Investors,

I’ve booked three separate 1-hour slots with subscribers on Monday evening to discuss market conditions and answer any questions that they might have about the broader economy and financial markets. I’m super excited to see that members are utilizing this new Substack feature, where I’m lucky enough to be apart of the beta program. I’d love to chat with you! For my availability, check the link below:

Book a meeting with Caleb Franzen

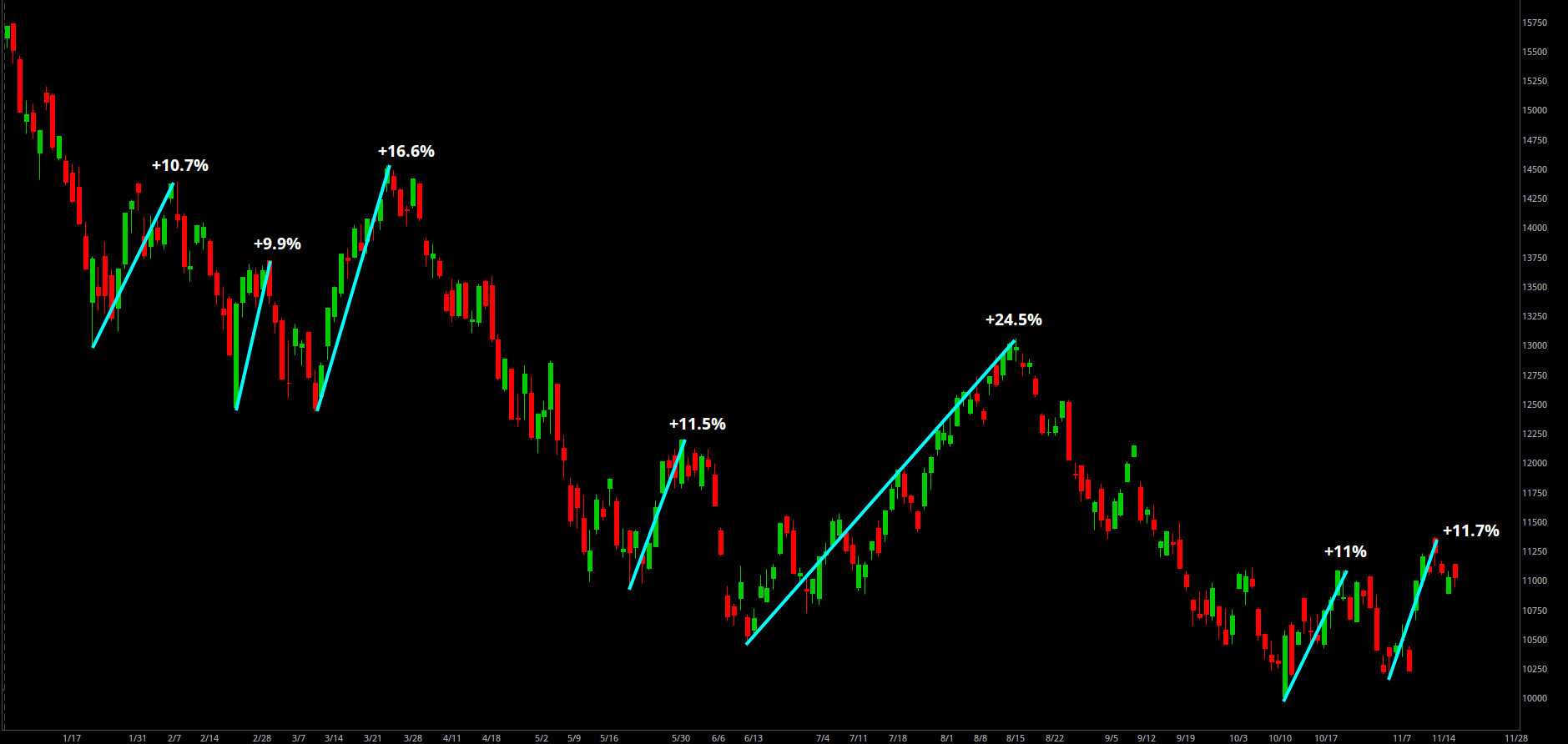

The current market environment is very intriguing at the present moment, as inflationary concerns begin to ease and we’ve completed 8 months of the Fed’s rate hike cycle. As far as investors are concerned, we continue to inch closer towards an inevitable Fed pivot, which is helping to fuel bullish market dynamics since the mid-October lows. The market has staged an impressive rally during this time, with the Nasdaq Composite Index producing the 6th double-digit percentage rally of 2022.

Despite these significant rallies, the index has fallen a total of -28.75% YTD, highlighting the overwhelming nature of persistent rate hikes & declining liquidity. Aside from the Dow Jones, the other major indexes appear to be losing momentum. At the very least, the market is digesting the gains from the past month & perhaps setting the stage for a continued market rally. While it’s much easier to be optimistic now that prices have improved to the upside, I don’t want to get carried away by the positive emotions. As I mentioned in yesterday’s newsletter, “there’s nothing like price to change sentiment”. I’d encourage all investors to remain level-headed.

I continue to express my doubts & concerns about the market, and found further evidence to support my stance during Friday’s session. Consider the following: all asset classes have been plagued by the rising interest rate environment. The traditional 60/40 portfolio is having one of the worst years of all-time, because bonds aren’t providing a safe-haven for investors and correlations have become extremely tight between stocks & bonds. Knowing this, I decided to look at the relationship between the S&P 500 and zero-coupon bonds (widely accepted as the most interest-rate sensitive bonds, because they don’t pay any coupon).

Starting in April 2021, stocks and zero-coupon bonds, ZROZ 0.00%↑, started to move in lockstep! Interestingly, there have been brief deviations during the 2022 bear market, where stocks provide more upside during market rallies & bonds generally remain muted. Eventually, stocks (dark blue) play catch-up to the downside and converge upon zero-coupon bonds (teal).

That’s exactly the position that we’re in right now: stocks & bonds have diverged, during a period where stocks have drastically outperformed bonds as yields have declined. We’ve seen this situation unfold four times in 2022, with the fifth occurrence right before our eyes. Will the current case repeat the prior four? I believe that it will.

In the remainder of this report, I’ll be breaking down other important charts, datapoints, and trends that I’m seeing in the market, with the intention of giving you an edge over the coming weeks. As always, we’ll dive into the S&P 500’s under-the-hood metrics in order to diagnose how most stocks are behaving in this environment.