, I do think they’re going to face turbulence for the remainder of 2022. Recall, my “Investment Outlook for 2022” called for an 80% chance of below-average returns this year. I’ve been extremely consistent on this point for months, specifically citing the change in monetary policy and even highlighting the risk of geopolitical conflict with Ukraine/Russia.

I think it’s also prudent to recognize that many stocks in the S&P 500 are already beaten up. Specifically, 342 stocks out of 500 in the S&P 500 are down more than -10% from their 52-week highs (official correction territory). Additionally, 189 stocks in the S&P 500 are down more than -20% from their 52-week highs (official bear market territory). This means that 38% of stocks in the S&P 500 are in a bear market.

It’s logical to be attracted to many stocks at these valuations, and perhaps prudent to start building long-term positions by dollar-cost averaging into selective stocks. In this current environment, investors must be wholeheartedly ready to see their stocks decline further while maintaining a long-term vision. Patience will produce winners in this market, so I don’t see the need to act swiftly or allocate dry powder aggressively.

Which areas in the market are showing the greatest levels of strength right now?

Commodities & commodity-related equities.

In last week’s free report, I highlighted several dynamics taking place in the commodity market, particularly regarding energy and food-related commodities. I specifically cited oil, natural gas, wheat, soybean, corn, and rice. Here’s how all of these performed this past week:

Crude oil futures: +25%

Natural gas futures: +9%

Wheat futures: +40%

Soybean futures: +5%

Corn futures: +15%

Rice futures: +7%

Industrial & precious metals also had a strong week:

Gold: +4.5%

Silver: +6.5%

Platinum: +27%

Palladium: +6.5%

Copper: +9.3%

On the aggregate, the Bloomberg Commodity Index rose +13% this past week, reflecting extremely strong supply/demand dynamics in the market. As I said last week, I expect to see this trend continue (albeit at a slower rate of change). Here are some of the hottest industries related to these commodities: oil & gas exploration and production, thermal coal, steel, aluminum, metal miners, agriculture, and marine shipping.

Concluding Remarks:

I’ve tried to explain market dynamics in the simplest manner possible, by focusing almost purely on yields and the key factors that are driving them. I’m focused on analyzing the path of least resistance, concluding that yields will most likely move higher from the shift in monetary policy and inflationary pressures. The geopolitical situation overseas is putting pressure on this hypothesis, but I can’t stipulate how the geopolitical crisis will evolve, or to what magnitude. I expect to see continued weakness in speculative growth stocks, particularly those belonging to $ARKK (technology innovation fund), $IPO (IPO fund), and $XBI (biotechnology fund). I think fears of a global economic recession are being overstated, although I expect to see economic weakness throughout Europe and Asia when compared to the United States and North America. This could lead to ripple effects that impact the global financial markets; however, I don’t think this is likely at the present moment.

Considering how significant Russia is to global commodity markets (Russia is the third largest global producer of oil, the second largest producer of natural gas, and third largest producer of wheat), the conflict and sanctions will likely push commodity prices higher. Russia is an extremely important exporter of these commodities to the EU, indicating that EU countries will need to get their resources elsewhere. As these prices rise, it will put significant pressure on EU consumers, who are already facing multi-decade high inflation. Monitoring EU economic data will become extremely important as this situation unfolds, as it may foreshadow global economic conditions. We must wait and see how the data evolves.

As we continue to move forward through these uncertainties, the critical things to watch are: yields, inflation, monetary policy. If the Ukraine/Russia conflict escalates further, yields and monetary policy will react in a substantive way. Inflation will likely remain persistent, barring a massive reduction in economic activity and a recession. I will continue to pay attention to these three variables and discuss them in my weekly updates.

Talk soon,

Caleb Franzen

DISCLAIMER:

My investment thesis, risk appetite, and time frames are strictly my own and are significantly different than that of my readership. As such, the investments & stocks covered in this publication are not to be considered investment advice and should be regarded as information only. I encourage everyone to conduct their own due diligence, understand the risks associated with any information that is reviewed, and to recognize that my investment approach is not necessarily suitable for your specific portfolio & investing needs. Please consult a registered & licensed financial advisor for any topics related to your portfolio, exercise strong risk controls, and understand that I have no responsibility for any gains or losses incurred in your portfolio.