Disinflation + Pause = Bullish

Investors,

Just this past week, we saw the following take place:

The Dow Jones hit new all-time highs.

The S&P 500 had its highest daily close since January 12, 2022.

The Nasdaq-100 had its highest daily close of all-time.

The Russell 2000 hit new YTD highs, officially up +12.7% in 2023.

On top of this, semiconductor stocks (SMH & SOXX) are hitting new all-time highs, broker-dealers (XBD) are hitting new all-time highs, home construction stocks (XHB & ITB) are hitting new all-time highs. And it gets better…

The Renaissance IPO ETF IPO 0.00%↑ hit new YTD highs.

The Select Sector Financial ETF XLF 0.00%↑ hit new YTD highs.

The iShares Expanded Tech ETF IGV 0.00%↑ hit new YTD highs.

The Ark Fintech Innovation ETF ARKF 0.00%↑ hit new YTD highs.

The Select Sector Industrials ETF XLI 0.00%↑ hit new all-time highs.

The iShares Core U.S. Growth ETF IUSG 0.00%↑ hit new YTD highs.

The First Trust Cloud Computing ETF SKYY 0.00%↑ hit new YTD highs.

The iShares Core Russell U.S. Value ETF IUSV 0.00%↑ hit new all-time highs.

The Invesco S&P Small Cap Industrials ETF PSCI 0.00%↑ hit new all-time highs.

This is bull market behavior. This is uptrend behavior. This is constructive behavior.

What caused these objective facts? The same things that have been unfolding all year!

In addition to a milieu of statistical indicators, momentum dynamics, and pure technicals, the fundamental catalysts can be summarized by disinflation, resilient economic data, a stronger-than-expected consumer, better-than-expected earnings, and further confirmation that the Federal Reserve is done with their rate hike cycle and will remain “paused” in light of continued improvements in the inflationary trend.

Aside from the final point, these are the key dynamics that I’ve highlighted all year.

Regarding the final point about Fed policy, I said this in June 14, 2023:

“The Federal Reserve doesn't flip-flop.

This pause marks an almost certain inflection point in monetary policy, wherein an extended pause is the most likely case scenario going forward.

Remember how Fed officials have invoked the mistakes of Arthur Burns?

They won't make that mistake again, so this pause should reflect their confidence that disinflation is firm and that we'll be at their 2% target soon enough. My prediction is before the end of the year.

Regarding a cut, I don't foresee it this year, based on the signals that I'm seeing in the bond market. The signal from the 3M and 6M Treasury yield is dynamic, so perhaps the cut becomes probable in the coming weeks/months/quarter.

A pause at 5.08% effective federal funds rate is still sufficiently effective for the Fed to combat inflation, but the Federal Reserve is late to the disinflationary party. We are in disinflation.

We have been in disinflation.

Disinflation will get stronger in the coming 3-6 months.

The Fed seems to finally recognize this, officially, with their policy decision at today’s FOMC meeting.”

So I was wrong about getting to 2% by year-end, as I didn’t foresee a +40% increase in crude oil over a 3-month period, but my assessment of monetary policy was solid.

This was the first time I stated that the Fed was done with their rate hikes, continuing that “I expect that this pause is an ‘end’” after predicting that the Fed would hike between +0.5% and +1.25% in 2023. With the final Fed meeting of 2023 officially in the books, the amount of total hikes was +1.0%.

In their policy meeting this week, following the release of both the CPI & PPI for November 2023, the Federal Reserve forecasted several rate cuts in their 2024 dot plot for the first time. This is a firm indication that the Federal Reserve is done raising rates — and the market responded as such.

Yields plummeted. The U.S. Dollar Index dropped. Treasuries rose. Equities rose.

My thesis over the past 6 months is playing out: further disinflation will force the Fed to cut rates in order to prevent the real federal funds rate from rising too much and inadvertently tightening into a resilient (but softening) economy.

The market is now pricing this scenario in, which is contributing to the new high achievements that I highlighted above.

I’m going to keep this edition short & sweet, highlighting three key charts:

Macroeconomics:

Regarding the updated CPI data for November 2023, my favorite chart is the following:

The YoY rate of change in headline CPI excluding Shelter is +1.4%, down from +1.5%.

While this was a modest deceleration, continuing to prove that the disinflationary trend is intact, the primary reason why I’m bringing this up is because Shelter is the largest and laggiest datapoint in the Consumer Price Index. In removing Shelter, we can evaluate how literally every other variable of inflation is evolving, on the aggregate. The fact of the matter is that CPI ex-Shelter is comfortably back within the historically normal range.

Stock Market:

The Russell 2000 just had it’s strongest 30-day momentum thrust since December 2020:

More specifically, the small-cap index with the largest exposure to financials just gained +19.8% in a 30-day period.

While this doesn’t necessarily indicate that momentum will continue to create a ripple effect of strength in the months ahead, even though I lean towards saying it will, it’s hard to be bearish after seeing these kinds of achievements.

When this signal happened in mid-2020, stocks performed well thereafter.

When this signal happened in December 2020, stock performed well thereafter.

Perhaps the Russell 2000 itself didn’t perform well, but the S&P 500 & the Nasdaq did.

There’s probably a lesson in that…

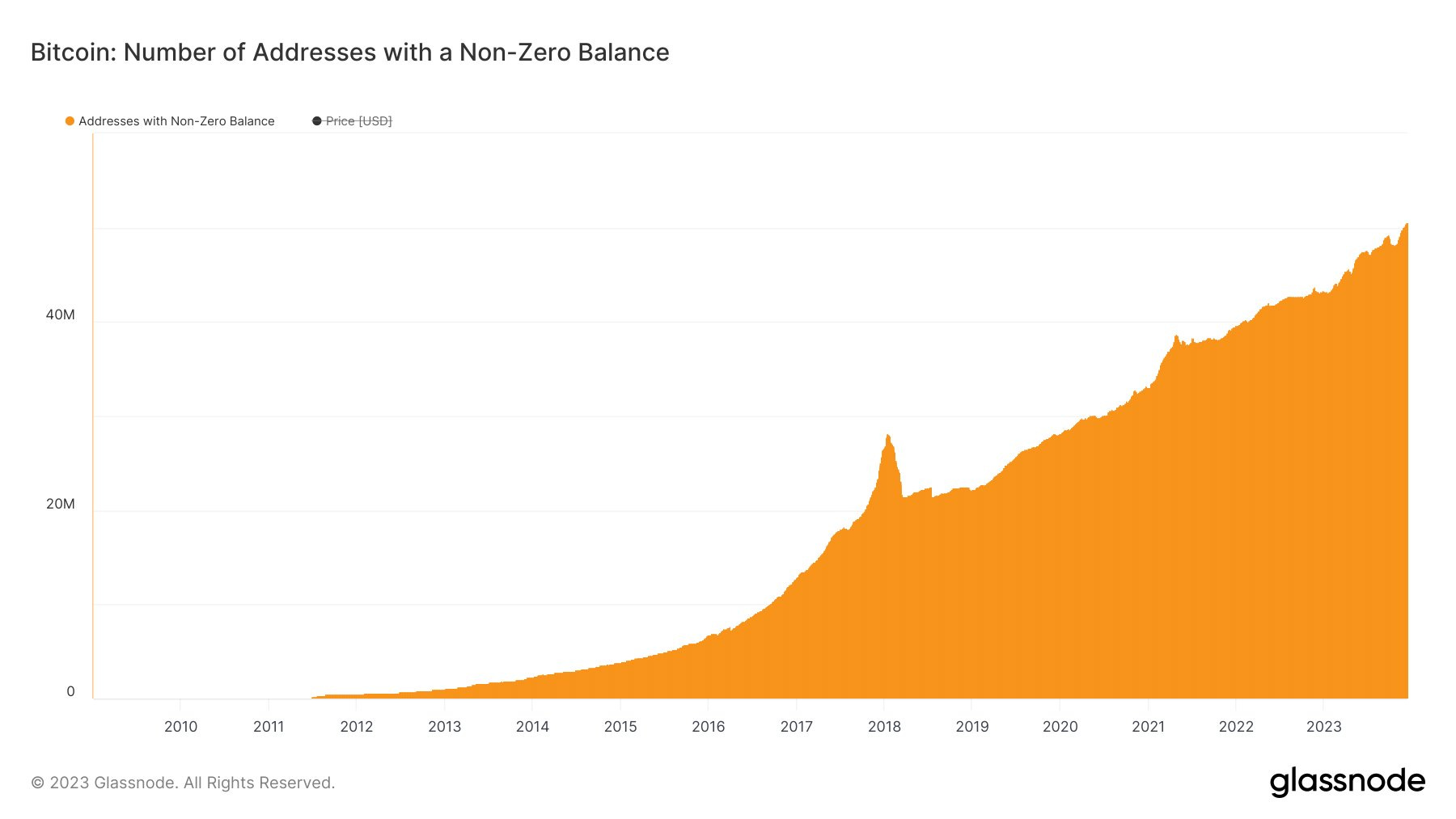

Bitcoin:

Wallet addresses holding a positive amount of BTC hits a new all-time high:

This is extremely straight-forward, but we continue to see evidence that Bitcoin adoption, in terms of a growing user-base, is increasing. While these wallet addresses could be rising because a single Bitcoin user is now creating another new wallet or because a new user has joined the network is unknown, but we can nonetheless zoom out and acknowledge that the growth & the trend is remarkable.

That’s 50+ million Bitcoin wallets folks.

Best,

Caleb Franzen

DISCLAIMER:

This report expresses the views of the author as of the date it was published, and are subject to change without notice. The author believes that the information, data, and charts contained within this report are accurate, but cannot guarantee the accuracy of such information.

The investment thesis, security analysis, risk appetite, & timeframes expressed above are strictly those of the author and are not intended to be interpreted as financial advice. As such, market views covered in this publication are not to be considered investment advice and should be regarded as information only. The mention, discussion, and/or analysis of individual securities is not a solicitation or recommendation to buy, sell, or hold said security.

Each investor is responsible to conduct their own due diligence and to understand the risks associated with any information that is reviewed. The information contained herein does not constitute and shouldn’t be construed as a solicitation of advisory services. Consult a registered financial advisor and/or certified financial planner before making any investment decisions.

ممکنه فارسی ترجمه کنید؟

Great report! Leading stock market sectors giving good reason to be bullish all along!