Cuts Aren't Coming Until This Happens

Investors,

Cuts aren’t coming for at least 6 months, based on the data that I’m currently seeing.

This has been the exact same message that I’ve said all year, encouraging investors to be conservative and patient in their expectations for when rate cuts will occur.

However, other analysts have recently been reinvigorated in their belief that cuts are around the corner, likely to come within the next 2-3 Fed meetings.

These are the same analysts who predicted rate cuts by mid-2023 when the 2Y Treasury yield fell below the Fed funds rate in December 2022, and the same analysts who predicted rate cuts by March 2024 at the start of this year.

They’ve been wrong and they will continue to be wrong once again.

In the video analysis below, I share when rate cuts are most likely to occur:

In the remainder of this report, I’ll cover the following dynamics:

The relationship between the labor market and inflation

The significance of the labor force participation rate

Ongoing stock market dynamics and fundamentals

Bitcoin’s recent consolidation

If you’re one of the 11,500+ investors who appreciate these unbiased & exclusive reports, consider sharing this free analysis with someone in your inner-circle so that they can benefit too!

Macroeconomics:

Regarding macro, there are two things that I want to focus on:

Disinflation

Labor market resilience

Thankfully, we can kill two birds with one stone…

The Job Openings and Labor Turnover Survey (JOLTS) was released on Tuesday, showing a significant decline in job openings at the end of April 2024. The challenge with this data is that we don’t know the context for why job openings are declining:

Are they declining because companies are delisting job openings? or

Are they declining because companies have those job openings?

We don’t know.

Nonetheless, what we do know is that job openings declined to 8.059M from 8.355M.

Based on research that I’ve shared in the past, the decline in JOLTS is disinflationary and this latest round of data allows us to update the correlation between job openings and YoY levels of inflation:

🔵 Job openings

🔴 Core CPI inflation YoY

Therefore, the significant decline in job openings illustrates that the most likely path for inflation is a further deceleration, which by definition means that more disinflation is coming down the pipeline via the labor market.

In other words, if the Fed is looking for more evidence that inflation is moving sustainably towards their 2% target, this type of labor market data is accretive for a shift in monetary policy.

Additionally, the marginal increase in the unemployment rate from 3.9% to 4.0% is likely accretive to the Fed as they balance the risks of their dual-mandate.

First of all, I want to highlight that the unemployment rate has largely been moving sideways for the past 2.5 years… as the level in January 2022 was also 4.0%.

It’s important to understand WHY this uptick in unemployment occurred. While some folks on X and pundits on T.V. want you to believe that unemployment is rising because the labor force is weakening, it’s actually the opposite! The unemployment rate is rising because more people are entering the labor force!

Specifically, the labor force participation rate for people between the ages of 25-54 is reaching new highs post-COVID:

With a “prime-age” LFPR of 83.6%, this is the highest reading since May 2002.

Yes, you read that right — May 2002.

This is what happens when there’s an abundance of opportunities to generate strong levels of income, which are also growing steadily at +4.1% YoY (avg. hourly earnings).

So how does the rising labor force participation rate cause the unemployment rate to rise? It’s simple! When people “rejoin” the labor force, they immediately start looking for opportunities. Interestingly, people who are unemployed but aren’t looking for work aren’t actually counted as part of the labor force and they don’t contribute to the unemployment rate measurement. However, once they rejoin the labor force and begin looking for work, they are counted as unemployed (unless they immediately accept a job).

Therefore, the unemployment rate should rise (by definition) when the labor force participation rate rises, all else being equal, because more people are in the labor force and looking for new employment opportunities.

Why is this important? So long as the labor force participation rate is rising, I’m not overly concerned by modest upticks in the unemployment rate, because I view higher labor force participation as a boost to aggregate income (more people looking for work means more people accepting jobs, means more people making money).

Understanding this simple correlation between the unemployment rate and the LFPR helps to explain why the actual number of people who are counted as unemployed (job losers) actually declined in the month of May, despite the fact that the unemployment rate increased.

On net, the data we received for JOLTS, ADP Private Payrolls, and the Nonfarm Payrolls indicates that the labor market continues to be resilient & dynamic. While certain aspects are weakening and other aspects certainly aren’t strong, we must objectively agree and recognize that the labor market is still resilient & dynamic.

My belief has been (and continues to be) that it will remain resilient.

Stock Market:

First and foremost, both the S&P 500 (chart below) and the Nasdaq-100 achieved their highest weekly closes of all-time yesterday.

I’ve said this sentence many times in 2024, en route to the S&P 500 generating a YTD return of +13% (annualized calendar year return of +30%).

It’s almost like we’re in an uptrend and a bull market!

Hint: we are.

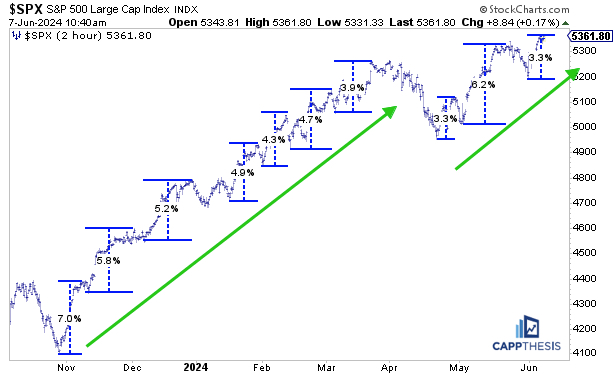

My good friend Frank Cappelleri, from CappThesis, shared the following chart of the S&P 500 that highlights the symmetry of the current market rally:

All I see over the past 6 months is higher highs and higher lows, which certainly isn’t indicative of a bearish trend…

From a fundamental perspective, we’re also seeing internal fundamentals improve from an earnings standpoint, as shown by this chart from Bank of America:

Specifically, we’re seeing that the forward earnings contribution for S&P 500 constituents is no longer solely dependent on NVDA and the other Magnificent 7 companies! In other words, the S&P 493 are expected to contribute positively to the aggregate earnings for the S&P 500, which should be a positive catalyst for stock market performance going forward.

We’re seeing both technicals & fundamentals continue to align in a positive manner.

That doesn’t sound bearish to me.

Bitcoin:

Friday’s trading session saw a rapid decline from $71.9k down to $68.4k.

This certainly felt like a big swing (because it was), but it wasn’t out of the ordinary.

It was normal volatility and downside risk that has been ever-present throughout Bitcoin bull markets… and make no mistake about it — we are in a bull market.

Presently, I’m focused on a few things:

The LuxAlgo Price Action Concepts, which effectively held as resistance & support.

The 100 & 200-day EMA cloud, which continues to rise higher & provide support.

I remain bullish on BTC here and expect to see a breakout to new all-time highs in the near future, but I’m always prepared for more downward volatility and will be buying more Bitcoin on dips along the way.

Zoom out… I see an uptrend and bullish catalysts in the economy & the stock market.

I’m not going to fight those trends.

Best,

Caleb Franzen,

Founder of Cubic Analytics

DISCLAIMER:

This report expresses the views of the author as of the date it was published, and are subject to change without notice. The author believes that the information, data, and charts contained within this report are accurate, but cannot guarantee the accuracy of such information.

The investment thesis, security analysis, risk appetite, and time frames expressed above are strictly those of the author and are not intended to be interpreted as financial advice. As such, market views covered in this publication are not to be considered investment advice and should be regarded as information only. The mention, discussion, and/or analysis of individual securities is not a solicitation or recommendation to buy, sell, or hold said security.

Each investor is responsible to conduct their own due diligence and to understand the risks associated with any information that is reviewed. The information contained herein does not constitute and shouldn’t be construed as a solicitation of advisory services. Consult a registered financial advisor and/or certified financial planner before making any investment decisions.

Great points and explanation as always brother, thank you 🙏🏻

The nuance on unemployment by pointing out the participation rate at 22-year highs was clutch. I haven't seen any other analyst make the connection that a higher participation rate is bullish, but will also, naturally, increase the unemployment rate. Fantastic observation, Caleb!