Edition #14 - 6.3.2021

Beige Book Report Highlights, S&P 500 Complacency, BTC Halving Cycle Update

Economy:

Yesterday afternoon, the Federal Reserve released the Beige Book report, which is a high level summary of the economic conditions in the 12 Federal Reserve Districts. The report is cultivated through the Fed’s business connections in each of the districts, who respond via questionnaires, interviews, or general discussions. While it’s interesting to see some of the different challenges that each respective district is facing, the aggregate data on the national level is what helps to drive policy. Here are some highlights that I saw from the report, from the national summary:

“Homebuilders often noted that strong demand, buoyed by low mortgage interest rates, outpaced their capacity to build, leading some to limit sales.”

“Lending volumes increased modestly, with gains in both household and business loans.”

“It remained difficult for many firms to hire new workers, especially low-wage hourly workers, truck drivers, and skilled tradespeople. The lack of job candidates prevented some firms from increasing output and, less commonly, led some businesses to reduce their hours of operation.”

“Contacts expected that labor demand will remain strong, but supply constrained, in the months ahead.”

“Input costs have continued to increase across the board, with many contacts noting sharp increases in construction and manufacturing raw materials prices. Increases were also noted in freight, packaging, and petrochemicals prices. Contacts reported that continuing supply chain disruptions intensified cost pressures. Strengthening demand, however, allowed some businesses, particularly manufacturers, builders, and transportation companies, to pass through much of the cost increases to their customers. Looking forward, contacts anticipate facing cost increases and charging higher prices in coming months.”

Really great information here, helping to highlight some of the very issues I’ve been covering in this newsletter. In the past, I’ve discussed how the Fed’s purchases of agency MBS at historical rates is putting downward pressure on mortgage rates, helping to boost the demand for residential housing. In yesterday’s post, I even highlighted how mortgage originations are even exceeding the peak of the housing crisis, albeit with a significant improvement in credit quality. Now we’re seeing how those demand-side pressures are impacting homebuilders and putting strains on the market.

I think it’s great to see an increase in lending volume, but I’d be curious to know if they are referring to the number of loan originations or the total dollar value of originations. The latter is what’s important, in my opinion. Either way, I’m hopeful that the loans are being used for capital expenditures and investment activity.

I have also discussed the labor shortage on this newsletter several times, and even included some of Neel Kashkari’s comments in yesterday’s report. Again, I expect these shortages will remain significant for the next 3-5 months before subsiding. Businesses want to hire, but the incentives just are worthwhile compared to the benefits being received for leisure. Essentially, if someone hypothetically values their leisure time at $8/hr, earn $10/hr from unemployment benefits, and price in health risks at $3/hr, then they’d only be willing to work in a position that pays them more than $21/hr. Until the unemployment benefits & health risks become less of a factor, these shortages will persist.

As I’ve been mentioning with my recent comments on inflation, the Fed is getting feedback from the business community that inflationary pressures continue to grow & the higher input costs for producers are being passed over to the end consumers. As such, as the producer price index rises (largely driven from commodity prices, labor costs, freight costs, and general transportation costs), so will the consumer price index. We’ve been seeing this trend so far already this year, and the expectation is that we’re still in the early innings.

Stock Market:

I saw two fantastic tweets today, both from Ryan Detrick (@RyanDetrick on Twitter), in regards to the S&P 500.

Tweet #1: “That is now 6 days in a row the S&P 500 has closed within 0.22% of the previous day's close. This ties the longest streak since December 2017. The longest ever? 10 in November 1961.”

Tweet #2: “The S&P 500 has now closed 9 days in a row within 2% of an all-time high, but not made a new ATH. This is the longest streak since 9 in a row in August'20.”

It’s hard to tell what to make of this information. It’s clearly highlighting an elevated level of complacency in the market, in which investors are still uncertain about the risk/reward of engaging in the market. Typically, after these “lengthy” periods of complacency and indifference, the market makes a decisive & strong move in one direction or another. I think I’ve made it well known that I have a bullish bias & strong view on equities, therefore my tendency is to see this as potentially positive.

With that said, I think the resurgence in $AMC, $GME, $NAKD, $KOSS, $BBBY and other WallStreetBets favorites is causing investors to de-risk prior to the eventual decline. While I say their decline is eventual, it’s very plausible their meteoric rise can sustain for several more days or weeks. As I’ve highlighted in this newsletter, one of my favorite quotes in the world of investing is, “the market can stay irrational longer than you can stay solvent”. During this time, I’ve continued to be a net buyer of equities, although I have yet to get involved with any of the “meme” stocks highlighted above and have zero intention of getting involved. Once this exuberance subsides, I think the market will likely have some decisive down days as a way to flush out capital. I don’t know how deep that move will be, and it’s possible it doesn’t happen at all. Time will tell.

Cryptocurrency:

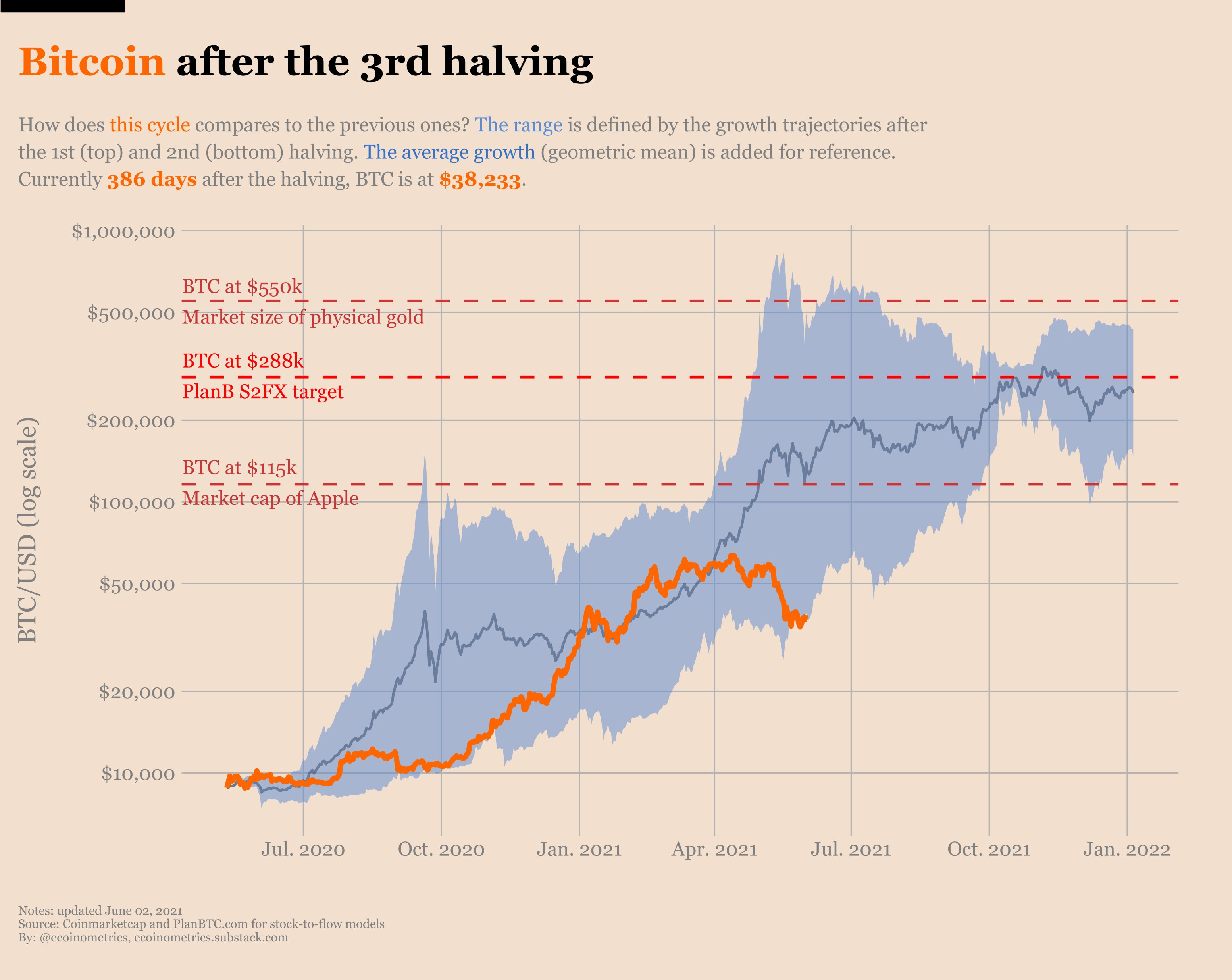

With the massive decline felt throughout the crypto market over the last month, I wanted to post a follow-up from a prior chart that I shared in my very first newsletter.

This chart shows the price action of the current halving cycle (the 3rd in Bitcoin’s 12 year history), beginning in May 2020, in orange. The blue “cloud” is the price action of the 2013 halving cycle (upper-bound) & the 2017 cycle (lower-bound). The dark blue line is the mean trajectory of the 2013 & 2017 cycles. The y-axis is given in logarithmic scale, which is usually a little strange for people to digest since we often aren’t exposed to continuously exponential growth. A logarithmic chart reflects a percent change in the underlying asset’s price rather than a nominal value change that we see often see in a linear chart. As such, a log chart will usually follow a progression of 1, 2, 4, 8 16, 32, etc. in which each rung along the axis is equidistant & represents a doubling, or 100% growth. That’s essentially what we have above, where the distance between $10k and $20k is the same as $50k to $100k and then to $200k.

While the significance of the decline cannot be understated, and objectively seems to shift the trend towards the downside, I continue to remain optimistic on the cycle trend & have been purchasing BTC on a daily basis over the last week. I’ve had many friends & connections reach out to me about my opinion during this decline, in which I’ve continued to reiterate that I believe we’ll be back over $50k by the end of the year. In my eyes, that is the conservative view. BTC is currently trading at $37,300 at the time of writing (10:15 pm ET, 6/2/21).

Until tomorrow,

Caleb Franzen