Don't Fall For It Again

Investors,

I want you to think back to 2023, when bears and Doomers constantly complained that only 7 stocks were going up and that broad-based weakness under the hood was going to topple the S&P 500.

They tried — tirelessly, I might add — to tell us that the market was weak.

They tried to tell us that the Russell 2000 was the “real” stock market and that its underperformance was a harbinger of things to come for the large-cap indices.

As we know, that “theory” (which wasn’t even really true in the first place) was ineffective, with the S&P 500 now generating a +33.65% YoY return and the Russell 2000 gaining +29.9% YoY.

I’m bringing this up because I saw this narrative reappear this week and I want you to be prepared and armed to fight this erroneous narrative once again.

For context, the Vanguard Mega-Cap Growth ETF ($MGK), which has a 58.1% weighting to the Magnificent 7 stocks, gained +3.73% this week. Additionally, the NYSE FANG+ Index ($NYFANG), an equal-weight basket of 10 mega-cap technology stocks, gained +5.98%.

Meanwhile, the equal-weight S&P 500 ($RSP) was down -1.3%!

Clearly, this divergence is extremely wide & notable.

So what do we do with this information?

Well, while bears want us to be concerned about this deterioration, I’m just going to repeat the same message that I did throughout 2023: there is nothing bearish about the MVPs of the market acting like MVPs and putting the team on their back.

Imagine being a Golden State Warriors fan and being discouraged because Stephen Curry is playing basketball too well, scoring too many threes, and getting too many assists en route to too many victories.

Imagine being a fan of Argentina’s national football team and complaining that Messi is too good and he’s going to be the reason why the team won’t succeed.

Imagine being an Apple shareholder and complaining that Tim Cook is too good of a CEO, or an NVDA shareholder who complains about Jensen Huang being too much of a visionary.

The fact of the matter is that performance and positive contributions are almost always concentrated at the top, something that is explained by the Pareto Principle, which explains that 80% of a system’s output is produced by 20% of its inputs.

You can (and should) read more about that here.

So when the best companies in the world (yes, the entire world) are producing the lion’s share of the returns for the stock market, isn’t that exactly what we should expect (and root for)?

My answer is yes.

Maybe your answer is no.

And hey, you have the right to disagree, but the data is on my side.

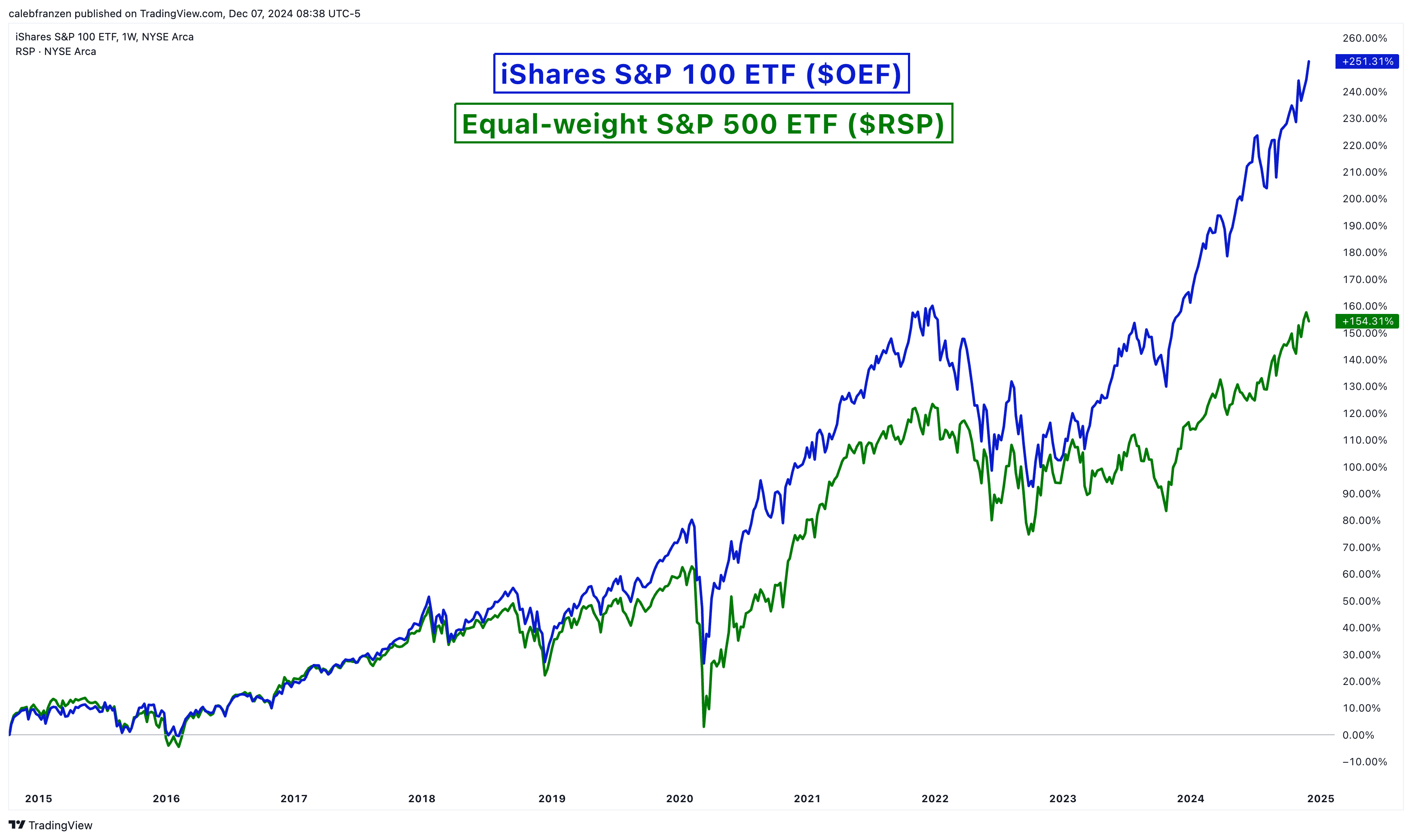

Just look at the excess returns produced by the biggest names in the S&P 500, which we can illustrate through the 10-year performance of the following:

🔵 iShares S&P 100 ETF ($OEF)

🟢 Equal-weight S&P 500 ETF ($RSP)

And guess what happens if we add one more ETF into the mix, the Invesco S&P 500 Top 50 ETF… even more outperformance!

It’s almost like the best companies are the best for a reason, and they get treated as such via consistent outperformance vs. the rest of the market.

So, as we think about the complaints this past week about performance being so concentrated at the top and only the biggest stocks showing strength, I genuinely hope (and believe) that it will continue.

As an investor, you have two choices on this matter:

You can complain about it and cry that the biggest stocks are outperforming the smallest stocks; or…

You can accept it, align with it, and benefit from their outperformance.

I’ve done the latter.

Macroeconomics:

I’m only going to talk about macro in the remainder of this brief report, with comments on two quick dynamics from the past week.

First & foremost, the labor market continues to be dynamic & resilient.

After the surprising miss in the nonfarm payrolls data for October, coming in at +12,000 jobs for the month, macro Doomers warned us that “this is finally it!” for the umpteenth time. They told us that there was a good chance that the figure would be revised lower and actually come in negative. They told us that the November data was going to show negative job growth too.

But now we have the data…

Nonfarm payrolls growth in November 2024 was +227k jobs, exceeding expectations for +214k. Additionally, the October result was revised up by +24k jobs to a new total of +36k AND the September results were also revised higher by +32k to +255k jobs!

Read that again… job growth was revised UP for each of the past two months.

Therefore, with this newly revised data at our disposal, the U.S. economy has added an average of 172.6k jobs per month on a trailing 3-month basis.

Meanwhile, wage growth is still robust at +4.0% YoY and layoffs declined to 1.6M.

Monthly layoffs have generally remained stable since January 2023:

However, if we measure total layoffs relative to the size of the labor market (civilian labor force), we see that the layoffs rate is back below 1%:

Finally, the employment of part-time workers for economic reasons has declined for the 3rd consecutive month, highlighting the limited stress in the labor market:

Given that part-time employment is roughly at the same level as it was 3 years ago, it’s clear (at least to me) that broader economic conditions are not putting pressure on the labor market (and vice versa).

So let’s tie this into the economy quickly, because the Atlanta Fed published their latest estimate for Q4’24 real GDP growth earlier in the week, now coming in at +3.3%, driven primarily by a jump in real gross private domestic investment from +1.2% to +1.8%.

This is now the highest estimate that the Atlanta Fed has published for Q4’24, which again highlights the resilient & dynamic nature of the U.S. economy, which continues to grow at a solid pace, even after adjusting for inflation.

Thankfully, I’ve continued to stay on the right side of these macro dynamics for the past two years, going back to when I initially highlighted how the Fed was actually threading the needle on the soft landing in November 2022.

At the time, I was still hesitant to accept the soft landing scenario… however, this early recognition of basic facts is what helped me to fully shift into a bullish stance in April & May 2023, both regarding asset prices and the economy itself.

I’ve been pounding the table about the “resilient & dynamic” nature of the economy ever since.

For those of you who trusted in my analysis, my objective approach, and my willingness to stick my neck out on this call, I’m hopeful that the market has treated you extremely well over the past 20+ months.

I’ll be publishing in-depth research on the stock & crypto markets in tomorrow’s premium edition of Cubic Analytics, exclusive only for monthly/annual members.

Best,

Caleb Franzen,

Founder of Cubic Analytics

This was a free edition of Cubic Analytics, a publication that I write independently and send out to 11,700+ investors every Saturday. Feel free to share this post!

To support my work as an independent analyst and access even more exclusive & in-depth research on the markets, consider upgrading to a premium membership with either a monthly or annual plan using the link below:

DISCLAIMER:

This report expresses the views of the author as of the date it was published, and are subject to change without notice. The author believes that the information, data, and charts contained within this report are accurate, but cannot guarantee the accuracy of such information.

The investment thesis, security analysis, risk appetite, and time frames expressed above are strictly those of the author and are not intended to be interpreted as financial advice. As such, market views covered in this publication are not to be considered investment advice and should be regarded as information only. The mention, discussion, and/or analysis of individual securities is not a solicitation or recommendation to buy, sell, or hold said security.

Each investor is responsible to conduct their own due diligence and to understand the risks associated with any information that is reviewed. The information contained herein does not constitute and shouldn’t be construed as a solicitation of advisory services. Consult a registered financial advisor and/or certified financial planner before making any investment decisions.

Please be advised that this report contains a third party paid advertisement and links to third party websites. The advertisement contained herein did not influence the market views, analysis, or commentary expressed above and Cubic Analytics maintains its independence and full control over all ideas, thoughts, and expressions above. The mention, discussion, and/or analysis of individual securities is not a solicitation or recommendation to buy, sell, or hold said security. All investments carry risks and past performance is not necessarily indicative of future results/returns.

Each investor is responsible to understand the investment risks of the market & individual securities, which is subjective and will also vary in terms of magnitude and duration.

It's wild that bears are still acting so bearish, solid evidence that they're detached from reality.