Hello everyone,

Here are the takeaways from today’s special report on the economy & inflation:

• The 12-month inflation rate increases to +6.8% for November 2021, continuing to validate the prediction I made in May 2021.

• Basic goods & energy utilities are driving inflation higher.

• Inflationary pressures are offsetting all benefits of higher nominal wages.

• The Federal Reserve is facing a critical predicament in their responsibility to maintain price stability.

This is not the newsletter that I wanted to write, as I truly don’t enjoy writing about inflation. 90% of the reason why I track inflation is simply to evaluate and understand what the Federal Reserve may do in the future. Recall, the Federal Reserve has a dual-mandate, established by congress, to promote maximum employment and price stability. The Fed aims to accomplish these goals through a variety of tools, but most notably through asset purchases and interest rate controls. The main reason why I care about the Fed is because of these tools, which undeniably impact asset prices. All else being equal, when the Fed pushes interest rates lower, this creates a tailwind for asset prices to rise.

While I thoroughly enjoy monetary economics above all other sub-groups of economics, my interest in the Fed is based in the fact that they have the power to produce, elongate, and control bull markets through monetary policy.

Therefore, by monitoring developments in the labor market and in consumer prices, we can attempt to understand monetary policy decisions by the Fed prior to them being announced. At the very least, we can attempt to understand the data being used in their framework to make decisions.

In May 2021, I was evaluating a wide-array of economic data and shared that “I wouldn’t be surprised if we see the 12-month CPI inflation numbers between +6% to +10% at some point in 2021.” When I published this prediction in Edition #6, the most recent CPI data was for April 2021, which was +4.2% on a trailing-twelve-month basis. My prediction was vindicated in early November upon the release of the September CPI data, reflecting a +6.2% increase in consumer prices year-over-year. This was the highest annual inflation increase since 1990.

When I reviewed this data in Edition #118, I reiterated my expectation that inflation would peak in the 6% to 10% window, but extended that window to Q1 - Q2 2022. It’s important to recognize that an inflation rate in this range is historic, particularly after experiencing muted inflation since the 2000’s. Most economists, including myself, didn’t think this was likely at the end of 2020. It was only until I saw early signals of inflationary pressures that I remained flexible and adjusted my outlook.

On Friday of this most recent week, the CPI data for November 2021 was released. In my mid-week publication, I specifically stated that “I have zero doubts that we’ll see another 12-month inflation rate that exceeds 6.0%, possibly even higher than 7.0%. At the present moment, the median estimate for the November figure is 6.7%. Again, I wouldn’t be surprised to see the data come in higher than that.”

The result was a 12-month inflation rate of +6.8%, given by a month-over-month increase of +0.8%. This 12-month rate of change in consumer prices was the highest reading since 1982, a 39-year high.

The core CPI, a measure of inflation that excludes food & energy prices, was up +4.9% YoY. This was the largest 12-month increase since the period ending June 1991. Unequivocally, we can say that inflation has not been transitory, with evidence & data that reflects a continued acceleration in consumer prices. Some notable increases for particular items were:

• Meat, Fish, and Eggs +12.8%

• Electricity +6.5%

• Gas Utilities +25.1%

• New Cars +11.1%

• Gasoline +58.1%

• Shelter +3.8%

I have serious concerns about the accuracy of “Shelter” being up only +3.8%. According to data from Apartment List, “the pace of rent growth has been cooling rapidly for the past few months, but growth is still outpacing pre-pandemic trends”. According to their most recent report, published on November 29, “the national median rent has increased by a staggering 17.8%” since the start of 2021.

If rents are increasing at such a rapid pace, we would logically conclude that home prices are increasing by the same, or more! The Case-Shiller U.S. National Home Price Index is currently up +19.51% on a one-year basis ending September 2021. So if rents and home prices are both up more than +17%, how are Shelter prices only +3.3%? I genuinely don’t have an answer for this. Considering that Shelter accounts for nearly one-third of of the CPI, this massively understated component could be masking the reality of inflationary pressures.

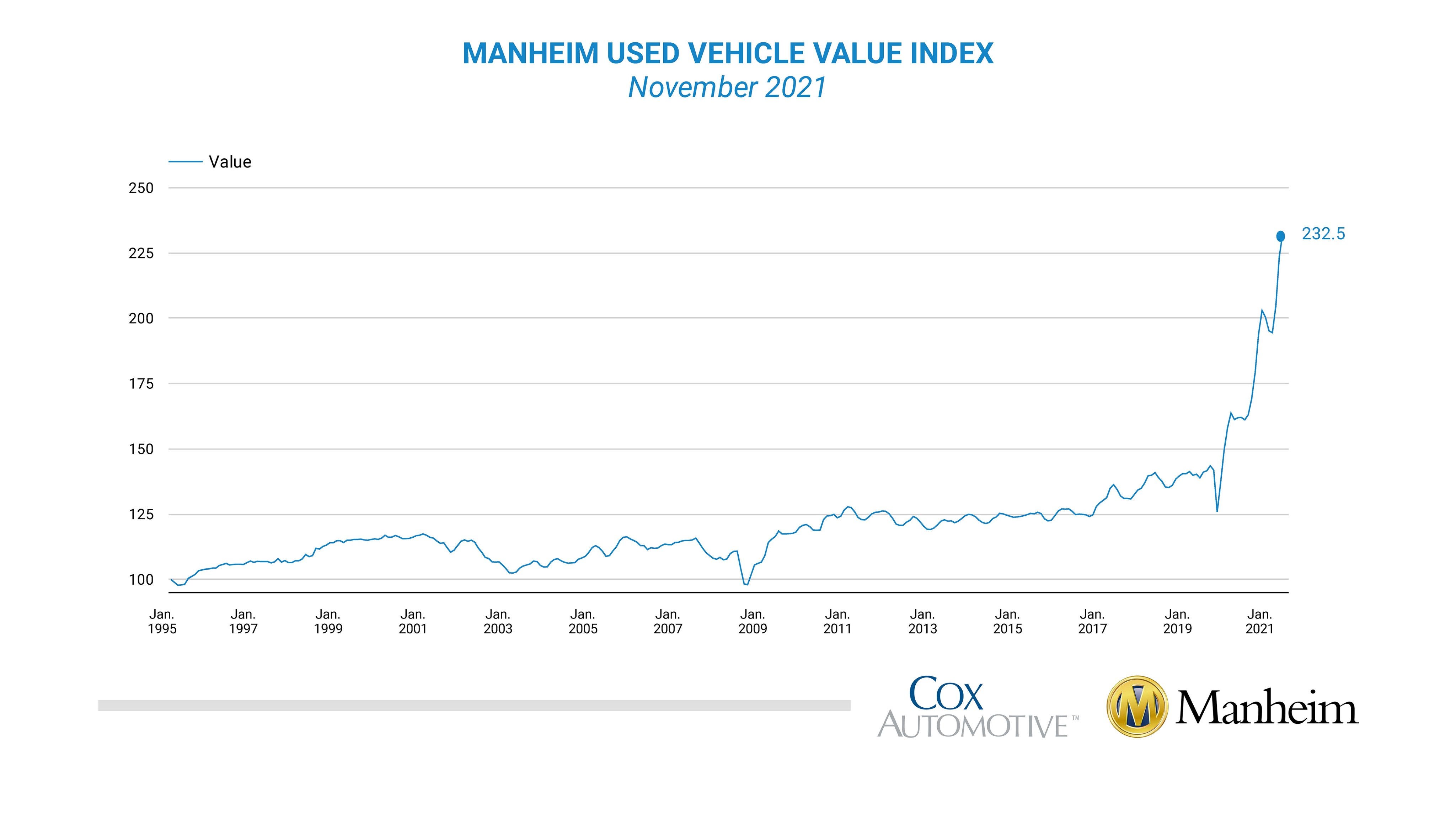

Additionally, used car prices continue to accelerate at historical levels. The Manheim Used Vehicle Value Index was one of the first metrics that I saw in May that made me truly question if we’d continue to see widespread inflation across the economic system. When I first published data on this in May 2021, the Manheim Used Vehicle Value Index was slightly above 200. Just six months later, the current reading is 232.5, up roughly +15%. On a year-over-year basis, the index has gained +43.5% since last November.

Price pressures for critical/basic goods, not luxury items, are relentlessly rising and outstripping any gains made in terms of nominal wage/salary increases. If we measure real hourly earnings, which adjust nominal gains against inflation, we can see that they’ve been negative for 8/11 months so far this year.

The current reading for real average hourly earnings was -1.9% for November 2021, meaning that the average employee is earnings 2% less per hour relative to November 2020. Ironically, this is happening during an economic expansion and recovery from one of the largest economic shocks in U.S. history. The nature of this recession deserves some culpability for this, particularly due to the disproportionate impact the pandemic has had on low-wage jobs, on the hospitality industry, and on retail labor. If we look at the chart above, we can see a massive increase in real average hourly earnings, which is entirely explained by the fact that many of the low-wage positions were fired. Absent these low-earnings jobs, the remaining labor in professional services boosted the average hourly earnings of the labor market! As the hospitality industry continues to recover and these jobs become more abundant, they will create a negative drag on the data. In conjunction with rapidly rising consumer prices, we’re seeing a sustained and dramatic decrease in real average hourly earnings.

So, where does all of this data leave us now? I will remain consistent with the outlook that I have been stating since May 2021, that the 12-month inflation rate will peak between 6% and 10%. The only update that I’ve made to that outlook is that my expectation is for the the inflation rate to peak by June 2022. The Federal Reserve has begun their tapering process, and even made it clear that it might be appropriate to taper more aggressively than they initially stated. There is a strong chance that the taper process concludes in April, rather than the original schedule of June 2022. From my perspective this merely means that the monetary stimulus punch bowl is being taken away faster. It’s important to recognize that monetary stimulus is still being injected into the financial system during the tapering process, but at a decreased rate. In a way, this form of monetary tightening is simply a precursor to raising rates, which is expected to come in the second half of 2022.

The purpose of tapering more aggressively and perhaps raising rates sooner/faster than anticipated is purely so that the Federal Reserve can try to pump the brakes on inflation. Based on their economic framework, the Fed believes that they can toe the line of slowing inflation while still maintaining smooth-functioning financial markets. This is a big test, one that is fairly unprecedented given the Fed’s lack of desire to raise rates. Recall, the last time we had substantial inflation was in the 1970’s, when Federal Reserve Chairman Paul Volcker raised interest rates to 20% to combat double-digit inflation. It worked, but it was an extremely painful period for U.S. consumers.

Based on current economic dynamics, the Federal Reserve could not feasibly raise interest rates to 20% today. Considering that interest rates have been at 0% for roughly nine of the last thirteen years, this is not a controversial statement. During the tightening process from 2015-2018, the Fed could only manage to increase interest rates to 2.5% before the market had a tantrum. I suspect this time will be no different. If the Fed is forced to combat runaway inflation, which is still a big “if”, they will almost certainly have to tighten monetary policy above a 2.5% interest rate. In that environment, I would expect to see a substantial slow down in terms of economic activity and a decrease in asset prices.

While I am critical of the Fed, I am sympathetic to their predicament. I am cautiously optimistic that they can succeed, but I am nonetheless rooting for their success. As always, I will remain flexible with incoming data and continue to update this group with my outlook.

Talk soon,

Caleb Franzen