Edition #127 - Stock Market Update

A Deep-Dive on Equity Prices, Rates, and Asset Returns

Happy Saturday everyone,

The mood of the market over the last two weeks can best be described as trepidatious. We’ve seen rates continue to inch higher, putting pressure on general equity prices and specifically on growth stocks. The market was additionally put into a frenzy on Friday with increasing uncertainty surrounding a new COVID variant, which exacerbated some of the market pressure to end the week. Amidst this market pressure, growth stocks experienced the worst of the selloff from the rotation into safe-haven assets.

Earlier in the week, I was doing research on some of the retail-favorite stocks that have been getting hit the hardest. One aspect that I noticed right away is that many of them were relatively recent IPO’s (within the last 18 months) or were promising tech/growth companies that still had a lot to prove. To confirm that this trend wasn’t just anecdotal, I pulled up the chart of Ark Invest’s flagship fund, $ARKK. Many of the companies within this fund are relatively “young”, at least as publicly traded stocks, and practically all are using technological advancements and innovation to disrupt their respective markets. Essentially, it’s a perfect proxy for what I was noticing at the surface level.

After a massive run in 2020, in which $ARKK became the poster-child of tech investing, the stock has had an abysmal 2021. Relative to 2020’s return of +152%, the 2021 YTD return of -14% is not what investors were likely expecting. Even worse, the fund has fallen more than -52% from the YTD highs in February 2021.

The choppy behavior and downtrend in 2021 made me curious to dive deeper into the individual holdings within the fund in order to understand how successful Ark has been at picking stocks. Considering that $TSLA is the highest allocation within the fund, currently around 9%, I was baffled to see such terrible performance so far in 2021. In attempt to analyze the under-the-hood metrics, I summarized the takeaways in a Twitter post on 11/23/2021. For those who don’t follow me on there, or who didn’t see that post, I wanted to share the takeaways as a precursor to the main point of this premium report. Here is the unraveled thread I posted, which can be viewed in its original form here:

“Is it possible to track the return of $ARKK excluding $TSLA? It’s clear that the fund is investing in the most innovative companies, and arguably the ones that are most critical to future tech, but the fund is currently -15% YTD and down -33% from the YTD highs. $TSLA is up +63% YTD…

I just pulled $ARKK’s holdings report as of 11/23/21 and the YTD return data on each holding they currently have. The average YTD return is -13.2%. If we exclude $TSLA, it’s -15%. This is an equal-weight average, which isn’t intended to show us $ARKK’s YTD return. Of the 42 stocks they currently own in the fund, 31 have a negative YTD return (26% hit rate). 21 positions in the fund currently have a YTD return worse than -20%. Every -20% loss requires a +25% return to break even. 7 positions in the fund have a YTD return larger than +25%. Along these same lines, there are 8 positions in the fund with a YTD return worse than -50%, but only 2 positions with a return larger than +100%. Essentially, there are a handful of massive losers and not enough winners to offset them. This approach above is weighting agnostic.

I can't stand this question, but is $ARKK dead? No. Far from it in my opinion. 2021 has been a super hard year for stock pickers and traders, particularly relative to 2020. I think egos were inflated from last year's returns & a lot of people got caught too far on the risk curve. $ARKK is here to stay, and I think Cathie's approach in the long-run will be effective. There's room for $ARKK in a well-balanced portfolio, but I do have doubts as using it as a trading instrument or following their open-sourced trading activity. In my opinion, they should significantly reduce healthcare & biotech exposure in $ARKK. Based on my count, 18/41 stocks in $ARKK are related to these industries. The average return on these positions is -24.1%. I'd prefer if they were only in $ARKG.”

At a fundamental level, the significant majority of individual stocks currently held by $ARKK are underwater in 2021 and underperforming the S&P 500 by a wide margin. As an investor, how do you absorb this information and create actionable insights going forward, based on what we know in the present moment? That’s what we’ll be discussing today.

The rest of this newsletter is a deep-dive intended to explore these market dynamics and to understand why they are occurring. Once that is achieved and we are able to put the puzzle pieces together, I’m hopeful that investors will have a clear perspective on where we are, how we got here, and where we might be headed next. Enjoy!

The first aspect that I specifically want to highlight is that the struggles of $ARKK, its various components, and dozens of other tech companies that had stellar 2020 returns can be largely attributed to one main factor: yields.

If we examine interest rates in 2020 by tracking the yield on 10-year government Treasuries, we can use the ticker symbol $TNX to analyze the 10-year Treasury Yield Index. In 2020, $TNX had a calendar year decline of -52% despite experiencing an +78% gain from August - December 31st, 2020.

If we track the same index for the YTD performance in 2021, we get the following:

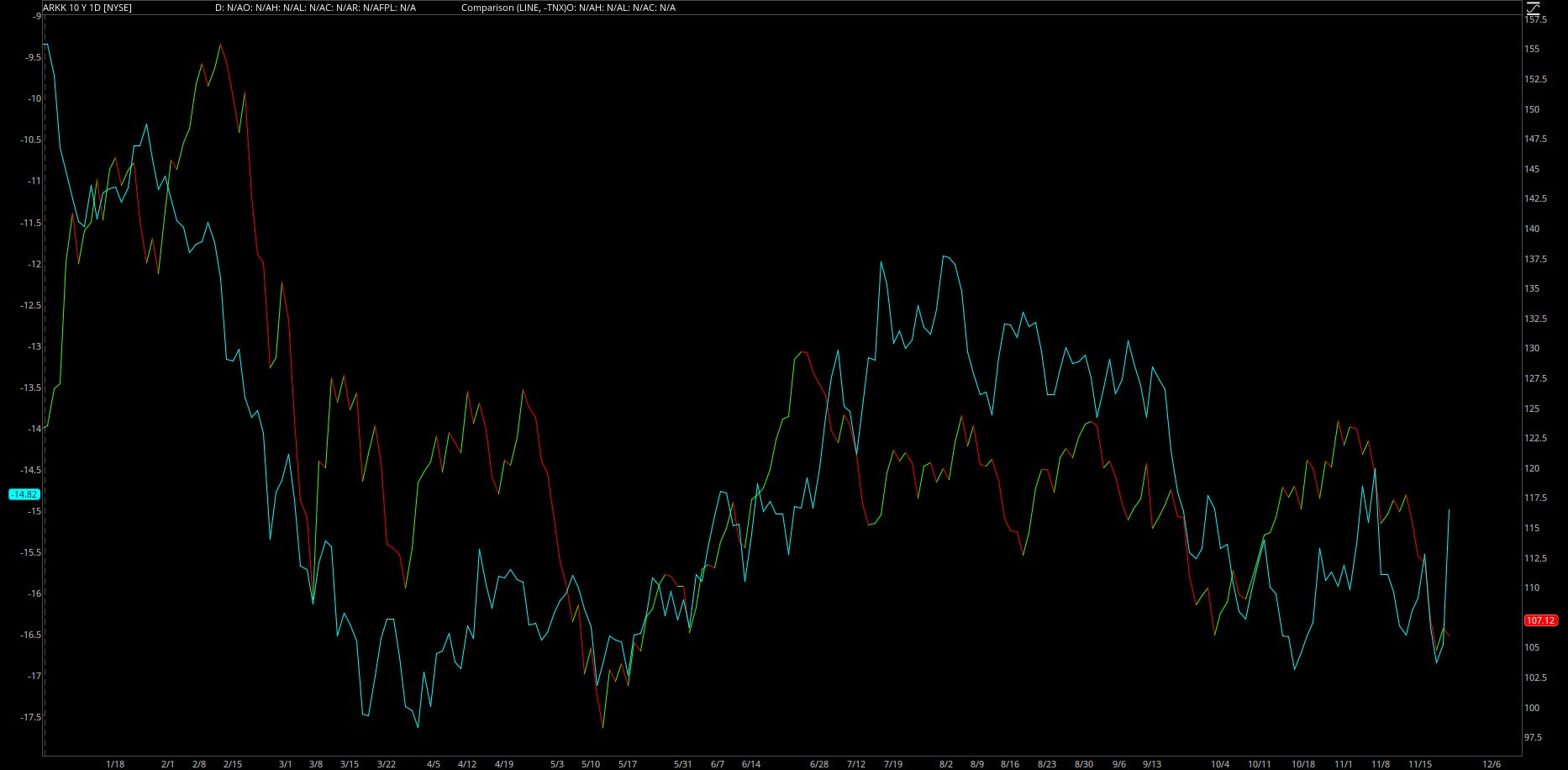

So far in 2021, the 10-year yield index has increased by +61%, which is a complete 180° switch in behavior. As I have continuously pointed out in my newsletter, stock prices (and particularly growth stocks) have an inverse relationship with yields and interest rates! In fact, if we invert the $TNX index (teal line) and overlay the chart on top of $ARKK (red/green line), we can clearly identify the high correlation between them in 2021.

As we can see, there is an uncanny correlation between these two variables, highlighting that $ARKK is extremely sensitive to the interest rate environment. I truly wasn’t expecting the correlation to be this clear, so even I was astounded by these findings. This chart alone is a perfect visual representation of the fact that interest rates and asset prices have an inverse correlation. Considering that we’re taking the inverted performance of $TNX, the lock-step behavior of these two variables is proof that the rate-sensitivity of an asset is a determining factor for that asset’s returns.

Therefore, on the aggregate, if we want to know how high growth technology stocks will perform going forward, it’s imperative to attempt to understand where rates are headed. As I laid out in my newsletter to all subscribers this morning, yields plummeted during Friday’s session as investors rushed to safety from the new COVID variant; however, it’s most likely the case that yields will rise under the Federal Reserve’s tapering process and liftoff schedule.

As an investor with a time horizon of 3-12 months, I’d be extremely wary to get invested in unprofitable tech/growth stocks barring any material outlook in the trajectory of rates going forward. Based on what we know right now, it appears that the path of least resistance for rates is to gradually rise higher. I want to specifically highlight why I’m articulating so specifically against unprofitable tech/growth stocks….

Quite simply, the 2021 correlation between -$TNX and the S&P 500 is not nearly as decisive as -$TNX vs. $ARKK.

As we can see, the correlation between the two is strong, but occasionally loose. While the correlation to $ARKK was crystal clear, the correlation with $SPX is sometimes in effect, but occasionally gets distorted (as we see in the beginning of 2021 and again since October 2021). The broader market, given by the proxy of the S&P 500, has been able to generally perform well regardless of what rates are doing in the short-term. For one, this shows the clear benefits that industry/sector/thematic diversification can provide by using a “shotgun” approach and simply buying the entire market — theoretically, it should provide muted volatility to rates vs. rate-sensitive stocks.

The key here is that unprofitable tech companies that trade at very high price/sales ratios are extremely rate-sensitive. At a near-zero interest rate, investors are willing to forego a 0% yield for the potential returns of a stock with fast-growing revenues and future profits, even if that company is generating negative profits in the short-run. As soon as rates rise, the rapid revenue growth and potential future profitability aren’t worth as much in the present moment, resulting in a lower stock price (all else being equal). When a company’s stock price is primarily driven by their revenue growth and not by profits, dividends, share buybacks, etc., they are going to be extremely rate sensitive. Therefore, as rates occasionally make wild swings and unexpected turns, these rate-sensitive stocks get whipsawed around.

This is why $ARKK is tightly correlated to yields, while the S&P 500 is more loosely correlated. To drive this point home, I’ll leave you with the following chart of Goldman Sachs’ Non-Profitable Tech Index as of 11/22/2021. For the sake of this context, ignore the data in orange and only focus on the blue data.

As we can see, non-profitable tech stocks had a monster year in 2020 and drastically outperformed the S&P 500. With the context of how 10-year Treasury yields plummeted in 2020, this makes perfect sense! However, the story in 2021 has been the complete opposite, as the non-profitable tech index is preparing to make YTD lows relative to the S&P 500. In my opinion, this is almost entirely driven by the uncertainty surrounding the Fed’s tapering schedule, rate liftoff, and the general trend of rising rates so far in 2021.

It’s also worth noting that rate sensitivity isn’t solely determined by whether or not the company is classified as either tech or non-tech. To prove this, it’s worth pointing out that the Nasdaq-100 is up more than +24% YTD while $ARKK is down double-digits.

Therefore, if we expect that rates are likely to rise going forward, we are likely better off by limiting and reducing our exposure to non-profitable tech. At the very least, it’s a reminder that if we invest in any non-profitable tech stocks, we must be extremely diligent in our analysis of those companies and believe in the long-term potential with the intent of dollar-cost averaging into said stocks.

I continue to remain extremely optimistic on U.S. equities looking out over various time frames, despite the continued rise in yields and the possibility that they will continue to rise under the Fed’s tapering schedule and potential rate liftoff in 2022. While we don’t know what pressures the market will face in the short-run, it has proven its ability to produce strong inflation-adjusted returns in the intermediate and long-run. I believe that will continue to be the case, based on the various items we addressed above and my fundamental outlook on the U.S. economy, global economic conditions, and technological innovation.

Best,

Caleb Franzen