Correlations Are Breaking

Labor Market Data vs. The Stock Market

Investors,

This is a jam-packed report, analyzing the most important developments and charts from the past week. Of note, I’ll be covering key relationships between the labor market and ongoing stock market trends based on the latest data released this week.

Specifically, this edition of Cubic Analytics will focus on the following:

Regional banks, deposit outflows, and the Earthquake Effect

Labor market data implications for inflation

Labor market data implications for economic activity

Labor market data implications for the stock market

Bitcoin’s fundamental value proposition & network activity

Before jumping into the data, I’m excited to remind you about my sponsorship with MicroSectors! MicroSectors is an ETN brand with a variety of solutions for gaining direct leveraged & inverse leveraged exposure to unique aspects of the market. When I first came across the team behind the ETN’s, REX Shares, I was impressed with their wide range of products that filled unique niches in the market, allowing investors to take long & short positions on gold, mega-cap tech, oil stocks, big banks, and many other investment ideas.

For example, their newly-released bull/bear ETN’s for 3x gold exposure just recently started trading in mid-February. Gold has been a hot topic in 2023 amidst ongoing bank failures and the desire for investors to flock to safety. In fact, gold futures traded at the second-highest price of all-time earlier this week at $2,085/oz!

I’ve gotten to know the REX Shares team over the past 6+ months and I feel that this is the most natural fit for me in terms of a first official sponsor, especially since I’ve already been using and discussing the MicroSectors ETN’s prior to the sponsorship.

You’ll be hearing more about Rex Shares and MicroSectors in the next few editions of Cubic Analytics, and perhaps beyond!

Check them out on their website or on Twitter!

Macroeconomics:

Call me a broken record, but the Earthquake Effect is still underway. Concerns about the banking industry rippled to Pacific West Corp $PACW, Western Alliance Bancorp $WAL, and First Horizon Corp $FHN, all of which had extremely volatile weeks. The entire regional banking sector continued to face selling pressure in the first four trading sessions of the week, with many banks losing more than 30% of their market cap in a single day. However, concerns seemed to abate on Friday and the same regional banks who faced immense selling pressure launched like a rocket ship.

Take the headliner of the group PACW, for example, who had the following gains/losses during the trading week:

Monday: -10.7%

Tuesday: -27.6%

Wednesday: -2.2%

Thursday: -50.4%

Friday: +81.7%

All in all, the stock had a negative weekly return of -43.25% and has a YTD return of -74.8%. In order to erase all of the YTD losses, the stock would need to gain +298%.

The regional bank ETF, KRE 0.00%↑, is down nearly -35% YTD.

While there are certainly concerns about the broader banking system and the large banks, fears are primarily centered around the regional banks. For example, we can compare the relative performance of XLF 0.00%↑, the Financial Select Sector SPDR ETF, vs. KRE and see that the overall financial sector is drastically outperforming the regional banks:

This isn’t representative of a healthy regional banking industry. In fact, the only similar behavior we’ve seen to the current environment was in the aftermath of the Great Financial Crisis, in which XLF/KRE made a v-shaped recovery. However, this is starkly different than the current circumstance where XLF/KRE is blasting to new all-time highs!

Deposit outflows continue to accelerate on a year-over-year (YoY) basis, based on new commercial banking data as of Wednesday, May 3rd. Throughout the history of the data series, which begins in 1974, deposits have never contracted at this pace.

In fact, it’s rare for them to even contract at all! After flooding the financial market with liquidity in 2020 and 2021, causing deposits to skyrocket, the Federal Reserve’s stark shift to monetary tightening and balance sheet runoff has induced the inverse effect on deposits. With the Federal Reserve continuing to raise interest rates this past week by another +0.25%, the effective federal funds rate is now at 5.08%. Even if the Fed pauses from here, capital will continue to flow to where it can generate the highest yield.

With deposit rates practically at zero (see below), savers are taking advantage of money market funds and Treasuries, accessible outside of the deposit banking system, in order to capture yield while still remaining in minimal risk investment vehicles.

National Deposit Rates (Interest Checking) as of April 2023: 0.06%

National Deposit Rates (Savings) as of April 2023: 0.37%

Why would a saver sit idly in the banking system to capture these yields, particularly as new regional banks are falling at such a substantial magnitude? The short answer is they wouldn’t and the deposit data reflects that they aren’t sitting idly by. Investors are likely capitalizing on 3M Treasury yields offering an annualized coupon rate of 5.25%, the 6M Treasury at 5.1%, and even money market funds that are yielding 5.05% after the Fed’s latest rate hike.

The combined dynamic of banking concerns + the massive spread between Treasures/MMF’s vs. checkings/savings yields will continue to produce deposit outflows in the weeks and months ahead, likely putting more banks under pressure and exposing more naked swimmers. Amidst ongoing Federal Reserve tightening & balance sheet runoff, the Earthquake Effect will almost certainly expose more naked swimmers in the traditional financial system, which was the underpinning of my 2023 market outlook.

As banks are forced to become more conservative with their balance sheet amidst deposit outflows, the tightening of credit conditions and outright contraction in lending activity will anchor economic activity, all else being equal.

However, new labor market data continues to indicate that the U.S. labor market is dynamic and resilient. While there was weakness in the JOLTS data for March 2023, the nonfarm payroll data for April 2023 was strong overall. Here are the main charts you need to know and why they’re important:

1. Job openings at the end of March to 9.59M from 9.974M in the prior month.

It’s hard to say if this is bad news because we don’t have context around why the decline is happening. For example, are job openings getting filled or are employers delisting their openings? The former would be good news while the latter would indicate weakness in the labor market, but we don’t have this level of granularity in the report. Nonetheless, we can generally see that declining job openings occur prior to recessions leading into the GFC and even into 2020, so the current decline doesn’t necessarily bode well for the economy.

2. The quits rate fell to 2.5% in March 2023, vs. 2.6% in the prior month.

Given the historic correlation between the quits rate and the YoY CPI inflation rate, I think this decline foreshadows more disinflation (aka lower inflation) in the months ahead.

3. The unemployment rate fell to multi-decade lows in the April 2023 NFP data, from 3.5% to 3.4%, while the prime-age labor force participation rate (LFPR) made new 15-year highs.

In other words, Americans in their prime earning years are actively participating in the work force and able to find jobs at a historic pace. While this dynamic cannot be extrapolated forward to imply that this trend will continue, it indicates that aggregate income levels are strong.

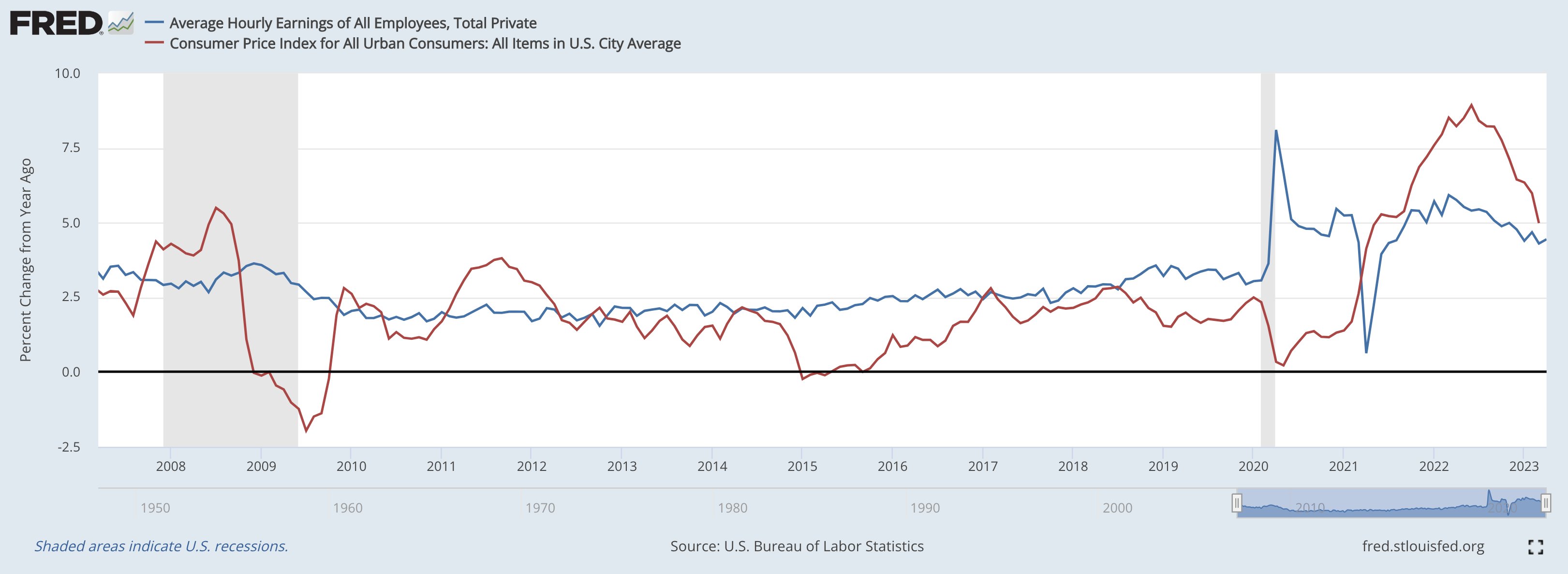

4. Average hourly earnings hit a new all-time high of $33.36, up +4.4% YoY.

While there isn’t a super tight correlation between average hourly earnings and inflation on a month-to-month basis, it’s logically accurate to think that wage growth will need to price growth. The ongoing stagnation in the YoY growth of average hourly earnings bodes well for disinflation, though earnings growth is still elevated.

Stock Market:

Tying in some of the labor market data above, I want to highlight the ongoing divergence between job openings and the Nasdaq Composite Index. Looking at the chart below, we can see how these two variables are tightly correlated through history; however, the Nasdaq bottomed in October-December 2022, while the job openings data has declined significantly since then.

This contradiction between asset prices and JOLTS data is concerning, particularly if labor market data worsens in the months ahead, which is certainly possible.

Nonetheless, it feels like bulls are truly in control of the stock market in the present environment, with the Nasdaq-100 inching moderately higher this week by +0.1%. While the weekly gain isn’t anything impressive, the index gained +2.48% from Thursday’s intraday lows and achieved the highest daily close of 2023. The Nasdaq-100 hasn’t been this high since mid-August 2022 and has now gained +27% from the October 2022 lows.

Continuing to focus on the relationship between labor market data and the stock market, the chart below highlights one of my favorite fundamental correlations, comparing the YoY rate of change in the unemployment rate vs. the YoY rate of change in the Nasdaq Composite Index:

This chart indicates a very simple truth: an acceleration in the unemployment rate, particularly a shift from a negative to positive YoY % change, has traditionally foreshadowed a recession and a contraction in the YoY performance of the stock market.

While this inverse correlation remained true throughout 2022, seeing a sharp acceleration in the YoY % change in the unemployment rate and a sharp contraction in the Nasdaq Composite Index, we’ve seen both variables trend higher in 2023.

Notably, the YoY % change in the unemployment rate has not crossed into positive territory yet, an important signal that could foreshadow pain for the broader economy, it’s clear to see that both variables are on the cusp of transitioning from negative to positive territory. Given that the unemployment rate was 3.6% in May 2022, the next NFP data would need to jump from 3.4% to at least 3.6% to cross out of negative territory. This isn’t an unfathomable increase and would still represent historically low unemployment, but I think this second-derivative data is extremely important to monitor. As of the latest NFP data for April 2023, the YoY rate of change in the unemployment rate is -5.6%, a sizable decline from March’s result of -2.8%.

Bitcoin:

Upon ongoing concerns and news about bank failures, the apex digital asset has continued to attract capital seeking a home outside of the traditional financial system, where owners of the asset can self-custody and distinctly own their purchasing power.

While all depositors of the various bank failures have been made whole, the failures in and of themselves have highlighted the fragile nature of the fractional banking sector and reignited the conversation around third-party trust. Considering that Bitcoin has a 99.988% uptime, with the last structural outage occurring in 2013, there is a high margin of security that Bitcoin the monetary network will continue to function as intended.

In this sense, it’s important to bifurcate Bitcoin the monetary asset vs. Bitcoin the monetary network. While the value of the asset in its current level of adoption will certainly fluctuate, the monetary network itself is consistently effective while having no centralized point of failure or direct third-party control/trust.

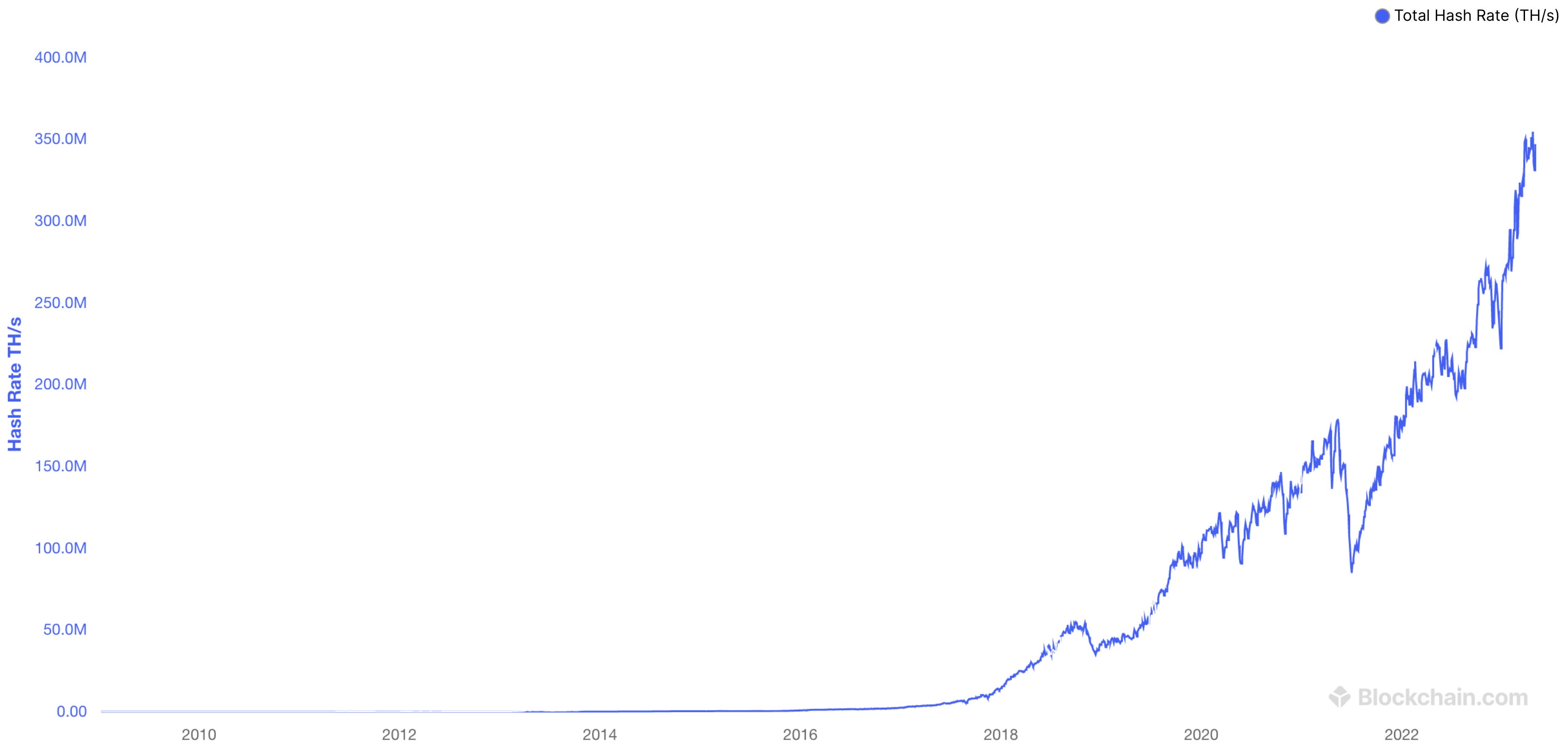

The hash rate of the network has reached new all-time highs recently, speaking to the competitive nature of decentralized miners to validate the blockchain & secure the network.

At the present moment, the total computational power dedicated to this task is 346.967 exahash per second, or 346 quintillion, or 346 billion billion, or 346,967,000,000,000,000,000 calculations per second. The incentive to mine Bitcoin, an asset with a fixed and increasingly scarce supply, has produced the most decentralized network in the world, allowing Bitcoin owners to sleep well at night knowing that unknown third parties across the world are competing to secure the network.

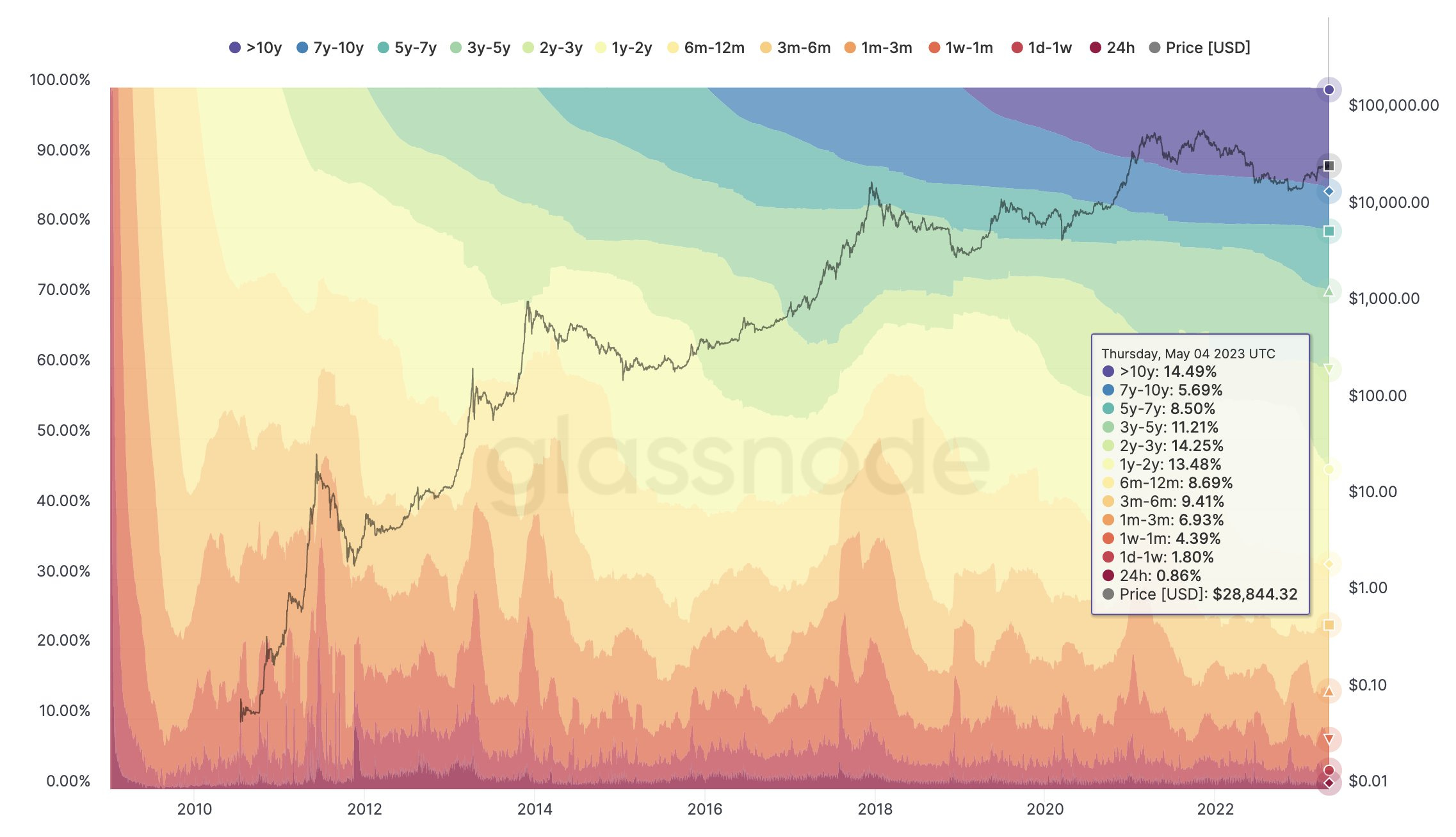

The conviction of long-term holders remains concrete, with the percent of Bitcoin being unmoved in 2 years reaching a new high of 54%.

Considering that the price of Bitcoin was $56,300 on May 6th, 2021, which then fell to $28,800 in July 2021, then back to $69,000 in November 2021, to $15,500 in November 2022, it’s amazing that 54% of investors haven’t sold or moved their Bitcoin to another wallet address. Hodlers are simply hodling, trusting that the value of the network itself will continue to rise, regardless of what the BTCUSD exchange rate is doing.

Best,

Caleb Franzen

DISCLAIMER:

This report expresses the views of the author as of the date it was published, and are subject to change without notice. The author believes that the information, data, and charts contained within this report are accurate, but cannot guarantee the accuracy of such information.

The investment thesis, security analysis, risk appetite, and time frames expressed above are strictly those of the author and are not intended to be interpreted as financial advice. As such, market views covered in this publication are not to be considered investment advice and should be regarded as information only. The mention, discussion, and/or analysis of individual securities is not a solicitation or recommendation to buy, sell, or hold said security.

Each investor is responsible to conduct their own due diligence and to understand the risks associated with any information that is reviewed. The information contained herein does not constitute and shouldn’t be construed as a solicitation of advisory services. Consult a registered financial advisor and/or certified financial planner before making any investment decisions.

This report may not be copied, reproduced, republished or posted without the consent of Cubic Analytics and/or Caleb Franzen, without proper citation.

Please be advised that this report contains a third party paid advertisement and links to third party websites. These advertisements do not constitute endorsements and are not necessarily representative of the views or opinions of the newsletter author. The advertisement contained herein did not influence the market views, analysis, or commentary expressed above and Cubic Analytics maintains its independence and full control over all ideas, thoughts, and expressions above. The mention, discussion, and/or analysis of individual securities is not a solicitation or recommendation to buy, sell, or hold said security. All investments carry risks and past performance is not necessarily indicative of future results/returns.